“Prices have dropped to the lowest level in years. Pipelines are overbooked, and supplies are backing up. There is just not enough capacity to get out of the supply area and into the market area. Pipeline capacity is at a premium. The last time prices got to this level, producers shut in.”

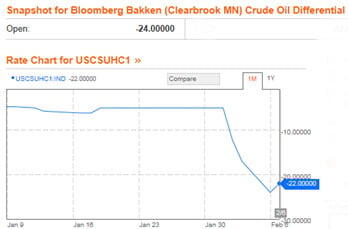

Natural gas in the Rockies a few years back? It certainly could be. But noooooo. It is crude oil today. In Canada and in the Bakken. Bakken crude oil is more than $22/bbl cheaper than WTI. The differential was $11 a week ago, and $4-5 in early January. These changes happen fast. According to Reuters, Western Canada Select was running at $31.25 a barrel under WTI yesterday, actually up $4.25 versus Monday (explained below). This crude was only $18/bbl under WTI a couple of weeks back.

And to add insult to injury, the Brent-WTI differential has widened back out. From $20 over the past couple of days, narrowing slightly yesterday (also explained below).

There are several things happening at the same time responsible for all of this chaos. First, the story that was so familiar to the Canadian and Rockies gas markets. There is too much of the stuff and we can’t get it out. North Dakota kicked out a release in January saying “Bakken Blend crude production in the state averaged more than half a million bpd, marking a new record. Crude production averaged nearly 510,000 bpd in November, up about 22,000 b/d from October and more than 150,000 b/d more than November 2010. ….500,000 bpd of crude represents about 10% of U.S. production.”

On the Canadian side, we talked about some of this a couple of weeks ago in a RBN Markets posting - A Home for Canadian Oil Sands Crude? Canadian oil sands production is ramping up. Volume from the Athabasca Oil Sands Project in Q4 increased 30% over the previous year to about 200,000 b/d.

And in the midst of the increasing supply, (a) BP’s big refinery in Whiting, Indiana (largest U.S. consumer of Syncrude) is has a major unit outage, (b) capacity on the Enbridge pipeline system is maxed out, (c) rail capacity is having issues (see Ridin’ the Bakken Slow Rail), and (d) the Seaway reversal (to move 150,000 b/d from Cushing to the Gulf Coast eventually getting to 400,000 b/d) has been delayed until June. Damn. Damn! Where is that pipeline?

As these things usually happen, all the factors converged and the differentials shifted almost overnight. The graphic below is indicative what has happened to the Bakken crude oil differential.

This whole market looks like the perfect storm. And it sounds eerily familiar to Rockies natural gas traders backed up in that market in 2007-08, looking at prices of $.01/mmbtu. Yes, I do mean one penny. Simultaneous maintenance on a couple of pipelines in June 2007 contributed to one of the first major price shocks of that fiasco.

How bad could it get for the crude market? Fortunately, not nearly as bad as the 2007-08 gas market. There are many more transportation options (pipeline, rail, truck). There are more storage options (there was minimal gas storage in the Rockies). New refining capacity for running heavy crude in the Midwest is coming on line. And there is the possibility of the curtailment of production from oil sands producers if their economics go underwater. In fact, the 110,000 b/d Horizon plant (Canadian Natural Resources facility, 4th largest oil sands plant in Canada) shut down for “unplanned repairs” yesterday, which helped kick both Canadian and WTI higher. This is what bumped up the Western Canada Select price and narrowed the Brent-WTI spread.

The current situation will abate, but it will be back – over and over again. It will be a roller coaster ride for crude producers as supply increases, infrastructure catches up and demand hiccups happen. This cycle will continue until transportation capacity permanently exceeds production capacity – one way or the other.

There is a lot of crude looking to find a market, and transportation constraints are starting to take their toll on producer netback prices. It is back to the future for gas people that lived through this kind of market five years ago. Remember those transportation constraints? Remember what happened to the Henry Hub when those transportation constraints were finally relieved by new pipeline capacity? Uh oh.

Listen, Doc, about the future...