The summer of 2024 proved somewhat melancholy for natural gas bulls, but also for bears, as front-month futures have consistently sported a $2 handle on the vast majority of trading days. What happened to the dire predictions of oversupply heard this past winter? And what about the bullish swing that took over the market in early June? Developments in production and weather have ameliorated both concerns but new issues may cause volatility to return in the near future. In today’s RBN blog, we’ll detail what happened during this summer’s gas market and what current trends portend for the fall and winter.

Join us at our historic 20th School of Energy!

School of Energy: Foundations is a two day, in person conference designed to help energy professionals better understand the forces shaping crude oil, natural gas, NGLs, refined products, and petrochemicals.

Attendees will learn from RBN experts, work with Excel based analytical models, participate in Q&As, and network with industry peers.

Build the foundation to better navigate volatile energy markets.

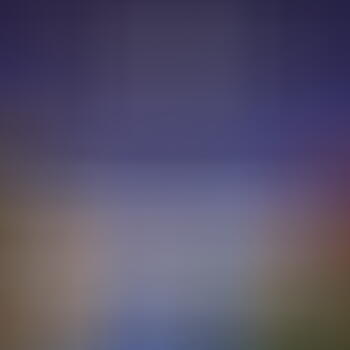

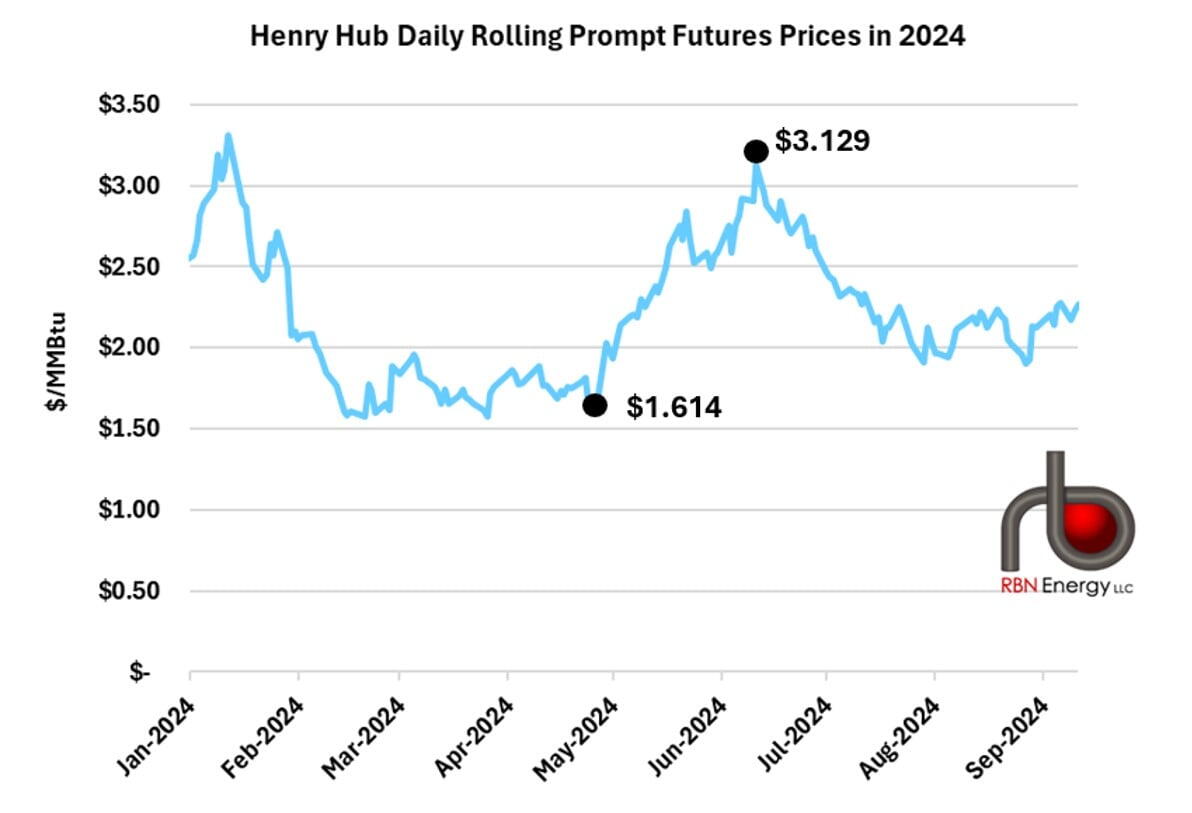

The domestic gas market was heavily oversupplied at the beginning of 2024. A historically mild winter was just wrapping up, and the initial start date for ExxonMobil and QatarEnergy’s Golden Pass LNG was pushed back for the first time. In the face of this slackening demand, production soared to unseen levels, hovering above 105 Bcf/d for most of early February. The loose gas balance (see Heat of the Moment) precipitated a sell-off in gas futures in February and the market languished in the doldrums below $2/MMBtu for much of the spring. However, shortly after the May contract reached final settlement at $1.614/MMBtu on April 26 (see Figure 1 below), market bulls became emboldened as producer discipline started to kick in. Predictions of hot summer weather also roiled the market and the front-month contract briefly surged as high as $3.129/MMBtu on June 11. But the bulls, too, would end up disappointed once summer truly got underway.

Figure 1. Prompt-Month Futures Prices. Source: CME

We’ll start our look back by focusing on production. Dry gas production in the Lower 48 averaged 102 Bcf/d in June, roughly 0.3 Bcf/d lower than the prior year’s June average — evidence of the successful pullback orchestrated by several major producers during the oversupplied winter period. Gas production in July came in nearly identical to the previous year’s figure, but by the time August rolled around production was 1.5 Bcf/d lower year on year. However, this was not the result of production declines during this summer — total dry gas production averaged just above 102 Bcf/d in June, July and August. Instead, it was the previous year’s upward slope of production that was not replicated, as upstream firms in 2023 had retained their optimism in the aftermath of 2022’s high-price environment. So the 0.6 Bcf/d year-on-year production change shown in Figure 2 below was created entirely by August’s deficit.

About the song

“Summertime Sadness” was written by Lana Del Rey and Rick Nowels and appears as the 11th song on Lana Del Rey’s second studio album, Born to Die. The pop ballad was released as a single in June 2012. The house remixes of “Summertime Sadness” helped put the song at #1 on the Billboard Hot Dance Club Songs Singles chart. In 2013, a remixed version of the song by Cedric Gervais went to #6 on the Billboard Hot 100 Singles chart, Del Rey’s highest charting single in her career. Gervais’ remixed version won a Grammy Award for Best Remixed Record, Non-Classical, in 2014. A video shot at various locations around Los Angeles by director Kyle Newman accompanied the release of the single. It has been certified 8x Platinum by the Recording Industry Association of America. Personnel on the record were: Lana Del Rey (vocals), Emile Haynie (keyboards, drums), Dan Heath (flute), Devrin Karaoglu (drum programming), and Patrick Warren, Rick Novels (strings).

Born to Die is the second studio album by Lana Del Rey. It was recorded between 2010-11 at Electric Lady and The Cutting Room in New York City and produced by Emile Haynie, Robopop, Jeff Bhasker, Al Shux, and Rick Nowels. Released in January 2012, it went to #2 on the Billboard 200 Albums chart and has been certified 5x Platinum by the RIAA. Six singles were released from the LP.

Lana Del Rey (Elizabeth Woolridge Grant) is an American singer and songwriter. She has released ten studio albums, two EPs, and 39 singles. She has sold more than 130 million records worldwide, making her one of the most successful alternative artists in the world. She has won two Brit Awards and an MTV Video Music Award. She continues to record and tour. Her next studio album, Lasso, is her first foray into country music and is due to be released in late September.