The Federal Reserve cut interest rates three times last year, brightening the prospects for continued economic growth and increases in energy demand, and additional rate cuts could be coming in 2025. But what do lower borrowing costs really mean for E&Ps, midstream companies, refiners and others in the energy industry? In today’s RBN blog, we will examine the impact of lower interest rates on energy companies and whether they might affect plans to boost output and build new infrastructure.

Canadian crude output is rising, requiring new export routes. As traditional pathways face constraints, the U.S. Rockies—especially the Guernsey, WY hub—are emerging as key corridors for moving Canadian heavy crude to downstream markets, including the Gulf Coast.

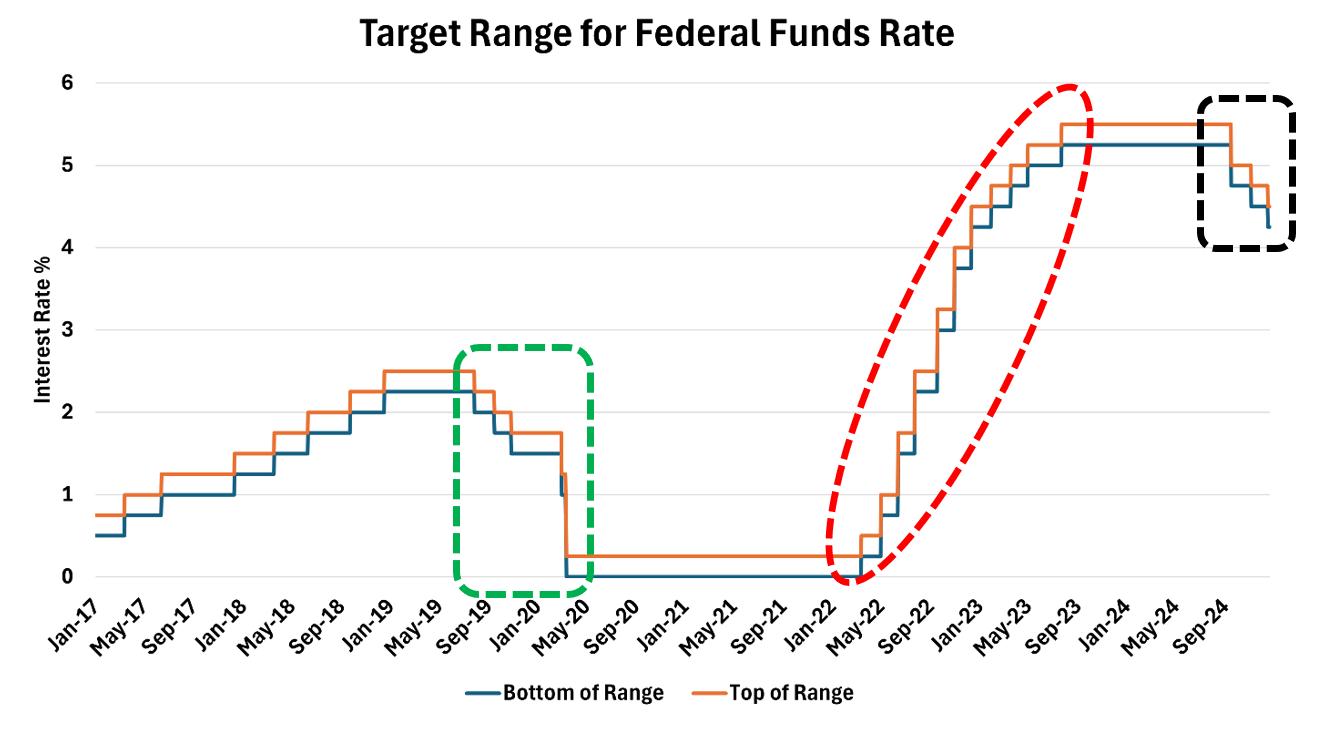

Before we dive in, let’s take a minute to discuss interest rates and why they shift over time. The U.S. central bank, or Federal Reserve (commonly known as the Fed), has a dual mandate: maximize employment and keep inflation low (ideally at 2% or less). The Fed sets what’s known as the Federal Funds Rate (FFR), a key short-term interest rate — typically a range of 0.25% or 25 basis points — primarily used by banks when lending to one another. (The orange and blue lines in Figure 1 below indicate the top and bottom of the ranges, respectively, beginning in 2017.) The FFR influences the so-called prime lending rate, the percentage that commercial banks charge their most creditworthy customers. Loans to the energy sector can be tied to both the FFR and the prime rate. And since many oil and gas projects rely on external funding — whether from banks or other financial institutions — any move by the Fed is closely watched.

Figure 1. Target Range for Federal Funds Rate. Source: Federal Reserve

The Fed adjusts the FFR based on a wide range of economic indicators. It decreased the rate as the pandemic hit to help buoy the economy (dashed green box), then increased the rate several times in 2022 and 2023 (dashed red oval) to help bring down inflation without sending the economy into a recession — the goal being a so-called “soft landing.” The 50-basis-point cut in the FFR to 4.75%-5% in September, followed by a reduction to 4.5%-4.75% in November and 4.25%-4.5% in December (dashed black box), basically informed the market that borrowing costs across the business community were finally beginning to decrease.

About the song

“Opportunities (Let’s Make Lots of Money)” was written by Neil Tennant and Chris Lowe and appears as the third song on side one of Pet Shop Boys’ debut album, Please. It was originally released as a single in July 1985 but re-recorded and re-released in 1986, where it went to #3 on the Billboard Dance Club Songs and #10 on the Billboard Hot 100 Singles charts. The song was originally recorded by Tennant and Lowe when they were in the formative years of Pet Shop Boys at a London studio in Camden Town in 1983. The song was later used in an American reality television show, Beauty and the Geek, and for a television commercial for Allstate that ran during Super Bowl LV in 2021. Personnel on the record were: Neil Tennant (vocals, keyboards), Chris Lowe (sequencer, synthesizer, keyboards, sampling, drum programming), and Stephen Hague (keyboards, programming).

Please was recorded between August 1985 to January 1986 at Advision in London with Stephen Hague producing. Released in March 1986, it went to #7 on the Billboard 200 Albums chart and has been certified Platinum by the Recording Industry Association of America. Four singles were released from the LP.

Pet Shop Boys are an English synth-pop duo formed in London in 1981 by Neil Tennant and Chris Lowe. They have released 15 studio albums, five live albums, five soundtrack albums, five compilation albums, four EPs, and 79 singles. They have sold more than 100 million records worldwide. They have won two ASCAP Pop Music Awards, three Brit Awards, and two Ivor Novello Awards. They continue to record and tour and released their latest album, Nonetheless, in April 2024.