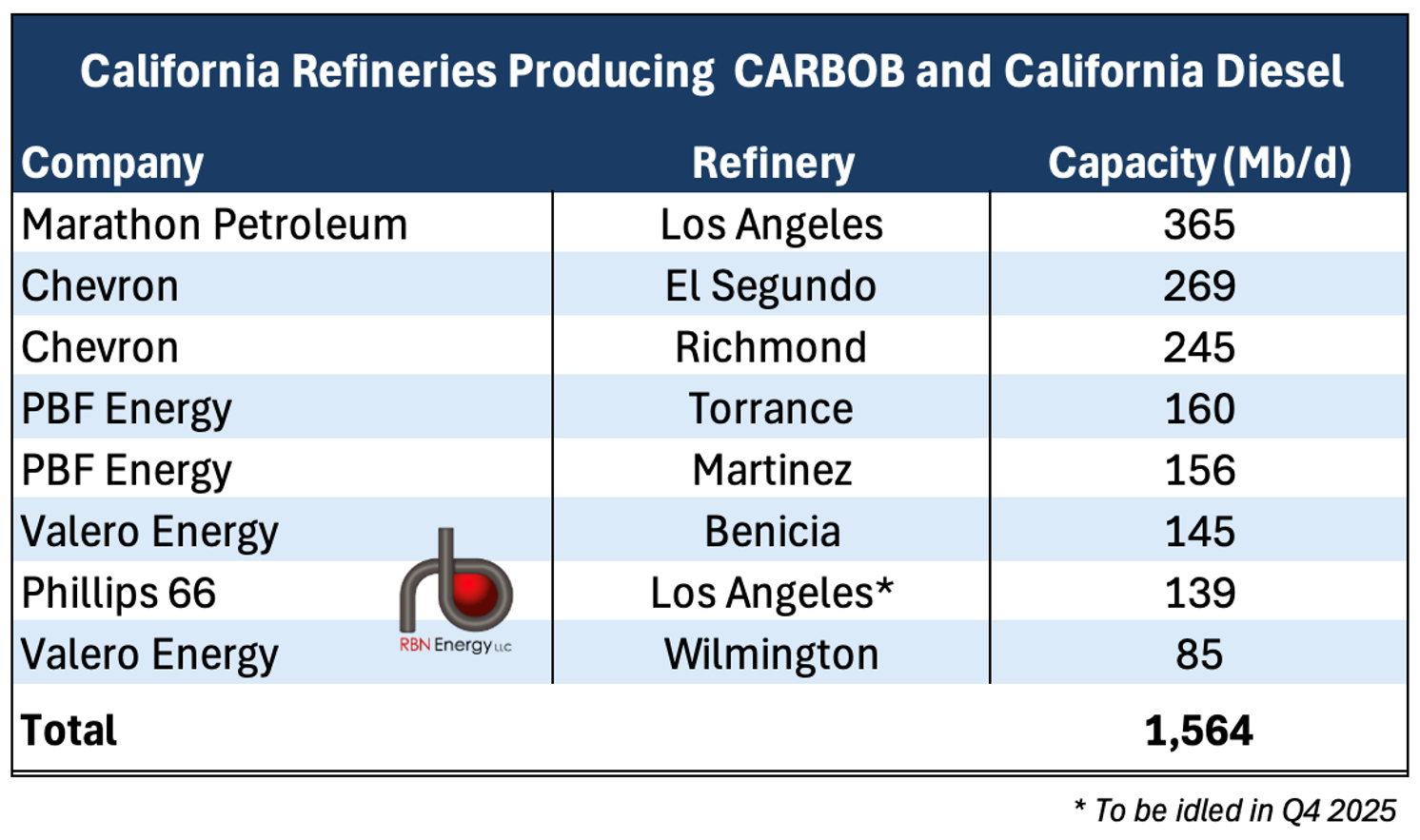

Weak refining margins, rising regulatory compliance costs, softening demand for gasoline and the push for lower-carbon alternatives like batteries and renewable diesel have each contributed to a steady decline in California’s refining capacity the past few years. Now, Phillips 66’s plan to idle its 139-Mb/d Los Angeles Refinery in Q4 2025 will leave the Golden State with only seven conventional refineries producing gasoline, diesel and jet fuel — a couple of dozen fewer than it had 40 years ago. In today’s RBN blog, we’ll put P66’s recent announcement in context and discuss the likelihood of additional refinery closures.

The Future of Fuels bi-annual report by RBN's Refined Fuels Analytics provides an in-depth analysis of the U.S. and global refinery industries, focusing on crude oil and fuel market dynamics, supply and demand, alternative fuels, refinery capacities, and price forecasts to help stakeholders navigate the evolving energy landscape.

California’s refining sector — and the state’s ambitious efforts to decarbonize its economy — has been a frequent topic in the RBN blogosphere. Most recently, in I Asked For Water (She Brought Me Gasoline), we discussed the many ways that California is a refining/refined-products market unto itself, with special circumstances and a definite tilt against fossil fuels. Consider this:

- Three-quarters of the crude oil refined there is shipped in — 14% from Alaska and 61% from foreign sources (mostly Iraq, Saudi Arabia, Brazil, Ecuador, and, since the startup of TMX, Canada) — with only 25% coming from in-state wells. This is a major disadvantage vs. refiners in most of the rest of the U.S. (with the exception of the East Coast), which have benefited significantly from the boom in domestic production, and is a major shift from a few decades ago when California crude production was more than triple current levels.

- Service stations can only sell the state’s unique gasoline blend, known as California Reformulated Gasoline Blendstock for Oxygenate Blending (CARBOB), which meets the state’s tougher clean-air requirements.

- There are no refined-products pipelines that connect the state’s northern and southern population centers, and no pipelines that deliver gasoline into California from other states.

- The state’s Low Carbon Fuel Standard (LCFS), which incentivizes the production of renewable diesel, biodiesel and other lower-carbon transportation fuels, has been trimming demand for conventional diesel, meaning the large majority of diesel produced by California refineries must be exported, mostly to the west coast of Mexico and Latin America.

Add to that the fact that California has more electric vehicles on the road today (about 1.25 million at last count, according to the U.S. Department of Energy) than the next eight states combined and a law requiring that all new cars and light trucks sold in the state in 2035 and beyond be zero-emission vehicles (ZEVs) such as battery-electric and hydrogen fuel cell vehicles. And, while it was not a factor in P66’s decision to shut down its Los Angeles Refinery, there’s California’s Assembly Bill X1-2 (AB X1-2, aka the California Gas Price Gouging and Transparency Law), which, among other things, authorizes the California Energy Commission (CEC) to set a maximum gross gasoline margin (and a penalty for refiners that exceed it) and establish a requirement that refineries stockpile specified volumes of gasoline to minimize the risk of fuel shortages.

Figure 1. California Refineries Producing CARBOB and California Diesel. Source: EIA

About the song

“It’s Time to Go” was written by Taylor Swift and Aaron Dessner and appears as the 17th song on Taylor Swift’s Deluxe Edition of her ninth studio album, Evermore. Swift has stated that the song is about listening to your gut when it is time to leave. The song is rumored to be about Scott Bordetta from Swift’s label of 15 years — he didn't give her the option to own her old catalog despite her wishes to do so, leading her to re-record most of her earlier works. Personnel on the record were: Taylor Swift (vocals), Aaron Dessner (drum machine, keyboards, guitars, bass, synth bass, orchestrations), Brian Devendorf (drum machine), Yuki Resnick (violin), Clarice Jensen (cello), Jason Treuting (chord stick), Thomas Bartlett (keyboards), J. T. Bates (drums, percussion), Kyle Resnick (trumpet), and Dave Nelson (trombone).

Evermore was recorded in 2020 at Kitty Committee and Ariel Rechtshaid’s house in Los Angeles; Long Pond Studio in upstate New York’s Columbia County; and Scarlet Pimpernel in Exeter, NH. Produced by Aaron Dessner, Taylor Swift, Jack Antonoff and Bryce Dessner, the album was released in December 2020. It went to #1 on the Billboard 200 Albums chart and has been certified Platinum by the Recording Industry Association of America. Three singles were released from the LP.

Taylor Swift is an American singer, songwriter and record producer. She is the highest-grossing female touring act and the richest female musician in the world. Her Eras Tour and its accompanying concert film are the highest-grossing tour and concert film of all time. Swift has released 11 studio albums, four live albums, 32 compilation albums, five EPs and 61 singles and has sold over 200 million records worldwide. She has won 39 Billboard Music Awards, two Brit Awards, eight ACM Awards, 12 CMA Awards, an Emmy Award and 30 MTV Video Music Awards and is a member of the Songwriters Hall of Fame. She continues to record and tour and nearing the end of her Eras Tour in the U.S. and Canada.