In the early 2000s, prices for West Texas Intermediate (WTI) were becoming increasingly disconnected from global fundamentals. WTI reflected conditions in the Midcontinent at the Cushing, OK, crude oil storage hub, where bottlenecks repeatedly distorted its value. In today’s RBN blog, we look at how the problem contributed to the creation of the Argus Sour Crude Index (ASCI) 16 years ago, how the index has evolved and whether it remains relevant today.

Analyst Insights are unique perspectives provided by RBN analysts about energy markets developments. The Insights may cover a wide range of information, such as industry trends, fundamentals, competitive landscape, or other market rumblings. These Insights are designed to be bite-size but punchy analysis so that readers can stay abreast of the most important market changes.

Transcontinental Gas Pipe Line was granted a crucial authorization last week, bringing the Northeast Supply Enhancement (NESE) one step closer to fruition. This project will allow the Williams Company pipeline to flow an incremental 400 MMcf/d to New York City and Long Island.

Waterborne crude oil exports from the expanded Trans Mountain Pipeline (TMX) averaged 453 Mb/d in September 2025 (rightmost stacked columns in chart below), a gain of 24 Mb/d versus August and an increase of 143 Mb/d from a year ago based on tanker tracking data compiled by Bloomberg.

On Friday, the Conway ethane (in E/P mix) price crashed to 13.5 cnts/gal. No this is not the Decline and Fall of Western Civilization (neither the actual event or the punk rock movie of that name), but it is an important development for NGL and natural gas markets. Six months ago the E/P mix price stood at 56 cnts/gal. That’s a 75% drop. Last week the price decline was particularly swift – 40% in five days.

With natural gas prices hanging at numbers around $2.50/MMbtu and possibly headed lower, there is a lot of talk about shut-ins. Presumably going out to the wellhead and turning off the valve. A couple of weeks ago, Jim Hackett, Anadarko CEO told a Rice University audience that “at current gas prices, gas operators can't sustain profitable domestic operations. By shutting in some of their wells, prices quickly would rebound.” Is that true? Is it a good idea?

“Prices have dropped to the lowest level in years. Pipelines are overbooked, and supplies are backing up. There is just not enough capacity to get out of the supply area and into the market area. Pipeline capacity is at a premium. The last time prices got to this level, producers shut in.”

It looks like OPEC has started to figure out that this shale thing might be a problem for them. The evidence? In the latest edition of OPECs bi-monthly bulletin, there is an article about the environmental risks of shale gas drilling in the north of England. OPEC? Environmental risk? Hmmm.

Over the past couple of years, the NGL market has cussed and discussed every nuance of PADD I ethane. The fear that ethane bottlenecks would curtail Marcellus drilling worried a lot of producers, and their investors. But it finally looks like the problem is being fixed, and the winners are settling out. MarkWest and Sunoco will take 50 Mb/d north to Sarnia, Ontario on Mariner West. And another 90 Mb/d will go south on Enterprise’s ATEX Express, the TEPPCO line reversal project. Chesapeake and Range have both signed up to move barrels on ATEX which runs from MarkWest`s Houston, PA plant down to the Enterprise storage complex in Mont. Belvieu. It’s nice to have one problem behind us. Unless of course it turns out that Utica ethane piles on to the top of Marcellus. But that’s another story.

Drilling and crude oil production in the Bakken has developed much faster than the gathering and pipeline infrastructure necessary to move the barrels. Consequently, over the past two years rail has become a significant feature of crude oil transportation in the region. According to the North Dakota Pipeline Authority, the capacity of rail terminals in the state was about 300,000 b/d at the end of 2011, and will reach 750,000 b/d this year. But there is a catch. The rail lines in North Dakota were not built for this kind of traffic.

Yesterday I attended the Argus Americas Crude Summit in Houston. Throughout the day the same theme kept repeating – “The times they are a changing”. Not only is the crude oil market trying to digest the implications of rapid growth in U.S. light-sweet crude and condensate production, it is also dealing with the Canadian oil sands saga, production growth across Latin America, new U.S. heavy crude conversion capacity, escalating Chinese demand, uncertain pipeline development schedules, the expanding role of rail transportation, the shut-down of East Coast refineries…. The list goes on. There was no shortage of topics for the presenters. In this blog I’ll summarize the high points of several of the most interesting presentations. Several speakers talked about condensates, so I will highlight that topic here.

We finally got that press release warning of shut-ins from Chesapeake, and it had the expected impact on price. Feb was up 18.2 cents to $2.525. The market was oversold and the smart money had gone long, so it was the perfect triggering event for a bump up. But as we said a couple of weeks ago in Shut In by Press Release, beware of producers bearing gifts. The economics of shut-in rarely make sense.

Natural gas prices are low. Really low. Really really low. The refrain has started to get tiresome. Yes it is a warm winter and yes shale production is high. We’ve all got that. The only question seems to be ‘Where is the bottom?’

Good article today in several newspapers (including the Chicago Tribune) from Jonathan Fahey at AP. “Cheaper natural gas gives American homeowners a break and helps manufacturers compete globally”. I talked to John last week on one of my last days at Bentek and provided several items he used, including the quote attributed to me at the end of the article “The most likely near-term scenario is that prices keep falling, according to Rusty Braziel, an analyst at Bentek Energy. This ain't the bottom," he says.

A couple of weeks ago we talked about the difference between the $4.14/MMbtu average price (HH) for natural gas storage injection in 2011 versus the average YTD withdrawal season price of $3.20 at the time ---$0.95 below the injection number. Now Feb futures have fallen below $2.70, or $1.44/MMbtu below the injection season value. So the implications then are even more true now – motivation for storage players to hold volumes in storage through the end of the withdrawal season, stronger possibility for 2 TCF remaining in storage at the end of the withdrawal season, etc.

Front page article today in the WSJ “Glut Hits Natural Gas Prices”. With front month futures hitting $2.774/MMBtu (lowest front-month price since Sept. 2009, lowest winter since 2002), and Henry Hub cash at $2.808/MMbtu), the non-energy world is finally starting to absorb the magnitude of the shale overhang. Heck, this would have happened in 2010 and 2011 if weather had not saved the day. This year, no weather and no save.

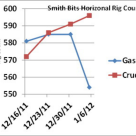

If you were looking for a sure sign that the shale phenomenon has shifted to crude oil, look no further than the Smith Bits rig count last week. These are horizontal-only numbers, split between the primary commodity target of the rig.

Yesterday Feb. natgas was up 10.3 cents at $3.096/MMBtu. Don’t get excited. This is just a minor blip due to weather and a little bit of crude sympathy. There is still a lot of gas out there.

Huge international companies are buying up all the hydrocarbon resources in North America. At least that's what it has looked like over the past few days. Total signed up with Chesapeake for a 25% interest in about 620M acres of Utica within a Cheapeake/EnerVest JV. Cost was $700MM plus a commitment to $1.6B of development (60%). Sinopec is ponying up $2.2B for an interest in 1.2MM of Devon's acreage in the Utica, Michigan Basin, the Mississippian, the Tuscaloosa marine shale and the Niobrara. Similar to Total, Sinopec will cover 70% of development costs - $1.6B by 2014. Finally PetroChina is buying the 40% of the MacKay River oil-sands prospect that it doesn't already own from Athabasca Oil Sands corp. Price is $680MM Canadian.