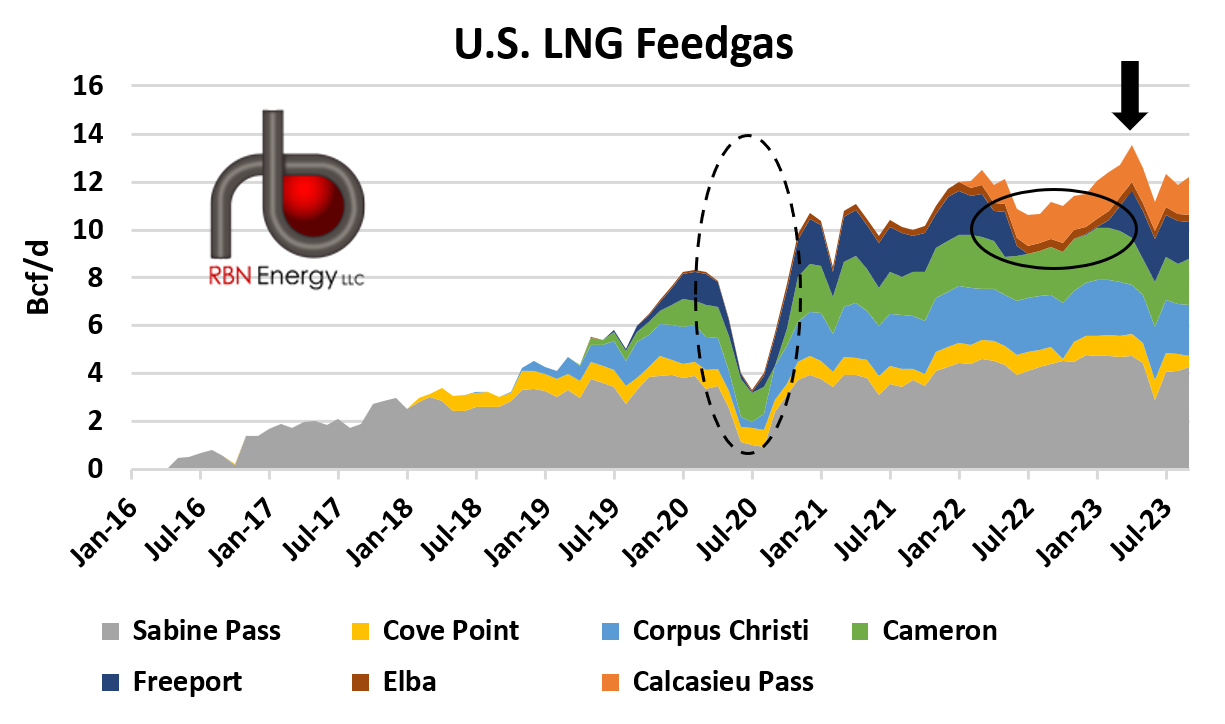

LNG feedgas demand has averaged a record of about 12 Bcf/d this summer and fall. While that may sound like an impressive number (and it is), it could increase significantly — even without new capacity additions — over the next few months as seasonal demand rises and maintenance activity slows. And that’s just for starters. Next year, the first of several planned LNG export terminals and expansions of existing ones will start commissioning, and by the end of this decade feedgas demand may well double. In today’s RBN blog, we look at how current LNG feedgas demand stacks up compared to past years, the factors driving current demand, and the potential for additional upside.

Visualize the infrastructure behind U.S. NGL movement.

The U.S. NGLs Map provides a comprehensive view of the transport, processing, and export networks moving NGLs across the U.S.

In the early years of U.S. LNG exports — from when Sabine Pass began operations in early 2016 through COVID’s arrival in early 2020 — feedgas demand for LNG climbed steadily. Nearly every month, a new feedgas record was set as an expanding fleet of LNG terminals came online. The pandemic stopped that growth in its tracks: feedgas demand peaked in February 2020 at 8.32 Bcf/d and then plummeted, averaging just 3.24 Bcf/d in July 2020 as more U.S. cargoes were canceled than exported (dashed black oval in Figure 1).

Figure 1. U.S. LNG Feedgas Demand by Terminal. Source: RBN LNG Voyager

About the song

“Feed Me” was written by Elton John and Bernie Taupin and appears as the third song on side two of Elton John’s 10th studio album, Rock of the Westies. The lyrics in the song seem to deal with John’s struggles with certain substances in the seventies (clean and sober for a long time now, he has helped several celebrities get on the path to sobriety). Personnel on the record were: Elton John (lead vocals), James Newton Howard (electric piano), Davey Johnstone, Caleb Quaye (electric guitar, backing vocals), Kenny Passarelli (bass), Roger Pope (drums), Ray Cooper (percussion), and Ann Orson (Elton John), Kiki Dee, Clive Franks (backing vocals).

Rock of the Westies was recorded between June-July 1975 at Caribou Ranch in Nederland, CO, and mixed at Trident in London, with Gus Dudgeon producing. The album didn't include John’s longtime drummer Nigel Ollson and bassist Dee Murray, both of whom John fired in April 1975. The album was released in October 1975 and debuted at #1 on the Billboard 200 Albums chart. It was John’s last chart-topping album to date. It has been certified Platinum by the Recording Industry Association of America. Two singles were released from the LP.

Sir Elton John (Reginald Kenneth Dwight) is a British singer, songwriter and composer. He learned piano at an early age and won a scholarship to the Royal Academy of Music in London, where he studied for five years. In 1967 he met lyricist Bernie Taupin, and for two years they wrote songs for other artists while John worked as a session musician. He released his debut album, Empty Sky, in 1969. He has released 31 studio albums, ten soundtrack albums, five live albums, 16 compilation albums, four EPs, and 140 singles. He has sold more than 300 million records worldwide, making him one of the best-selling artists of all time. He is a member of the Rock and Roll Hall of Fame, Songwriters Hall of Fame, has received a Kennedy Center Honor, a National Humanities Medal, A CBE, Legion of Honor, has a star on the Hollywood Walk of Fame, and was knighted by Queen Elizabeth II in 2020. He continues to record and finished his final world tour, the Farewell Yellow Brick Road Tour, in July 2023 in Stockholm, Sweden. He has stated that he will continue to do “the odd show” since his retirement from touring.