U.S. onshore crude oil production forecasts have skyrocketed in recent months, along with rig counts, current production and any other measure of activity you can think of. The big dogs are Bakken, Eagle Ford and Permian – all of which yield light-sweet crude or even lighter condensates. As outlined here last week in ‘You're doin' fine, Oklahoma’, forecasts for U.S. crude oil production can be classified as high, very high and extremely high. BENTEK is in the very high camp, expecting an increase of 2.2 Bcf/d between 2011 and 2016. Raymond James is poster child for the extremely high crowd, coming in at an incremental 3.5 Bcf/d by 2015. (RJ rounds up to 4.0 Bcf/d in some of their materials.). All of the forecasts have one thing in common. It is all light sweet crude oil. Not that gunky Canadian stuff that has so many protesters in a tizzy. …But clean, sweet smelling U.S. natural crude oil, made from the bodies of dead dinosaurs billions of years ago. (the one on the right)

The rapid growth in U.S. crude oil production is good news for just about everybody, with a few exceptions. Consider these four: (1) Refiners that are just completing huge capital expenditures to run more heavy Canadian crudes; (2) International importers of light sweet crudes into the U.S. Gulf; (3) Refiners that will be replacing those international imports with new U.S. light-sweet barrels; and (4) Refiners that are making most of their margin on diesel. The road is long, with many a winding turn - that leads us to who knows where. Let’s look at each of these issues to figure out where.

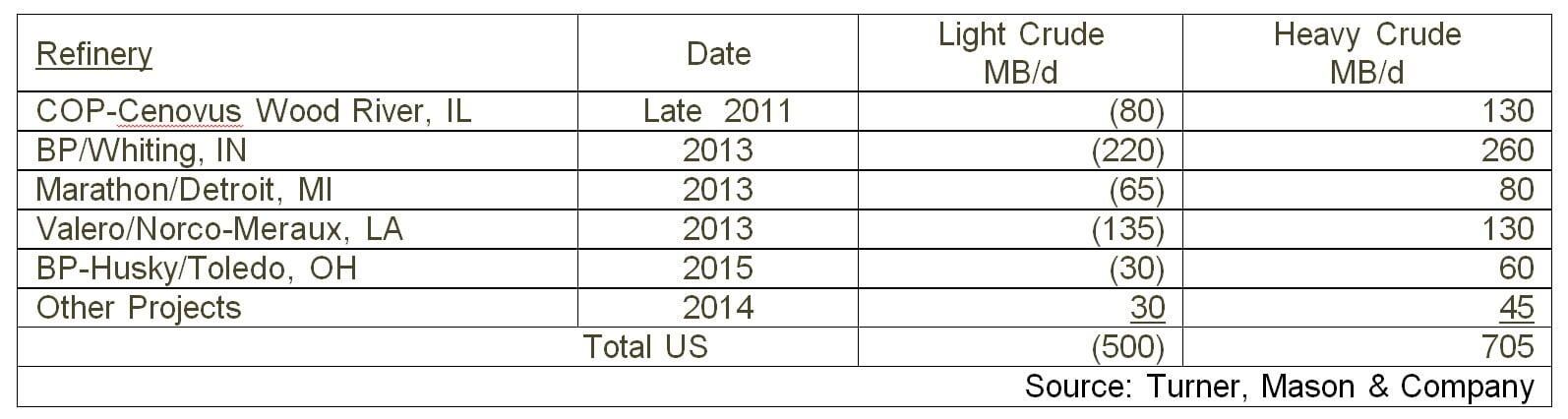

Exception #1 - Turning on a dime? That is not the modus operandi of refineries. It takes years to plan, design and build new crude oil refining units. That would not be a problem if the industry was not changing so quickly But it is. The following is a table presented by John Auers and Jim Jones from Turner, Mason & Company at the Platts’ North American Crude Marketing Conference last week in Houston. It details the heavy oil refinery expansions and the light crude capacity to be lost in the process.

This table says that the industry has added, or is adding 705 Mb/d of heavy crude capacity, while it is simultaneously reducing light crude capacity by 500 Mb/d. In other words, going in exactly the wrong direction based on the forecasts of light crude production referenced above.

It’s not the end of the world. There still will be significant increases in heavy Canadian imports over the next few years (Come on Keystone XL!) so all of these new units will not be sucking wind. But it does mean that there will be much more light crude supply at the same time demand for heavy crude is increasing. That can’t help but to narrow the differential between light and heavy crudes.

Refiners are willing to invest big dollars into heavy crude upgrading capacity because of the expectation that heavier, lower quality crudes will be cheaper (…defined as producing a given slate of products at a lower cost). If that is not true, it blows the economics of spending all those investment dollars in the first place. Sadly for some of these refiners, that is the most likely outlook for the light-heavy differential.

Exception #2. We don’t need you anymore. Domestic light sweet crude will displace waterborne imports into the U.S. Gulf over the next 3 to 5 years. This was the general consensus of all speakers that touched on the subject at the Platts conference. As described above, U.S. light sweet supply is up and demand is down. So it is only a matter of time before imports into the U.S. Gulf are backed out. Most of the displaced barrels come from Africa – primarily Nigeria and Algeria. The more interesting question is where there will be enough light crude to support exports – if exports were legal. This is another issue discussed briefly in the posting You're doin' fine, Oklahoma!

Exception #3. Oops. Let’s just turn off all that new heavy capacity and run lights instead. The Turner Mason table shows heavy crude capacity added and light crude capacity lost. But surely the refineries are not tearing out old equipment. If the ABC Refinery spent a billion or so putting in a new coker to run heavies, but heavies are not at a discount anymore, why not just shut it off? Unfortunately it doesn’t work that way. As explained by Jim Jones at Turner Mason, a refinery operates as an integrated whole. So if the crude distillation unit (that gets the crude before the heavy components are moved downstream to the coker) is tuned up to run heavies, if you fill the unit with light crude it will flood the top of the tower. In other words, more lights would cycle to the top end of the unit that it was designed (or had been modified) to handle. Consequently the refiner has two choices. Cut back capacity (something refiners are loath to do), or spend more money to re-retrofit the recent retrofit (something investors or loath to do). To use the famous comment of our current Texas governor – Oops.

Exception #4. I want my diesel back. Since we are talking about Oops, there is one last point to consider that was also illuminated by Jim Jones. The new crudes are light in another way. They are light on diesel yield. Bonny Light, one of the Nigerian crudes getting backed out of the Gulf Coast has kerosene (360-500 °F cut) and diesel (500-650 °F) yields at 20.8% and 24.8% respectively. For Bakken, the numbers are much lower at 14.7% and 14.3%. Condensates, which make up more than half of Eagle Ford production have even lower kero/diesel yields– well south of 5%. These numbers mean that refiners will be getting significantly less diesel out of the new crudes. Today refiners are making most of their money on diesel – so much so that the U.S. has become a net exporter of diesel, to Latin America and Europe. Declining distillate yields can’t be good news for the refiners who see this material coming. For this reason and others, it is entirely possible that distillate yields could become a primary determinant of future price differentials for different grades of crude oil.

The new crudes ain’t heavy. And brother, refiners will be dealing with that issue for years to come.

"He Ain't Heavy... He's My Brother" was written by Bobby Scott and Bob Russell in 1969. The song became a worldwide hit for The Hollies that year. It has been covered by Neil Diamond and countless other artists.

Comments

So why has the WCS negative differential (to WTI) blown out in the last few months?