More than 70 new data centers are under development in Virginia, which is already the world’s leading hub for the massive, high-tech facilities. But given the rapid pace of the buildout and the challenges that come with it, it’s probably no surprise that not everyone in the Old Dominion State is as enthusiastic about data centers as they once were. In today’s RBN blog, we’ll look at some of the biggest data centers in the works and discuss their path forward.

Analyst Insights are unique perspectives provided by RBN analysts about energy markets developments. The Insights may cover a wide range of information, such as industry trends, fundamentals, competitive landscape, or other market rumblings. These Insights are designed to be bite-size but punchy analysis so that readers can stay abreast of the most important market changes.

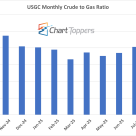

The monthly NYMEX crude-to-gas ratio for September 2025 stands at 21.4, where crude was $63.81/bbl and gas was $2.98/MMbtu, a slight decline from August’s 22.1.

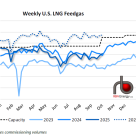

U.S. LNG feedgas demand averaged 15.4 Bcf/d last week (see blue-dotted line in figure below), up 0.1 Bcf/d from the previous week despite lower intake at Cove Point.

Taken together, the ethane-related infrastructure projects developed in the U.S. over the past several years serve as a reliable feedstock-delivery network for a number of steam crackers in Europe, Asia, and Latin America. NGL pipelines transport y-grade to fractionation hubs, fractionators split the mixed NGLs into ethane and other “purity” products, ethane pipelines move the feedstock to export terminals fitted with the special storage and loading facilities that ethane requires, and a class of cryogenic ships — Very Large Ethane Carriers, or VLECs — sails ethane to mostly long-term customers in distant lands. The end results of all this development are virtual ethane pipelines between, say, the Marcellus/Utica and Scotland, or the Permian and India. Today, we continue our series on ethane exports with a look at the two existing export terminals, the ethane volumes they have been handling, and where all that ethane has been headed.

If you’ve filled up the tank in your car, SUV, or pickup in the past few days, you probably bought your first batch of winter-blend gasoline since the spring. It’s unlikely that you noticed a difference — only a refining geek with a nose for this sort of thing would — but winter gasoline has a higher Reid Vapor Pressure than summer gasoline, and therefore evaporates more quickly and emits more fumes. There’s a logic to EPA’s mandated switchover from lower-RVP gasoline to higher-RVP gasoline each September, and their switch back to lower-RVP each April/May. For one thing, using different gasoline blends during the colder and warmer months helps ensure that your engine runs well year-round; for another, reducing gasoline vapor pressure in the summer reduces emissions that contribute to smog. Today, we discuss gasoline RVP, why it matters, and how refineries ramp it up and down. (A hint is in the blog’s title.)

In the past three years, two major commitments were made to construct propane dehydrogenation and polypropylene plants in Alberta to take advantage of the rising bounty and generally low cost of propane supplies in Western Canada. Two Calgary-based midstream companies, Inter Pipeline Ltd. and Pembina Pipeline, each started developing PDH-PP plants in Alberta’s Industrial Heartland area northeast of Edmonton. But then came COVID-19, which set back the timeline for one of the projects and put the other on ice. All this comes as Western Canada’s propane market is in greater flux than usual, and facing a tightening supply/demand balance as exports to Asia ramp up. Today, we provide a status check on the development of these two plants, and what the increase in demand might portend for propane balances in the next few years.

Battered by seismic economic shocks from sudden demand destruction and plummeting prices in the early days of the COVID-19 pandemic, exploration and production companies (E&Ps) abandoned their carefully crafted 2020 strategic plans and financial guidance and shifted into emergency survival mode to protect their financial stability. First-quarter earnings calls sounded more like FEMA disaster briefings than standard financial reporting as the companies announced aggressive capital and operational cost-cutting measures. But few E&Ps detailed the timing and duration of the investment reductions and the degree to which they would impact oil and gas production for the remainder of the year. Now, with second-quarter calls behind us and the third quarter about to end, there’s a lot more clarity on the capital spending and production fronts. Today, we discuss the evolution of E&Ps’ 2020 spending plans and how the changes will affect production for the balance of the year.

The run-up in U.S. production of natural gas liquids over the past 10 years spurred the development of a whole lot of infrastructure. More pipelines to transport mixed NGLs from production areas to NGL storage and fractionation hubs, especially Mont Belvieu, TX. More fractionators to split y-grade into ethane, propane, and other “purity” products. And, specifically for ethane — the lightest, quirkiest, and most plentiful NGL — a number of ethane-only steam crackers were built along the Gulf Coast to take advantage of the new supply abundance, as were ethane-only pipelines, export terminals, and a whole new class of cryogenic ships — Very Large Ethane Carriers, or VLECs — to move the product to markets in Europe and Asia. Today, we begin a new series on the unique nature of overseas ethane exports, including why most incremental export volumes are tied to long-term supply deals with a handful of global ethylene plants designed — or reconfigured — to “crack” ethane.

Canadian gas production in 2019 turned lower for the first time in half a dozen years as very weak benchmark Canadian gas prices led to a sharp reduction in drilling and wellhead shut-ins. This year, higher prices, more drilling, and greater pipeline egress capacity were supposed to set the stage for a return of supply growth. Instead, production volumes have slipped further due to reduced drilling activity and, more recently, a spate of maintenance work. And even if there is some improvement in the next few months, annual average production looks to be on track for a second consecutive decline in 2020. But what about next year? Today, we take a closer look at the recent supply trends and whether there are any signs pointing to a production rebound in 2021.

U.S. natural gas production in recent days has plunged more than 3 Bcf/d. While some Gulf of Mexico offshore and Gulf Coast production is still offline from the recent tropical storms, the bulk of these declines are happening in the Northeast, where gas production has dived 2 Bcf/d in the past week or so to about 30.2 Bcf/d, the lowest level since May 2019, pipeline flow data shows. Appalachia’s gas output was already down earlier in the month, as EQT Corp. shut in some volumes starting September 1. But with storage inventories soaring near five-year highs, a combination of maintenance events and demand constraints are forcing further curtailments of Marcellus/Utica volumes near-term. Today, we provide an update of Appalachia gas supply trends using daily gas pipeline flow data.

There’s no doubt about it: California’s decade-long efforts to expand the use of solar, wind, and other renewable energy and improve energy efficiency have enabled the state to significantly reduce its consumption of natural gas for power generation. But the Golden State’s rapid shift to a greener, lower-carbon electricity sector — and its push to shut down gas-fired power plants — has come at a cost, namely an increased risk of rolling blackouts, especially during extended heat waves in the West when neighboring states have less “surplus” electricity to send California’s way. The main problem is that while solar facilities provide a big share of the state’s midday power needs, there’s sometimes barely enough capacity from gas plants and other conventional generation sources to take up the slack when the sun sinks in the late afternoon and early evening. Today, we discuss recent developments on the power front in the most populous state, and what they mean for natural gas consumption there.

As U.S. natural gas spot and futures prices retreated in the past week, the price of gas at Appalachia’s Dominion South hub fell as low as $0.735/MMBtu, the lowest since fall 2017, before partially rebounding yesterday to about $1.10/MMBtu, according to the NGI daily gas price index. Moreover, the forwards market indicates sub-$1/MMBtu prices are in store for October as well. The regional supply hub didn’t weaken quite as much as prices at the national benchmark Henry Hub, which collapsed in recent days on demand losses — from cooler weather, storm-related power outages, and disruptions to LNG exports — and storage levels in the Gulf Coast region that are well above average and approaching peak capacity levels. The relative support for prices in the Northeast is in part due to a second round of production shut-ins by EQT Corp., which took effect September 1. But seasonal demand declines are underway; the Dominion Energy Cove Point LNG facility in Maryland just went offline for its annual fall maintenance, placing additional pressure on already-packed storage fields and takeaway pipelines; and pipeline maintenance events are reducing outflow capacity and curtailing production. Altogether, that signals more volatility ahead. Today, we provide an update on the fundamentals driving the Northeast gas market.

Western Canada’s relentless, decade-long increase in crude oil production began maxing out its export pipeline capacity in the past few years. With more supply than could be carried by pipelines, exporting crude by rail tank car became the next best alternative, leading to record amounts of rail-based exports earlier this year. However, this year’s wild swings in oil prices and COVID-led demand destruction resulted in drastic production cutbacks that freed up space on pipelines and put the kibosh on more expensive crude-by-rail, at least temporarily. Things are shifting again, though. With oil production recovering somewhat in the past couple of months and excess pipeline capacity dwindling, are we headed for a resurgence in the use of rail to export Canadian crude? Today, we conclude a series on Western Canada crude production and takeaway options with an analysis of what’s ahead for crude-by-rail.

No one in North America’s energy sector is likely to forget the second quarter of 2020 anytime soon. In those months — April, May, and June — the demand-destruction effects of the COVID-19 pandemic took root; the price of West Texas Intermediate (WTI) bottomed out, even going negative for a day; and crude oil-focused drillers in particular shut in vast numbers of wells. In late July and August, when exploration and production companies (E&Ps) announced their results for that train wreck of a quarter, it came as no surprise that the write-downs and losses were generally immense and, in many cases, record-shattering. But WTI prices have rebounded somewhat the past couple of months, as has production, suggesting that while E&Ps third-quarter results will be far from stellar, they’ll at least show an improvement and hopefully set the stage for further gains going forward. Today, we break down second-quarter results by producer peer group and discuss the positive trends that portend improved results for the third quarter.

In a normal year, the autumn months would be filled with the smell of brisket at a tailgate barbecue and the sound of college football fans cheering in their favorite team's stadium. But with the college football stadiums largely empty due to COVID-19, is there something that could fill the void? Well, maybe. The Bureau of Ocean Energy Management (BOEM) a couple months back issued a notice proposing Lease Sale 256 for oil and gas exploration of 78.8 million acres in the Gulf of Mexico (GOM). You will probably not be able to find the announcement of the lease sale on ESPN this November, but you will be able to tune into the livestream set in New Orleans. Today, we describe the process for bidding and acquiring lease acreage in the Gulf of Mexico.

The South Texas NGL market has always been a world of its own, a self-contained liquids ecosystem running from Brownsville to Markham, a distant 200 miles from the NGL epicenter at Mont Belvieu. In recent years, however, the South Texas market has been undergoing radical change, first with the emergence of the Eagle Ford basin, then with the onslaught of Permian production and, most recently, with the aptly named EPIC NGL Pipeline and new fractionation capacity in greater Corpus Christi. More supply and demand are on the way, with new pipes, exports, and the largest ethane-only petrochemical plant in the world under construction. And with these developments, a strategy by several large, well-financed players has emerged – to develop an NGL storage and fractionation hub competitive with Month Belvieu. Today, we begin a series to examine the South Texas NGL market and how changes there will impact flows, utilization, and pricing across North America and beyond.

The energy industry in North America is in crisis. COVID-19 remains a remarkably potent force, stifling a genuine rebound in demand for crude oil and refined products — and the broader U.S. economy. Oil prices have sagged south of $40/bbl, slowing drilling-and-completion activity to a crawl and imperiling the viability of many producers. The outlook for natural gas isn’t much better: anemic global demand for LNG is dragging down U.S. natural gas prices — and gas producers. The midstream sector isn’t immune to all this negativity. Lower production volumes mean lower flows on pipelines, less gas processing, less fractionation, and fewer export opportunities. But one major midstreamer, Enbridge Inc., made a prescient decision almost three years ago to significantly reduce its exposure to the vagaries of energy markets, and stands to emerge from the current hard times in good shape –– assuming, that is, that it can clear the major regulatory challenges it still faces. Today, we preview our new Spotlight report on the Calgary, AB-based midstream giant, Enbridge, which plans to de-risk its business model.

A combination of new-pipeline development, lower capex by producers, production shut-ins, and changing expectations for future production has significantly altered crude oil and natural gas market fundamentals in the all-important Permian Basin. Just over a year ago, Permian production was rising steadily and oil and gas pipelines out of West Texas were running at or near full capacity. Since then, nearly 2.2 MMb/d of incremental crude takeaway capacity has come online, and production dropped by about 700 Mb/d before rebounding somewhat in recent weeks. As for gas, some takeaway constraints remain, but they are limited to when pipelines are offline for maintenance, and will be alleviated when new pipelines start operating in 2021. Today, we discuss the recent downs and ups in Permian production, takeaway capacity additions, and the resulting impacts on markets and market participants.