More than 70 new data centers are under development in Virginia, which is already the world’s leading hub for the massive, high-tech facilities. But given the rapid pace of the buildout and the challenges that come with it, it’s probably no surprise that not everyone in the Old Dominion State is as enthusiastic about data centers as they once were. In today’s RBN blog, we’ll look at some of the biggest data centers in the works and discuss their path forward.

Analyst Insights are unique perspectives provided by RBN analysts about energy markets developments. The Insights may cover a wide range of information, such as industry trends, fundamentals, competitive landscape, or other market rumblings. These Insights are designed to be bite-size but punchy analysis so that readers can stay abreast of the most important market changes.

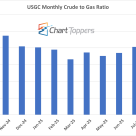

The monthly NYMEX crude-to-gas ratio for September 2025 stands at 21.4, where crude was $63.81/bbl and gas was $2.98/MMbtu, a slight decline from August’s 22.1.

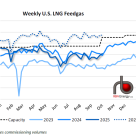

U.S. LNG feedgas demand averaged 15.4 Bcf/d last week (see blue-dotted line in figure below), up 0.1 Bcf/d from the previous week despite lower intake at Cove Point.

Down to only two months left in 2020. Whew! We’ll all be relieved to see this one disappear in the rear-view mirror. It’s been an extreme roller coaster ride for oil and gas — from the onset of the COVID pandemic and the crude price collapse in the spring, to withering demand for transportation fuels, to one hurricane after another, to chaotic swings in natural gas prices. And being thrashed about by all this turmoil are the natural gas liquids, with each NGL product taking its own wild ride through erratic market conditions. It’s been a challenge just keeping up with what is going on. At RBN, we’ve been working on a new app to address this challenge, and today we are rolling it out to you, as a reader of our daily blog. We are talking about access to everything from spot and futures prices, to market statistics, to reports on intra-day pricing, and to market alerts as they happen. Sound interesting? If so, hang on to your hat and read on in this RBN product advertorial.

Over the past decade, floating LNG — for liquefying and shipping offshore natural gas supply — emerged as a promising technology that would enable development of smaller, more remote offshore gas fields around the world. But with a handful of projects now completed and in commercial operation, the challenges of financing, developing, and operating this relatively new technology are overshadowing its prospects. Of the more than 20 FLNG projects that have been proposed since 2007, only five have crossed the finish line and only two others have reached a favorable final investment decision (FID). Moreover, Shell’s Prelude FLNG offshore Northwest Australia — the largest of the existing FLNG facilities — has been dogged by issues since its commissioning in mid-2019, and the operator last week said the unit will not produce any more LNG cargoes this year, after being shut down since February for electrical problems. Today, we examine the headwinds facing FLNG projects.

For the past few years, demand for U.S.-sourced ethane has been on the rise as petrochemical companies in the U.S. and abroad developed new, ethane-only steam crackers and retrofitted existing crackers to allow more ethane to be used as feedstock. U.S. NGL production was increasing too, of course, alongside growth in crude oil-focused plays like the Permian and “wet” gas plays like the Marcellus/Utica. But recently, drilling-and-completion activity has slowed to a crawl and NGL production has been leveling off, which means that less of the ethane that comes out of the ground with oil and gas will be “rejected” into natural gas and more will be separated out at fractionation plants. Today, we conclude a series on ethane exports with a look at U.S. NGL production, ethane supply and demand, ethane exports, and ethane prices.

Much has been written about the run-up in U.S. crude oil exports over the past five-plus years, and rightly so. Who would have guessed a dozen years ago that the U.S. would soon be producing as much as 13 MMb/d, and exporting one-quarter of it? Exports are only half of the story though. In fact, for every barrel of crude shipped or piped out of the U.S. today, two barrels of crude are shipped, piped, or railed in. Put simply, the U.S. refining sector still needs imported oil — or, more accurately, it can’t use all of the light, sweet crude that’s produced in the Permian and other shale/tight-oil plays in the Lower 48, and it still requires large volumes of the heavier crude that’s produced in Canada, Mexico, and overseas. Today, we begin a blog series on U.S. oil imports with a big-picture look at how crude sourcing for the refining sector has morphed in the Shale Era.

By the middle of the decade, LNG Canada should be sending its first cargoes of Canadian-sourced LNG to Asian markets. More importantly, Canada for the first time will have an alternative export market for its natural gas supplies — for more than 50 years, piping gas south to the U.S. has been its only option. But getting gas from the Montney and Duvernay production areas to the British Columbia coast is no easy task. It requires the construction of an entirely new, 2.1-Bcf/d pipeline — expandable to 5 Bcf/d — much of it over very rugged terrain. Coastal GasLink, as the planned pipe is known, has also faced major regulatory hurdles. Today, we conclude a two-part series with a look at where the pipeline project stands today.

The Permian is set to send increasing volumes of natural gas to the Texas Gulf Coast next year, but it is unlikely to be the flood that was once expected. This year’s decline in oil prices has slashed budgets for West Texas producers and rig counts show no sign of a big rebound anytime soon. As a result, growth of oil and associated gas from the Permian will be tepid at best over the next few years, which is a major change from when oil prices hovered north of $50/bbl. Despite the moderation in gas volumes out of the basin, infrastructure changes in 2021 are likely to roil Permian gas markets and have important knock-on impacts for adjacent regions and end-users that depend on West Texas supply. With much less incremental gas from the Permian, there are likely to be significant shifts in gas flows, particularly across the Texas-Louisiana border, to help meet the big increases anticipated for LNG exports. Today, we continue a series that highlights findings from RBN’s new, Special Edition Multi-Client Market Study.

Last week, Hurricane Delta became the latest of a string of hurricanes and tropical storms that have assaulted the Gulf Coast this year and disrupted energy production in the Gulf of Mexico — and energy exports. A number of major storms made direct hits or glancing blows to crude export centers like Corpus Christi, Houston, Beaumont, and Louisiana, forcing marine terminals to either slow down their carrier-loading operations or shut down for a few days at a time. That led to a yo-yoing of weekly export volumes: way down one week, way up the next. Despite the short-term dislocations, however, total export volumes since the hurricane season started on June 1 are actually up slightly from the first five months of 2020, a testament to the resilience not only of the export market but to the marine terminals themselves. Today, we discuss how hurricanes and tropical storms have been affecting export-terminal activity.

With the rise of U.S. LNG exports in recent years, southern Louisiana has become a focal point for natural gas demand, pulling in gas supply from near and far and all directions. That market was severely disrupted this summer as COVID-19 decimated global LNG demand and hammered the economics of U.S. LNG exports. Pipeline flows into southern Louisiana during those months went from record-breaking highs that pushed the limits of the area’s infrastructure capacity to levels consistent with 2018, when the Bayou State’s LNG export capacity was just 2.65 Bcf/d, compared with 4.9 Bcf/d now. More recently, an active hurricane season has also curtailed exports. But demand for U.S. LNG is rebounding, and as LNG feedgas heads back to its previous highs and beyond, a new flow dynamic is emerging along the Gulf Coast, driven by the 1.35 Bcf/d of new export capacity in Texas that came online this year. Flows between Louisiana and Texas are reversing as an increasing amount of gas is needed on the western side of the Sabine River to feed the Corpus Christi and Freeport LNG facilities. The incremental gas demand and flow reversal will create new challenges and constraints for the region’s pipeline infrastructure as steady exports resume. Flows into Louisiana will be higher than ever, but so will flows out of Louisiana heading west to serve additional LNG demand. Today, we begin a series discussing how LNG demand is changing gas flows along the U.S. Gulf Coast.

Six months on from the height of the crude oil price rout of April 2020 and the unprecedented market convulsions that followed, energy markets appear to be settling into a state of hyper-uncertainty amidst the ongoing pandemic. Crude oil prices have been downright equanimous, stabilizing near $40/bbl in recent months. Volatility has reigned in the gas market, but it has thus far managed to avoid a major collapse, and the NGLs market has dodged a complete derailment from norms, if barely. The relative calm provides the perfect opportunity to assess how COVID-era energy markets are operating and what lies ahead — which is what we’ll be doing next week at RBN’s Virtual School of Energy. There’s a new order taking shape, and we’re rolling out RBN’s freshly updated outlooks for U.S. crude oil, natural gas and NGL markets. As always, we’ll pull back the curtain on the fundamental analysis and models behind our forecasts, so you can understand how we arrived at our answers, and gain the skills and tools to adjust the assumptions as markets evolve. As you’ve gathered by now, today’s blog is an unabashed advertorial for our virtual conference, but read on if you’d like to hear more about the underlying premise behind our latest outlook.

Global LNG demand has picked up, cancellations for U.S. cargoes have subsided, at least for now, and there’s upside to U.S. cargo activity once tropical storm-related disruptions are resolved. But positive netbacks year-round are no longer a foregone conclusion for U.S. offtakers. As global oversupply conditions persist, at least on a seasonal basis, and supply competition intensifies, the economic decision to lift U.S. cargoes will be much more nuanced than it was in previous years. What do the economics for cargoes this winter and beyond look like? Today, we put the LNG economics model to work to understand what’s in store for U.S. LNG in the coming months.

Permian natural gas production is now expected to grow at a subdued pace over the next five years, as lower oil prices and a focus on capital discipline have slashed rig counts. Few observers see the Permian situation changing anytime soon, especially as crude oil prices continue to hover around $40/bbl. That said, the Permian gas market will be anything but dull over the months and years ahead. More than 4 Bcf/d of new outbound pipeline capacity from the Permian to the Gulf Coast will be coming online next year, throwing natural gas flows from West Texas into flux and deeply impacting neighboring markets. While natural gas basis at the Permian’s primary Waha hub should improve dramatically, outflow to the Midcontinent will likely fall sharply and potentially reverse, and the Texas Gulf Coast will see an influx of supply on the new pipelines. Today, we continue a series that highlights findings from RBN’s new, Special Edition Multi-Client Market Study.

The U.S. is by far the world’s largest ethane producer, and exports one-seventh of what it produces, with most of the exported volumes tied to long-term contracts to supply ethane-consuming steam crackers. Canada is the #1 importer of U.S. ethane, receiving its volumes via three pipelines. As for U.S. exports by ship, India is on top, followed by the UK and Norway. But watch out! China, which started importing U.S. ethane a year or so ago, is poised to buy a heck of lot more, with most of the incremental volumes to be shipped out of a new ethane export terminal about to come online in Nederland, TX. Today, we continue our series with a look at the Orbit Ethane Export Terminal, which is being jointly developed by Energy Transfer and Satellite Petrochemical, the U.S. subsidiary of a Chinese petrochemical company.

When plans for LNG Canada, a big LNG export project on the British Columbia coast, were sanctioned two years ago this month, the move came as a welcome sign that Western Canadian natural gas producers might finally be able to break their long-standing reliance on just one export customer: the U.S. Access to Asian and other overseas gas markets became a high priority, in part because U.S. demand for Canadian gas had been sagging for years as production in the Marcellus/Utica and other U.S. plays came to meet the vast majority of domestic needs. But while construction on LNG Canada has steadily advanced, there are signs that delays could be mounting. Today, we begin a two-part update on this all-important Canadian LNG export project and its accompanying Coastal GasLink pipeline.

Tough times in the crude oil sector generally affect all participants to some degree, but the impacts can vary widely by production basin. We saw that back in 2014-16, when the crash in oil prices battered the Eagle Ford, Bakken, and Niobrara but left the Permian unscathed — production there actually kept rising. Fast-forward to 2020, with its COVID-induced demand destruction, anemic prices, and uncertain-at-best recovery, and again the Bakken really took it on the chin. Production in the basin plummeted by 28% in one month — from April to May — and while Bakken output rebounded this summer, the rig count has been hovering at its lowest level in memory and another, albeit slower production decline may be imminent. Today, we discuss the challenges facing exploration and production companies in western North Dakota.

Expectations for Permian natural gas are far from what they were when this year started. Lower crude oil prices and a focus on capital discipline have slashed rig counts by about two-thirds since January and there are few signs of a recovery on the horizon. As a result, just about everyone’s forecast for Permian gas growth is much lower than just a few months ago, with tepid gains through the early 2020s now the industry’s consensus view. However, if you think all this means that Permian gas markets have lost their relevance, think again. Despite the modest production growth anticipated, the basin’s gas flow patterns will soon be thrown into shock as 4 Bcf/d of new outflow capacity to Gulf Coast markets starts up next year, when the Permian Highway and Whistler pipelines begin operation. And that shock will reverberate through regional basis relationships, including at the Waha Hub, which we expect to end 2021 much stronger than it is currently. Today, we begin a series that looks at Permian, as well as Gulf Coast, gas markets over the months and years ahead, highlighting findings from RBN’s new, Special Edition Multi-Client Market Study.