It’s well understood today that the U.S. natural gas market turned from potential domestic shortages to major LNG exports thanks to the Shale Revolution. What is not so well remembered is that the dramatic shift in the U.S. gas market wasn’t widely understood at the time and took several years to be accepted by the energy industry. In today’s RBN blog, we turn our attention to the beginnings of the Shale Revolution and how it allowed the U.S. to evolve into the world’s largest LNG exporter.

Analyst Insights are unique perspectives provided by RBN analysts about energy markets developments. The Insights may cover a wide range of information, such as industry trends, fundamentals, competitive landscape, or other market rumblings. These Insights are designed to be bite-size but punchy analysis so that readers can stay abreast of the most important market changes.

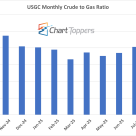

The monthly NYMEX crude-to-gas ratio for September 2025 stands at 21.4, where crude was $63.81/bbl and gas was $2.98/MMbtu, a slight decline from August’s 22.1.

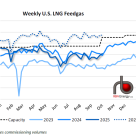

U.S. LNG feedgas demand averaged 15.4 Bcf/d last week (see blue-dotted line in figure below), up 0.1 Bcf/d from the previous week despite lower intake at Cove Point.

To succeed over the long term in the music business, professional sports, or the midstream sector, you need to learn from your successes and failures, and — most important — continue adapting and evolving. For many North American midstreamers, a key to success has been a thoughtful combination of expansion and diversification, plus an affinity for financial discipline, especially when the broader energy industry is going through tough, uncertain times. A prime example of that strategy is Canadian midstreamer Pembina Pipeline Corp., which after C$14 billion in acquisitions over the last four years is instituting a more cautious approach to new investment that’s largely based on self-funding and a new, more rigorous return criteria for new projects. Today, we preview our new Spotlight report, which focuses on the risks and rewards of Pembina’s new strategy.

Cushing. This small town in central Oklahoma is the center of the U.S. crude oil universe, with prices at the Cushing hub serving as the reference price for all of the crude produced in the U.S. — and given the role that U.S. oil has assumed on the global stage, one of the most important determinants of global crude oil pricing. Considering the hub’s significance, it’s frequently surprising to industry veterans just how misunderstood Cushing can be. Like, for example, how SHOCKED the world was when Cushing prices dropped below zero back in April. Cushing traders had seen that coming for weeks — the only surprise to them was how far the price plunged that crazy Monday morning. It’s easy to see how something as enigmatic and complex as Cushing might be misunderstood — or underestimated — if you’re not familiar with its history, its inner workings, and its many crucial roles in both the physical and financial crude oil markets. It’s also tempting to think you can get by with only a passing knowledge of Cushing and how it operates. Au contraire! Cushing really matters, and market participants ignore it at their peril. The good news is that there’s finally a combo encyclopedia and user’s manual for “The Pipeline Crossroads of the World.” Today, we examine the hub’s significance to producers, refiners, midstreamers, marketers, and traders, and discuss highlights from RBN’s new Cushing Playbook.

PADDs 4 and 5 — the Rockies and the West Coast regions, respectively — are each outliers in the U.S. refining sector. Refineries in the Rockies, for example, are generally far smaller than those in other PADDs and, due to pipeline flows, source their crude oil from either Western Canada, the Bakken, or in-region production, including the Niobrara and Utah’s Uinta Basin. West Coast refineries, in turn, have no crude oil pipeline links with U.S. points to the east, and depend on a mix of imported crude from Canada, Latin America, and the Middle East, as well as domestic oil from California, Alaska, and rail receipts. Today, we conclude a series on region-by-region crude oil imports and refinery crude slates with a look at PADDs 4 and 5.

No one could’ve seen the energy market disruptions of 2020 coming, and most of us are ready to write off what has been one of the most challenging years the industry has seen in a long time. Yet the events of the past year will most certainly define what unfolds in the New Year and beyond. To make sense of what 2020 will mean for the post-COVID era, we retooled and refreshed our models and forecasts to tackle the hard questions facing U.S. crude oil, natural gas, and NGL markets. As it turns out, beyond the immediate chaos of the pandemic, there is a new order taking shape, and that’s what we laid out in the RBN Fall Virtual School of Energy, sharing our results and the Excel spreadsheets behind the models to get you ready for what’s coming. Some of what we expected has come to fruition, and we still think that there is a pretty good chance that the rest will unfold in the months and years ahead. If you weren’t able to join us for the live broadcast, we invite you to sit by the fire, put your feet up and dig in over the holidays. The entire 14+ hours of streaming content, plus slide decks and spreadsheets, are available online. Today’s advertorial blog provides highlights from our key findings and the overall conference curriculum.

It’s been a wild and woolly December in the U.S. propane market. The Mont Belvieu propane price is up by almost 40%, blasting past 70 c/gal on Friday — a level not seen since February 2019, when WTI at Cushing was trading at $57/bbl, $8/bbl above where that price sits today. Is it simply cold weather goosing demand? Sure, that’s one factor. But it’s really all about exports. Just as 2020 cold weather finally arrived in U.S. propane country, exports hit the highest levels ever recorded. December Gulf Coast export volumes — 92% of the U.S. total — are up 21% over last month, and 39% above December 2019. So both international and domestic demand are pulling hard on supplies at the same time. No wonder propane prices are soaring. We started this series on winter 2020-21 supply/demand in late November by suggesting that there could be a few gotchas still out there that were not being reflected in the forward propane market. Well, we’ve now seen one of those gotchas. But there’s a lot of winter left to go — in fact, the official start of winter is this morning! Today, we review what’s happened so far in propane markets, and what could be coming next.

U.S. crude oil exports are off from the record highs they reached earlier this year, leaving the Gulf Coast even more flush with surplus export capacity than it had been going into 2020. And yet … Energy Transfer is developing an crude export terminal off the coast of Beaumont, TX, that would be capable of fully loading a 2-MMbbl VLCC every day or so. Is the company’s Blue Marlin project based simply on a hunch that U.S. oil production and exports will rebound over time and eventually leave PADD 3 short of dock and ship-loading capacity? Or is Energy Transfer’s proposed offshore terminal, with its extensive re-use of existing infrastructure, a cost-efficient way of giving oil-sands, Bakken and other producers more direct access to deep water and the supertankers that long-distance shippers prefer? Today, we discuss what may be behind the seemingly long-shot effort to develop new export capacity in a region that’s already got way too much.

As bitumen production in Alberta’s oil sands has grown over the past decade, so has demand for diluent, which is blended with molasses-like bitumen to help it flow through pipelines or be transported by rail. With bitumen output expected to continue rising through the first half of the 2020s, we have estimated that Alberta demand for field condensate, natural gasoline and other diluent will increase by more than 40% — to almost 1 MMb/d — by 2025. The catch is, diluent production in Western Canada isn’t growing fast enough to keep pace, and there are limits to how much diluent can be imported on the two existing pipelines from the U.S. What if there were a way to slash how much diluent is needed to put bitumen in rail tank cars — and make rail transport safer in the process? Today, we discuss Gibson Energy and US Development Group’s new diluent recovery unit in Hardisty, AB.

Back in 2005, marine terminals along the Gulf Coast were importing more than 6 MMb/d of crude oil, mostly to feed refineries within PADD 3 but also to pipe or barge north to PADD 2. By 2019, with U.S. shale production finishing up a decade-long rise, imports to the Gulf Coast had declined to less than 1.7 MMb/d. In COVID-impacted 2020, imports sagged, soared, then sagged again, recently settling in at about 1.2 MMb/d, their lowest level in — wait for it — 35 years! The 80% decline in Gulf Coast oil imports since the mid-2000s was made possible in part by big changes in the crude slates at refineries in Texas, Louisiana, and other PADD 3 states, mostly involving the swapping out of light sweet crude from overseas with favorably priced light sweet crude from the Permian and other U.S. shale plays. Today, we look at imports into PADD 3, the home of more than half of the U.S.’s total refining capacity.

Natural gas economic shut-ins! Shutting off a producing well on purpose, because the market won’t take the produced volume at a reasonable price. There was a time, back before gas commodity decontrol, when shut-ins were standard operating procedure, but that practice went the way of the dodo bird 40 years ago. Until earlier this year that is, when amid crushingly low prices, Appalachian producers said: enough is enough — and shut off the spigot themselves. In the months that followed, various producers have continued to see-saw their production in response to weather-related demand and regional market prices. The behavior signals that Appalachia’s shale gas producers are increasingly employing a light-switch approach in dealing with short-term weakness in demand and prices. Today, we take a closer look at the price-driven curtailments in the Northeast and potential implications for the market.

Wafting through the late autumn air in November, along with the sharp scent of burning leaves and the cinnamon-tinged aroma of pumpkin pie, was a moderate whiff of optimism for the energy industry’s long-beleaguered exploration and production sector. Equity prices in general were buoyed by news on the efficacy of the COVID-19 vaccines and the prospects of imminent approval that could finally bring the pandemic under control and improve industry fundamentals. E&P stocks, which also benefited from a rebound in third-quarter earnings, recorded the largest monthly gain in history: a 32% rise in the S&P E&P Index. However, their share prices were still down 69% from the 2019 highs and 45% from end-of-last-year levels as oil and gas producers still face a long road to return to “normal.” Today, we analyze the third-quarter earnings of the 40 major E&P companies we track and review the major impacts on the sector since the onset of the pandemic.

The energy world has been turned upside down in 2020 by COVID-19, resulting in the cancellation, scaling back, or deferral of numerous pipeline projects in both the U.S. and Canada. One such deferral involved a planned NGL pipeline that would run through the heart of Alberta’s Montney and Duvernay plays. Originally slated to begin construction earlier this year, a one-year deferral was announced back in May by the joint venture of Canadian midstream players Keyera and Energy Transfer Canada, the latter of which is itself a JV of Energy Transfer and KKR. Since then, a stabilization in energy markets and signs of recovery in Alberta NGL production has provided the co-developers with the confidence to commit to a construction start in 2021. Today, we review the project and what has changed to get it back on track.

Closing midstream deals has been a bit of a challenge in 2020, to say the least. In fact, this has been a year when many projects have been sidelined or cancelled outright, with most decisions on even the best prospects getting pushed to next year. But it hasn’t been all bad news. In a few cases, assets with advantages have made it across the finish line, even in the land of liquefied natural gas (LNG) export projects. Despite this summer’s collapse in U.S. LNG exports, driven by a compression of the spreads in global gas prices, Sempra Energy recently announced that it is going ahead with Phase 1 at its Costa Azul liquefaction project in Mexico’s Baja California. How did they pull this off in such a tumultuous year? Well, Costa Azul isn’t your everyday LNG export project. Today, we detail the most recent U.S. LNG export project to receive a final investment decision (FID) to proceed.

Cushing. This small town in central Oklahoma is the center of the U.S. crude oil universe, with prices at the Cushing hub serving as the reference price for all of the crude produced in the U.S. — and given the role that U.S. oil has assumed on the global stage, one of the most important determinants of global crude oil pricing. Considering the hub’s significance, it’s frequently surprising to industry veterans just how misunderstood Cushing can be. Like, for example, how SHOCKED the world was when Cushing prices dropped below zero back in April. Cushing traders had seen that coming for weeks — the only surprise to them was how far the price plunged that crazy Monday morning. It’s easy to see how something as enigmatic and complex as Cushing might be misunderstood — or underestimated — if you’re not familiar with its history, its inner workings, and its many crucial roles in both the physical and financial crude oil markets. It’s also tempting to think you can get by with only a passing knowledge of Cushing and how it operates. Au contraire! Cushing really matters, and market participants ignore it at their peril. The good news is that there’s finally a combo encyclopedia and user’s manual for “The Pipeline Crossroads of the World.” Today, we examine the hub’s significance to producers, refiners, midstreamers, marketers, and traders, and discuss highlights from RBN’s new Cushing Playbook.

On the 8th of October, the LNG carrier Golar Penguin loaded a cargo for RWE at the Freeport LNG terminal in Texas. Five days later, on October 13, the vessel was sitting just north of Panama. But then, the ship abruptly changed direction on the 14th and headed towards the Cape of Good Hope to deliver to the Far East. The reason for the diversion was that the vessel did not have a passage booked in the new locks of the Panama Canal and would have had to wait approximately nine days for its turn to transit, before heading across the Pacific Ocean to Asia. Since then, as queues of LNGCs for Panama Canal transits, both northbound (ballast) and southbound (laden) have developed, more ships have opted for the longer route. In today’s blog, we look at the delays that have developed surrounding the Panama Canal and the implications that its operations hold for global LNG trade.

To succeed over the long term in the music business, professional sports, or the midstream sector, you need to learn from your successes and failures, and — most important — continue adapting and evolving. For many North American midstreamers, a key to success has been a thoughtful combination of expansion and diversification, plus an affinity for financial discipline, especially when the broader energy industry is going through tough, uncertain times. A prime example of that strategy is Canadian midstreamer Pembina Pipeline Corp., which after C$14 billion in acquisitions over the last four years is instituting a more cautious approach to new investment that’s largely based on self-funding and a new, more rigorous return criteria for new projects. Today, we preview our new Spotlight report, which focuses on the risks and rewards of Pembina’s new strategy.