It’s well understood today that the U.S. natural gas market turned from potential domestic shortages to major LNG exports thanks to the Shale Revolution. What is not so well remembered is that the dramatic shift in the U.S. gas market wasn’t widely understood at the time and took several years to be accepted by the energy industry. In today’s RBN blog, we turn our attention to the beginnings of the Shale Revolution and how it allowed the U.S. to evolve into the world’s largest LNG exporter.

Analyst Insights are unique perspectives provided by RBN analysts about energy markets developments. The Insights may cover a wide range of information, such as industry trends, fundamentals, competitive landscape, or other market rumblings. These Insights are designed to be bite-size but punchy analysis so that readers can stay abreast of the most important market changes.

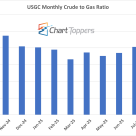

The monthly NYMEX crude-to-gas ratio for September 2025 stands at 21.4, where crude was $63.81/bbl and gas was $2.98/MMbtu, a slight decline from August’s 22.1.

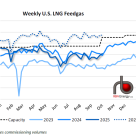

U.S. LNG feedgas demand averaged 15.4 Bcf/d last week (see blue-dotted line in figure below), up 0.1 Bcf/d from the previous week despite lower intake at Cove Point.

The Permian Basin has been producing oil in West Texas since the 1920’s. The principal route to market for Permian crude has been via Cushing, OK to Midwest refineries. After declining in the 1980’s Permian production is increasing again – reaching an estimated 1.3 MMB/d (September 2012 Bentek). The existing pipeline infrastructure means the majority of that crude still finds its way to Cushing and the Midwest. There Permian producers face the same congestion and price discounts that Canadian and Bakken producers have suffered. Today we review current Permian Basin routes to market.

Refinery yields are an important measure of refinery performance indicating the outputs that running a particular crude through a refinery configuration will produce. When these outputs are matched against refined product prices, the relative financial performance of different refinery configurations in different locations can be compared. Refinery yields are also important inputs to the optimization calculations that refiners use to determine the best mix of crudes to process. Today we review how refinery yields are determined and the part they play in refinery optimization.

Unlike pipelines that take a long time to build and only deliver to a handful of destinations, rail freight cars offer the flexibility to deliver anywhere across North America. The rail freight industry can load, store and transport different NGLs (including those NGL products that must be transported under high pressure) as well as crude and petroleum products. Rail infrastructure is mostly already in place so new routes can easily be brought on line. That’s why rail freight has been used successfully by the energy industry for over 100 years as - a “pipeline on wheels”. Today we look at the rail tank car business for moving NGL and petroleum products.

Permian basin oil production rose above 1 MMb/d last year (2011) for the first time since 1998, after sliding from a 1973 peak of 2.1 MMb/d. A lot of new Permian production uses conventional drilling and enhanced oil recovery techniques, but horizontal drilling is making its mark as well. The West Texas crudes this basin produces are sold the same way as any other except they have their own futures contract trading 60 MMb/d. Today we turn the RBN spotlight onto the Permian Basin.

Our good friends at Turner, Mason & Company (TM&C) released the latest update to their 2012 North American Crude Oil Outlook (NACOO) today (www.turnermason.com), looking at the crude oil market from a downstream perspective – where all the light shale and heavy Canadian oil is going to go and how it is going to impact refiners when it gets there.

Over the past five years exploitation of abundant gas and oil bearing shale basin formations by combining and augmenting two long-standing technologies has revolutionized North American energy markets. If you are at all involved in the energy industry you know that these technologies – horizontal drilling and hydraulic fracturing - are bigger than Bieber right now. Maybe bigger than Taylor Swift. Today we explain how they work and why they are so important.

Nowadays everyone is pretty sure that there is plenty of natural gas supply to go around. Storage is bursting at the seams; production is close to record levels. Midstream infrastructure companies are busy developing new pipelines and additions to deliver shale gas to existing markets. Market analysts agree that new natural gas demand over the next decade will largely come from increased gas fired power generation. Is the current natural gas infrastructure configured to deliver gas to this new generation capacity? Today we report on emerging power industry planning concerns.

The West Coast natural gas liquids (NGL) market is an island unto itself. Unlike the world east of the Rockies where pipelines link together producing and consuming regions, the West Coast NGL market is marooned except for rail tank cars and a few waterborne cargos. It is a fiercely independent market with its own unique players playing their own ballgame. But like the rest of the NGL world, big changes are rippling through that market. Today we begin a series looking at those changes and how West Coast NGLs are likely to evolve over the next few years.

US Complex refining capacity leads the world and US Gulf Coast refineries are enjoying an export led boom. As lower cost crude starts to become available to these refineries they should be in a strong position to compete even more efficiently in global markets. What makes these complex refineries competitive? Today we conclude our two part refining tutorial by explaining refinery upgrading processes.

If you haven’t already read the first part of this tutorial then you can review it here. In Part 1 we provided an overview of the refining process described the fractions that make up crude oil and ran through the refined product outputs of a complex refinery. We looked at the first refinery process – atmospheric distillation that breaks crude down into its component fractions. Today we turn to the processes refiners use to upgrade the heavier residual fuel oil outputs from atmospheric distillation.

NGL prices have been weak this year, but the same has been true for the price of natural gas. So how does this market scenario play out for gas processors who make their money extracting NGLs from gas? Last week we looked at what could be gleaned from the Frac Spread, and concluded that it missed a couple of key variables like the liquids content and the BTU value of the inlet gas. So today we’ll see what it takes to incorporate those factors into our analysis and in the process dive deep into the math of gas processing to learn about things like cubic feet, GPM and moles.

In June 2012 Bakken oil production reached 660 Mb/d with 0.7 Bcf/d of associated natural gas. A third of that associated gas (32 percent or 0.22 Bcf/d) was flared at the wellhead. There are sound environmental and economic reasons why flaring occurs. In other States like Texas the percentage of flaring is tiny (0.5 percent). The answer to flaring is better infrastructure but huge investments in North Dakota could still not be enough to eliminate flaring. Today we shed new light on the issue.

The US has more refining capacity than any other country (17MMb/d) and nowhere are refineries as sophisticated. In the past two years US refineries in the Midwest region have been running close to full capacity and refineries in the Gulf Coast region have led a refined product export boom. At the same time, refineries on the East Coast have been shuttered or saved only by a combination of last-minute deal-making and government subsidies. What makes one refinery better than another? Today we walk through the first distillation process in a complex refinery.

In the wake of competition from historically low natural gas prices and anti carbon environmental legislation the domestic US coal industry is reeling but it remains competitive in an expanding world market. In today’s blog we dig into projects for the export of Powder River Basin coal from terminals on the West Coast destined for markets in Asia.

2012 has not been a good year for natural gas liquids prices. Spring was a particularly brutal season, with prices falling to levels not seen since the bad ole days of 2009. This summer prices have recovered from late-June lows, but the numbers are still in the dog house relative to the past couple of years. Although this is hardly something that sprung up overnight, lately it seems like there has been a rash of hand wringing by analysts, rating agencies and not a few companies warning about the consequences for midstream businesses and NGL producers. Our friends at Tudor Pickering called it a ‘Blood Bath’. Is it really that bad? Our blog series in March called 2012 the ‘Golden Age’ of gas processors. Have we gone from a Golden Age to a Blood Bath in six months? It seems like it’s time for another deep dive into gas processing and NGL production.

In the immediate aftermath of disasters like hurricane Isaac, our thoughts focus on the victims and the tremendous damage to homes and infrastructure alike. As a category 1 hurricane Isaac has not so far shown the destructive force that its infamous predecessor, Katrina did in 2005. In particular energy infrastructure has been shut in by Isaac as a precaution but appears not to have suffered lasting damage. The Gulf of Mexico remains an important center for US crude oil and natural gas production. Today we compare the production shut ins caused by Katrina and Isaac and their impact on the national picture.