More than 70 new data centers are under development in Virginia, which is already the world’s leading hub for the massive, high-tech facilities. But given the rapid pace of the buildout and the challenges that come with it, it’s probably no surprise that not everyone in the Old Dominion State is as enthusiastic about data centers as they once were. In today’s RBN blog, we’ll look at some of the biggest data centers in the works and discuss their path forward.

Analyst Insights are unique perspectives provided by RBN analysts about energy markets developments. The Insights may cover a wide range of information, such as industry trends, fundamentals, competitive landscape, or other market rumblings. These Insights are designed to be bite-size but punchy analysis so that readers can stay abreast of the most important market changes.

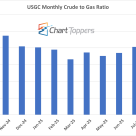

The monthly NYMEX crude-to-gas ratio for September 2025 stands at 21.4, where crude was $63.81/bbl and gas was $2.98/MMbtu, a slight decline from August’s 22.1.

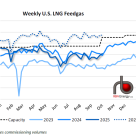

U.S. LNG feedgas demand averaged 15.4 Bcf/d last week (see blue-dotted line in figure below), up 0.1 Bcf/d from the previous week despite lower intake at Cove Point.

The Dakota Access Pipeline isn’t the only interstate liquids pipe facing an uncertain future. The fate of Enbridge’s Line 5, which batches either light crude oil or a propane/butanes mix from Superior, WI, through Michigan and into Ontario, also hangs in the balance as the company renews its battle with Michigan’s top elected officials to keep the 67-year-old pipeline open and its effort win regulatory approval to replace the pipe’s most important water crossing. Line 5 supporters say that closing the 540-Mb/d pipeline would slash supplies to residential and commercial propane consumers in the Great Lakes State, steam crackers in Ontario, and refineries and gasoline blenders in three states and two Canadian provinces. Critics of Line 5 counter that there are plenty of supply alternatives. Today we discuss the pipeline, what it transports, and who it serves, as well as challenges it faces.

When you talk about energy molecules, propane takes the prize for the most versatile. In addition to its well-known uses for BBQ grills, indoor cooking, and home heating, propane is used for drying crops, as a feedstock for petrochemicals, as an engine fuel for forklifts and fleet vehicles, and in recent years, as an export product in its own right. Propane moves to market on pipelines, railcars, ships, barges, trucks — just about any form of transportation you can imagine. But exactly how any particular molecule of propane makes the journey from the instant it comes out of a well to all those market destinations can be a mystery to all but a small cadre of propane market insiders. In another in our series of updates to RBN’s greatest hit blogs, we are delving into this mystery, one step at a time, today focusing on transportation from the producing basin to storage and fractionation at the Mont Belvieu hub, and the transformation of the generic commodity to a marketable fuel.

Bakken associated gas production volume, after falling to its lowest levels in three years in early May and remaining depressed through June, has surged by 500 MMcf/d, or about 45%, in the past month and a half to 1.7 Bcf/d. However, the gains have occurred in the absence of a meaningful change in rig counts or well completion activity, which remains sluggish. Similar to the Permian, the Bakken production recovery has been almost entirely driven by existing wells returning to service after being shut in earlier this year in response to the oil price collapse. With little in the way of new drilling and completion activity, how long will it be before natural declines of existing wells begin to take a toll on Bakken output? Today, we examine prospects for continued strength in Bakken gas production volumes.

The oil price meltdown earlier this year and demand destruction wrought by COVID-19 forced Canadian crude oil producers to throttle back output. At the height of the cutbacks in May, almost 1 MMb/d of oil supply had been curtailed due to uneconomic prices and/or lack of downstream demand. With oil prices and demand having staged a partial recovery in the past few months, production is rising off the lows and producers are talking about even higher supplies in the months ahead, with the prospect of returning to pre-pandemic levels. Today, we begin a short series that reviews the recent production pullback and discusses how producers are positioning themselves for a resurgence of their oil supplies.

The U.S. power sector’s shift to natural gas over the past few years has been a boon to gas producers across the Lower 48, especially in the Northeast. Scores of new gas-fired power plants have been built there during the Shale Era, and a number of coal-fired, oil-fired, and nuclear plants have been taken offline. New England is a case in point; gas-fired power now accounts for about half of the installed generating capacity in the six-state region (Connecticut, Rhode Island, Massachusetts, Vermont, New Hampshire, and Maine) — three times what it was 20 years ago. But New Englanders have a love-hate relationship with natural gas, and with renewables and energy storage on the rise, gas’s role in the land of the Red Sox, hard-to-understand accents, and lobsta’ rolls may well have peaked. Today, we discuss recent developments on the natural gas and power generation fronts in the northeastern corner of the U.S.

The global LNG market upheaval has wreaked havoc on U.S. LNG export demand this summer, which, in turn, has complicated operations at domestic export facilities. Gone are the days when U.S. LNG exports would move predictably, increasing with each new liquefaction train coming online and then mostly staying at or near capacity. Rather, as international LNG prices collapsed, U.S. LNG operators for the first time have had to contend with a relentless stream of cancelled cargoes and low facility utilization rates. More recently, cargo cancellations are showing signs of easing somewhat, as international price spreads are improving for fall and winter. But these recent market disruptions provide a window into the ways in which operational constraints and flexibilities will factor into LNG producers’ and offtakers’ decisions — and affect feedgas flows and capacity utilization — in a weak global market. Today, we consider some of the nuances of liquefaction operations.

When firing up the backyard propane grill and watching that first propane molecule flash to life, most people don’t think much about what it took to get that fuel to the cylinder they picked up at the store. But that long and winding road from the production well to the tank beneath your grill is actually a fascinating tale of supply-chain logistics involving producers, midstreamers, and propane retailers. In today’s blog, we will take that interesting and sometimes mysterious trip with a molecule of propane. We will travel over 1,000 miles, moving in and out of various facilities, purifying our product and incurring various costs each step of the way. So strap on your seat belt for a selection from our greatest blog hits, in which we track a typical propane molecule’s journey from beginning to end.

For U.S. refineries, the severe demand destruction that occurred this spring led to the worst financial performance in recent history. Not only did refiners produce less diesel, motor gasoline, and jet fuel in the second quarter than any quarter in recent memory, their refining margins were sharply lower than the historical range — a one-two punch that hit their bottom lines hard. The situation has improved somewhat this summer, but it’s still tough out there. So tough, in fact, that it’s reasonable to ask, does the coronavirus and its impacts to the energy sector signal the end of an era for refiners across the U.S.? Today, we review the decline in fuel demand and profitability in the second quarter and discuss the uncertainties refiners face in the second half of 2020 and beyond.

Canada’s propane market has quickly morphed from one characterized by abundant supply to one facing a tightening supply/demand balance, with direct exports to Asia playing an increasingly important role. This tension became evident in May 2019, when the start-up of the Ridley Island Propane Export Terminal (RIPET) in British Columbia, Canada’s first direct export connection for propane to Asian markets, effectively eliminated the usual seasonal surplus for propane in Western Canada. With rail exports of propane to the U.S. often reliant on that excess for restocking in the summer months and as a reliable fallback supply in the cold winter months, the prospect of fewer or no periods of excess supply may be signalling trouble for some U.S. regions that have come to rely on those volumes. What’s more, within a few months, another propane export terminal in BC will be starting up, further reducing what’s left for the U.S. market. In today’s blog, we conclude our series examining the Western Canadian propane market by considering the impacts of Canada-to-Asia propane sales on U.S. propane consumers and propane prices.

In their second-quarter earnings presentation last week, Energy Transfer said that they and their joint venture (JV) partners, Satellite Petrochemical, expect the first commissioning cargoes from their new 180-Mb/d ethane export facility in Nederland, TX — formally known as Orbit Gulf Coast NGL Exports LLC — to begin in November, only three months from now. This new outlet for U.S.-sourced ethane comes at a time when production of oil, gas, and NGLs faces near-term declines due to reduced drilling activity resulting from low crude prices. With those declines, will there be enough ethane supply to meet the capacity of the new Orbit export dock and other upcoming ethane-related projects? The short answer is, yes … for the right price. Today, we examine the latest supply and demand dynamics shaping the U.S. ethane market.

It’s only August, but the folks involved in Permian markets must feel like they’ve already packed in a full year’s worth of action. The events are well known by now, but they’re still remarkable. A crash in refining utilization, followed by massive field shut-ins, all precipitated by a novel virus and exacerbated by some unusual moves by global oil producers. The year’s not over, and the coronavirus hasn’t gone away like a miracle, but a calm has emerged in oil prices that has helped producers get their sea legs. While $40/bbl West Texas Intermediate (WTI) is a far cry from where we started 2020, it’s been just enough to get most of the shut-in crude production back online in West Texas. Today, we provide an update on the status of curtailments in the Permian Basin.

Over the past five years, the production of natural gas liquids from gas processing plants has soared by almost 2 million barrels per day (2 MMb/d), or about 60%. That has been great news for natural gas producers, processors, and end-use markets. But there is a catch: the rate of production does not match up with demand. While production is a steady, “ratable” volume, demand is anything but ratable. Demand swings with the gasoline blending season, cold weather (or lack thereof) in the propane market, export demand, petchem feedstock economics, the impact of COVID-19 on transportation fuels, and a myriad of other factors. The flywheel that balances supply and demand on any given day is storage. Not just any storage, though. For NGLs, storage of large volumes means salt caverns. Huge caverns thousands of feet below the surface. Today, we update one of RBN’s Greatest Hits blogs and take a deep dive into the history of NGL storage — all the way back to Smoky Billue.

The collapse in crude oil prices this year hit U.S. producers hard, and forced them to make big cuts in their capital budgets and drilling plans. But it also helped to prove their resilience. Throughout the Shale Era, and especially since the 2014-15 oil price crash, producers have been increasing their productivity and slashing their production costs, enabling most of them to survive even when prices slipped below $30 and $20/bbl for a while. Not all producers are alike, however — neither is all production. Even with oil prices rebounding to about $40/bbl in recent weeks, production based on enhanced oil recovery (EOR) through carbon-dioxide (CO2) “flooding” has become economically challenged, at least for some producers. Can EOR, with its high production costs, survive in a low-price environment? Today, we take a fresh look at EOR in an era of $40/bbl crude.

The global effort to stop the spread of COVID-19 brought the commercial aviation sector to its knees, and slashed demand for jet fuel to its lowest level in 50 years. That, combined with lower demand for motor gasoline and — to a lesser extent — diesel, forced refineries in the U.S. and elsewhere to substantially reduce their crude oil input and to make major changes in their operations, all with the aim of bringing refined product supply and demand into closer balance. After a horrific spring, U.S. jet fuel production and demand have been rebounding somewhat in recent weeks, but getting back to pre-coronavirus levels may take a long time. Today, we review the flight from hell that the jet fuel market has suffered through so far this year, and how it is affecting refineries.

The Ridley Island Propane Export Terminal — Canada’s first propane export facility — has been a game changer since it started up in May 2019. Located along the coast of British Columbia, RIPET has been shipping record amounts of propane to Asian markets in recent months, just as Western Canadian propane production has been sagging due to the twin pressures of crude oil price weakness and COVID-19-related disruptions. With production down, RIPET gradually ramping up its export capacity, a second export terminal poised to come online nearby, and Canadian demand for propane holding steady, something has to give, right? Today, we examine the changing supply/demand outlook for Western Canadian propane, and what it might mean for railed exports to the U.S.