Sure, natural gas markets have experienced plenty of changes over the past few years. Rising associated gas production in the Permian. New pipeline and storage capacity. New LNG demand. Pricing ups and downs. But we’d argue that all this was merely a prelude. That the main event — a veritable transformation of gas markets, especially along the Gulf Coast — is about to begin. A doubling of LNG demand (to 32 Bcf/d!). Another 10 Bcf/d of new pipelines out of West Texas, plus at least 15 Bcf/d more along the coast. Production revivals in the Haynesville and the Eagle Ford. And don’t forget soaring demand for gas-fired power generation. In today’s RBN blog, we discuss the massive, market-transforming changes just ahead — and our upcoming GasCon 2026 conference, which is hyper-focused on this market-shifting inflection point.

With all the announcements in 2022-25 — upstream and midstream consolidation, new pipelines and storage projects, new LNG export terminals, etc. — you’d be tempted to think this has been a period of extraordinary change. And you’d be right. But the fact is, the past few years in the U.S. natural gas market have really been just a teaser, a preview, an appetizer. Now, finally, all the planning and shifting is coalescing. A major, five-year ramp-up in LNG capacity is beginning in earnest. Soaring gas demand along the Gulf Coast will support stronger gas prices and, with that, more drilling and production, not just in the Permian but the Haynesville, the Eagle Ford and, very likely, other basins further afield. And to connect the supply and demand, new multi-Bcf/d pipelines will be coming online and storage projects will be developed.

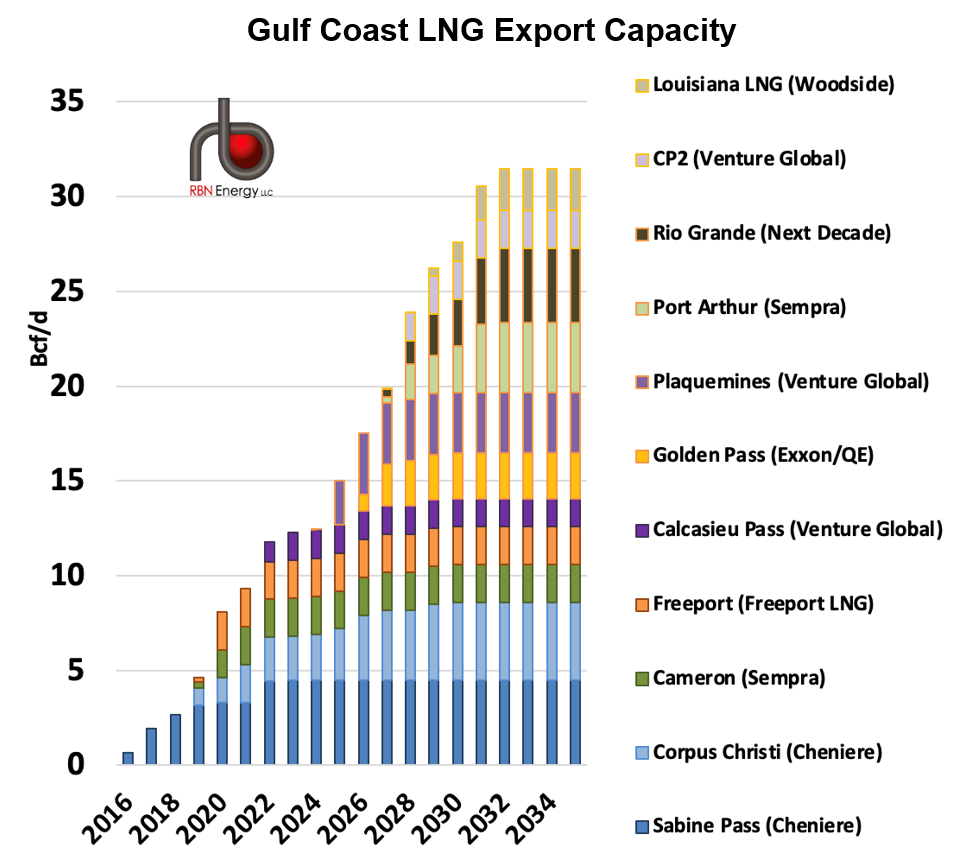

Let’s begin with the demand angle, because, despite being spurred by natural gas supply pushing out of basins like the Permian, it’s going to be the primary driver behind the upcoming market transformation. RBN’s Arrow Model, which closely monitors the planned addition of new LNG export capacity, projects that feedgas demand from LNG terminals in Texas will soar from “only” 4.5 Bcf/d in 2025 to 8.8 Bcf/d in 2027 and about 16 Bcf/d nine years from now. LNG feedgas demand in Louisiana is projected to rise more gradually, from an already hefty 10.6 Bcf/d in 2025 to 11.7 Bcf/d in 2027 and ~16 Bcf/d in 2035. (Figure 1 below shows the planned additions.) Liquefaction-train commissioning is underway at Plaquemines LNG (already consuming 3.9 Bcf/d on average in December), Golden Pass LNG and Corpus Christi LNG Stage III, with more to follow at these export terminals and others the next couple of years. Still more are on the way: Over the past 12 months, no fewer than six Gulf Coast LNG projects with a combined capacity of 61 MMtpa (8.1 Bcf/d) reached a final investment decision (FID): trains 4 and 5 at Rio Grande LNG, a two-train expansion at Port Arthur LNG, a small expansion at Corpus Christi Stage III, and two entirely new terminals (Venture Global’s CP2 and Woodside’s Louisiana LNG).

Figure 1. Gulf Coast LNG export capacity. Source: RBN

No doubt, there’s at least a little angst about the possibility of an overbuild. (Not unlike the worries some express about AI and data centers, which we talked about in our recent 2026 Prognostications blog.) Just a few days ago, Energy Transfer (ET) announced that it had suspended development of its 16.5-MMtpa (2.2-Bcf/d) Lake Charles LNG project, despite having secured long-term commitments for nearly 80% of its capacity. (ET said the company’s gas pipeline projects, including two out of the Permian, would provide “superior risk/return profiles.”) But we see LNG export volumes holding up, even if margins for some do get thin — we’ll explain why at GasCon 2026 in February — and we expect still more LNG projects will reach FID this year, including capacity being eyed by heavy hitters Cheniere Energy and Venture Global.

Iowa Gas Stations Must Now Offer E15 Gasoline

Now that the calendar has turned to 2026, most gas stations in Iowa are required to advertise and sell E15 gasoline. The requirement was included the state’s E15 Access Standard, which was adopted by the state legislature in 2022.

While expected growth in LNG feedgas demand may dominate, there’s also a lot happening on the power-generation front. ERCOT, the electric-grid operator for most of Texas, has said it expects power demand in its region to roughly double by the early 2030s, with most of the incremental need for electricity coming from data centers and much of the rest driven by population/economic growth and the electrification of Permian production. And while we remain skeptical of the scale of data center development, several gas-fired power projects are planned in Louisiana and the broader Southeast. Together, these may well add up to several Bcf/d of gas demand.

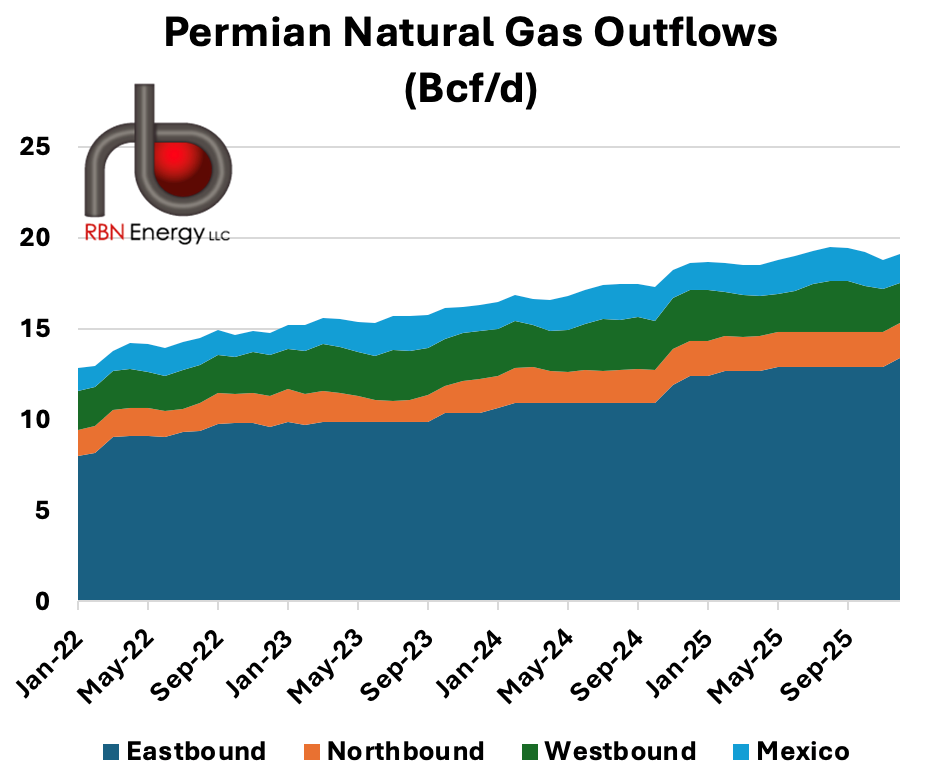

The gas-supply part of the equation is, well, complicated. On one hand, there’s ongoing supply-push production in the Permian, where crude-oil-focused drilling generates massive — and, thanks to rising gas-to-oil ratios (GORs), steadily growing — volumes of associated gas that need to be gathered, processed and (for nearly 90% of the natural gas and all the NGLs) transported to end users outside the basin. According to RBN’s NATGAS Permian report, of the 19 Bcf/d of gas that exits West Texas and southeastern New Mexico (stacked layers in Figure 2 below), 13 Bcf/d is piped east (dark-blue layer), predominately to the Gulf Coast — the other 6 Bcf/d is split about equally among northbound (orange layer), westbound (green layer) and Mexico-bound (light-blue layer) pipelines out of the Permian.

Figure 2. Permian Natural Gas Outflows.

Sources: RBN Arrow Model, RBN NATGAS Permian, Wood Mackenzie, EIA

There’s also demand-pull production in other areas supplying gas to the Gulf Coast. These include the Eagle Ford in South Texas and the Haynesville in northwestern Louisiana and northeastern Texas, plus more distant gas-producing plays like the Marcellus/Utica in Appalachia, the Anadarko in the Midcon, and the Niobrara in the Rockies. (Some also are placing bets on the Western Haynesville in East Texas’s Freestone, Leon, Limestone and Robertson counties.) The old-school Haynesville is the coast’s biggest swing-production region. It has vast amounts of gas trapped in its rock and it’s only a hop, skip and a jump from a long list of LNG export terminals. But there’s an important catch, namely that a substantial portion of its gas reserves are economic to develop only if gas prices top $3, $4 or even $5/MMBtu. (Another topic we’ll discuss in depth at GasCon 2026.)

The increasing volumes of natural gas being pushed or pulled to the Gulf Coast will require an increasingly beefed-up and flexible network of pipelines and gas-storage facilities. Midstream companies have been responding to this need in spades. Over the past couple of years, hardly a month has gone by without the announcement of yet another greenfield project or expansion of an existing facility. Consider gas pipelines out of the Permian. Gulf Coast Express (GCX), Permian Highway Pipeline (PHP) and Whistler Pipeline added a combined 6-plus-Bcf/d of takeaway capacity in 2019-21, and Matterhorn Express brought another 2.5 Bcf/d in 2024.

That was just the beginning, though. As we noted in the introduction to today’s blog, another 10 Bcf/d of pipeline capacity out of West Texas is in the works, including 8.4 Bcf/d to the coast: 2.5 Bcf/d from the Blackcomb Pipeline to the Agua Dulce hub in late 2026; 1.5 Bcf/d from the Hugh Brinson Pipeline to the Dallas area, also in late 2026 (followed by a 700-MMcf/d expansion a year later); and an astounding 3.7 Bcf/d from Eiger Express in 2028-29. To the west, Energy Transfer in August took FID on its 1.5-Bcf/d Desert Southwest Pipeline from the Waha Hub to the Phoenix area. All that new pipe could turn the Permian’s long-lived dearth of exit capacity and abysmal local gas prices into a (temporary) glut and narrow price basis.

The anticipation of rising LNG export and power-generation demand also has been underpinning the development of new gas pipelines from the Haynesville to the coast, new pipelines along the coast, and new gas storage throughout the Gulf Coast region. Out of the Haynesville, there’s the 1.8-Bcf/d Louisiana Energy Gateway (LEG) and the 2.2-Bcf/d Momentum NG3 pipelines, both of which came online in 2025, as well as the planned 2.5-Bcf/d Pelican Pipeline, slated to start up in the latter half of 2027, and Boardwalk’s recently announced 1.5-Bcf/d Texas Gateway project, which would come online in late 2029. Along the coast, there’s another set of pipeline projects totaling 15 Bcf/d — from south to north, they include Rio Bravo (4.5 Bcf/d), Traverse (2.5 Bcf/d), Blackfin (3.5 Bcf/d), Trident (2.2 Bcf/d), and Mustang (2.5 Bcf/d).

There’s one more category of Gulf Coast gas pipelines to keep in mind: projects to help deliver gas to new power plants and other customers in the Southeast. Examples? One is Boardwalk’s 1.16-Bcf/d Kosci Junction Pipeline, which will run 110 miles south/southeast from a Texas Gas Transmission (TGT) leg near Kosciusko, MS — Kosci for short — to an interconnect with the company’s Gulf South system. Others include Kinder Morgan’s 2.1-Bcf/d Mississippi Crossing and 1.3-Bcf/d South System Expansion 4 projects, which will help deliver gas off Kinder’s Tennessee Gas Pipeline (TGP) system, plus a slew of expansions on or near Williams’s Transco system.

And then there’s gas storage. The fluctuating gas needs of Gulf Coast LNG export terminals and power generators have been spurring the buildout of gas storage facilities in the region. More than 150 Bcf of additional storage capacity is planned. (See our Drill Down Report on the topic for more.)

Build your energy market expertise at the 20th School of Energy: Foundations.

Learn from RBN experts, participate in hands-on Excel modeling, connect with industry peers, and gain a stronger understanding of today's interconnected energy markets.

September 9-10 | Houston, TX

It would be challenging enough to wrap your head around the complicated story tying together soaring gas demand, rising production, gas-price shifts, infrastructure additions, and gas flows. But there are still other variables at play — including political changes within the U.S. and geopolitical uncertainties around the globe — that will each have their own effects on how Gulf Coast gas markets evolve over the next five to 10 years.

To help explain how all these pieces fit together and impact each other, RBN is planning GasCon 2026. This one-day conference at Hilton Americas in Houston, slated for Wednesday, February 25, will bring together RBN’s top analysts and leading executives from across the industry to discuss the latest developments in Gulf Coast gas markets. With these markets entering the most exciting — and challenging — era ever, it’s critically important for gas industry participants to keep up with the latest on the region’s gas demand, gas supply, and the pipelines, storage and LNG export terminals that connect it all. Looking forward to seeing you there! (For more on GasCon 2026, click here.)

About the song

“Gaston” has lyrics written by Howard Ashman and music by Alan Menken. It appears as the fourth song on side one of Beauty and the Beast: Original Motion Picture Soundtrack. It is sung by Jesse Conti as LeFou, Richard White as Gaston, and Paige O'Hara, Richard White, Jerry Orbach, Angela Lansbury and Jesse Conti as the chorus. The song includes the following lyrics ...

“My, what a guy, that Gaston

Give five ‘hurrahs!’

Give twelve ‘hip-hips!’

Gaston is the best

And the rest is all drips”

... which describe the specialness and superiority of the Gaston character. Beauty and the Beast is an animated romantic comedy based on the fairy tale written by French novelist Gabrielle-Suzanne Barbot de Villeneuve. It was directed by Gary Trousdale and Kirk Wise, from a screenplay by Linda Wolverton. Released in November 1991, it grossed $331 million, making it the third-highest-grossing film of 1991 and the first animated film to gross over $100 million in the U.S.

Beauty and the Beast: Original Motion Picture Soundtrack was recorded in 1989-91 at BMG Recording in New York City, Evergreen Studios in Los Angeles, and Sony Studios in Culver City, CA. Produced by Howard Ashman, Alan Menken and Walter Afanasieff, the album was released in October 1991. It went to #9 on the Billboard Soundtrack Albums chart and #19 on the Billboard 200 Album chart. It has been certified 3X Platinum by the Recording Industry Association of America. One single was released from the LP.

A live-action movie of Beauty and the Beast, released to theaters in March 2017, starred Emma Watson, Dan Stevens, Luke Evans and Kevin Kline. Directed by Bill Condon, it grossed $1.27 billion, becoming the second-highest-grossing film of 2017.

"About the Song" -- written by Mickey McMahan , RBN Director of Musicology