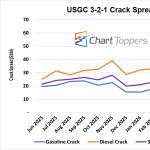

The USGC 3-2-1 crack spread (purple line) is averaging about $45/bbl so far in June, down from about $51/bbl in May but still more than double the roughly $21/bbl average seen a year earlier. Diesel cracks led the rally, jumping from about $33/bbl in February to $66/bbl in March before easing to $56/bbl in June. Gasoline cracks (blue line) were slower out of the gate, climbing from winter levels near $15-$18/bbl to $46/bbl in May before slipping back to $40/bbl in June. While both gasoline and diesel cracks (orange line) have softened from their spring highs, diesel remains up about 122% year over year and gasoline is up about 104%, leaving refining margins well above year-ago levels.

Featured Articles

- Analyst Insight

USGC Crack Spreads Ease but Remain Elevated

USGC crack spreads are easing in April, but margins remain well above historical norms as diesel and gasoline cracks stay elevated year over year.

- Blog

Double-Edged Sword – Refinery ‘Capacity Creep,’ Falling Inventories May Limit U.S. Crude Export Surge

U.S. crude oil production averaged a record 13.6 MMb/d in 2025, up nearly 1.6 MMb/d from 2023, but crude export volumes remained remarkably stable — at or very near 4.1 MMb/d — until a recent Iran-related surge. A key reason: “capacity creep” expansion projects at several Gulf Coast refineries.

- Blog

Two Out of Three Ain’t Bad – U.S. and European Refineries Thriving So Far, But Asian Ones Suffer

It’s been eight weeks since the steady flow of crude oil and refined product tankers out of the Persian Gulf ended, and the impacts on refineries and product suppliers in key parts of the world are becoming clearer. In today’s RBN blog, we discuss the state of refining in the U.S., Europe and the Asia-Pacific region.