The US Gulf Coast is perceived by midstream operators to offer a growing opportunity for the export of fuel oil left over from refinery processing. The US does not produce as much residual fuel oil as European refiners and the largest market is in Asia. But the US Gulf is ideally positioned to import fuel oil from Europe or Latin America to blend with domestic production and export to Asia. New terminal infrastructure is coming online to meet growing demand for storage and blending facilities. Today we look at the Gulf Coast’s largest fuel oil terminal.

This is the second installment in our series covering fuel oil infrastructure on the Gulf Coast. In the first episode we provided definitions for some of the many types and grades of fuel oil (see Yo Ho Ho and a Cargo of Bunkers). We discussed the main markets for fuel oil as a feedstock for refineries and as bunker fuel for ships. There is also demand for fuel oil or its derivatives in manufacturing industry and power generation.

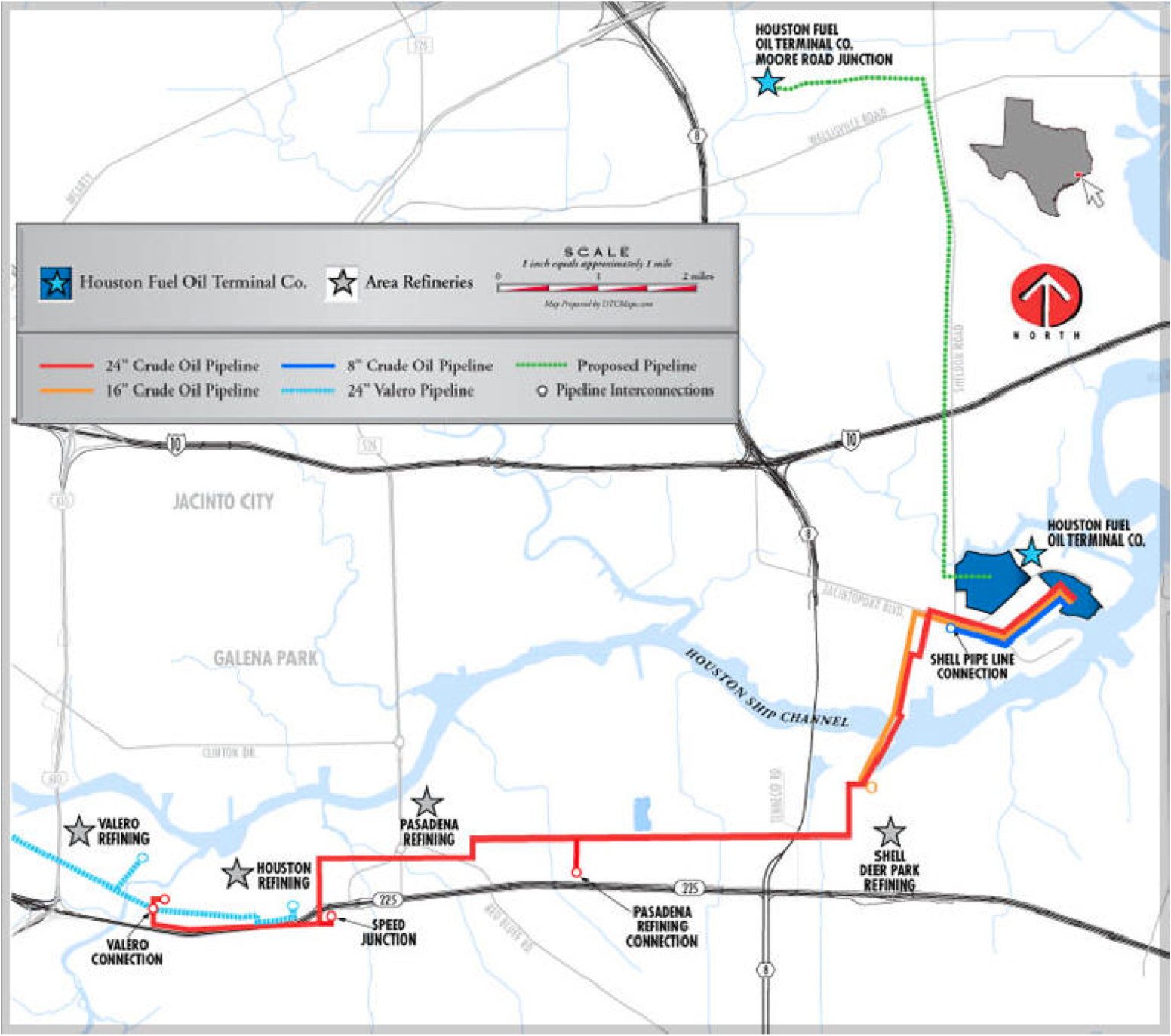

Alinda Capital Partners LLC, an infrastructure investment firm, owns Houston Fuel Oil Terminal Company (HFOTCO), the largest provider of residual fuel oil storage in the Gulf of Mexico. HFOTCO is located on 310 acres along the Houston Ship Channel (HSC) with marine dock access to the Gulf of Mexico. Founded in 1978 and originally dedicated to storing, blending, and moving residual oil, HFOTCO has also been handling crude oil since the early 1990’s.

HFOTCO has 16.1 MMBbl of storage capacity including a recently completed 1.3 MMBbl expansion. The majority of the storage is for residual oil (12.9 MMbbl) with the remaining 3.2 MMBbl used for crude. All the residual oil tankage is steam heated and insulated to keep product liquefied. The terminal can handle the delivery and unloading of heated fuel oil from tankers and barges as well as by rail and truck. They have rail facilities to unload up to 50 rail tank cars equipped with coils and insulation to handle fuel oil that has to be heated to flow (see Heat It for more on moving heavy oil by rail). There are plans to expand the rail facility by 20 rail tank cars but for the moment they cannot unload a “unit” train with 100 or more cars. The rail unload facilities are designed to handle fuel oil but not crude. That is because the heated tanks the product is offloaded into do not have the floating roofs necessary to store crude oil. Such floating roofs are required for crude because it typically has more volatile compounds than fuel oil. Some upgrading of the rail unload facilities would therefore be required for HFOTCO to handle heavy crude bitumen oil from Canada that we have discussed in recent RBN blogs (see Go Your Own Way).

For marine access HFOTCO has four ship docks that can load and unload fuel oil cargoes at 40 Mb/hour. Three of the docks can also handle crude oil. In addition HFOTCO has seven barge docks that can service 19 barges simultaneously. Aside from storage and blending in the HFOTCO tanks, crude and fuel oil can be received or delivered to local refineries on the HSC by pipeline. The map below shows pipeline connectivity to four area refineries. HFOTCO is also able to receive crude from the Magellan Speed Junction pipeline hub (see The Gates of Magellan). A pipeline project is currently underway to link HFOTCO to the Magellan Moore Road Junction (green dotted line on the map) that will be the receipt point for the 130 Mb/d Keystone XL Houston Lateral expected online in 2015.

Source: HFOTCO Website

Typical customers use HFOTCO for one of four purposes as follows:

Refinery Crude Feedstocks: HFOTCO has vessel capacity to import crude oil cargoes for local refineries. In addition, the storage facilities can be used to break down larger cargoes of fuel oil into smaller quantities of feedstock. This fuel oil feedstock is used to provide supplementary supplies for upgrading units at local refineries that do not produce enough fuel oil from processing their own crude. Residual Fuel Oil Blending: trading companies blend refinery fuel oil leftover from local refineries for export to overseas markets. Small volumes are sold (mostly as emergency backup fuel) to US electric power utilities. Fuel oil is also imported from Europe or Latin America or delivered to HFOTCO by barge or rail from US refineries in the Midwest. Roughly 80 percent of residual fuel is exported, much of it to Asia.

Comments

Remember 2007's Golden age of Refining ?

Economics now vividly point out opportunities in the FO and Crude Markets that exist today for blenders.

Refining Boom, E&P boom, Shale Boom, Energy Vets. will say that energy booms are just small parts of the big Cycle.

Watch the Golden Age of Fuel Oil.

The opportunities and timing are now for Blenders who can blend HSFO down to LSFO with diesel feedstock.

FO, LSFO, HSFO Markets:

Supply:

-спасибо России, or (Vitol and Litasco) Large Russian FO traders/exporters and the Russian Federation initiatives and fiscal incentives that I think are a big driver in the FO Market Structures see The Impact of Russia's refinery Upgrade on Global Fuel Oil Markets, Oxford Institute for Energy Studies, 2012

-Stricter environmental factors: from 3% to 1% to 0,1%S Emissions Control Areas (ECAs) and SOx Limited Zone (SLZ) that are pushing the LSFO-HSFO spread up, complex regulatory environment.

US/USG related: Since the last 15 years, US refiners have primarily focused on increasing their capacities to process heavier grades through coker, crackers and other processing expansions. Oil Majors' main focus is value-add products and are very disengaged from FO markets( if not totally from the Marine Fuel Market since 80's) Bunker has traditionally been a low-value by-product for refiners.

Demand: around 40% of the World's FO is consumed by vessels.

Forecast 2035 even if hitting Gas conversion targets, 63percent will still come from fossil fuel.

Shipping resists capital investment and added complexity of scrubbers, requires low cost fuel.In August, the HSFO premium to the front-month swap NWE ex-Rotterdam has breached 26,50$ the highest ever.

Demand for LSFO was 11mmt in 2010, doubling to 20mmt in 2011 and will more than 4x in 2014 to around by 2014, to meet the initial LSFO demand. -Robin Meech.

Marine bunkers do not have a thriving market in Houston. Most large vessels visiting the Gulf Coast will purchase their bunkers from offshore ports in the Caribbean that offer more competitive pricing. Bunker service in the HSC is mostly for short distance local traffic.

Houston is a Key HUB for Bunkering here's Why:

Location Location Location...

Shippers: You will find the hard way that Panama is full of extra's for this and that... though the fuel is load by via barge, you still got whacked with "pipeline" charges and If you believe that Houston is two far from Panama, think again. Ships are re-rerouted from Singapore to the Far East Russia to catch a fuel ARB.

Back to HFOTCO, it is the largest Gulf Coast’s fuel oil terminal plus is a crude bar tender for Houston's refineries, blending price-distressed crudes that are unable to reach refining markets in a timely and efficient manner.

The crude blending operations gives them steady and predictable cash flows, the location is a competitive advantage, plus they retain a real option on the LSFO-HSFO-Diesel spread if they step directly into proprietary FO trading.

Simonhttp://jacquessimon506.wordpress.com/