The icy “polar vortex” that swept across the US earlier this week brought freezing cold temperatures and a record 134 Bcf/d demand for natural gas on Tuesday (Jan 7, 2014). As a result natural gas prices on that day spiked over $70/MMBtu at the TRANSCO non-New York hub. New England buyers fared better - paying “only” around $35/MMBtu for their gas - largely because of a timely supply boost from a rare import cargo of LNG at the Canaport New Brunswick terminal. But these price spikes and severe stresses on the Northeast system demonstrate one more time how the pipeline network that delivers natural gas to New England remains inadequate. Today we conclude our analysis of the region’s gas pipeline situation by examining projects in the wings that together could provide the robust, reliable gas supply New England longs for.

Previously in this series we described how the hopes of Marcellus gas suppliers to move more of their product east are playing out in very different ways in metropolitan New York City and in New England (see Another Gassy Day in New York City). New pipeline capacity to deliver more gas from Pennsylvania, West Virginia and Ohio to the Big Apple and its environs already is installed and operating, easing the metro area’s supply crunch and (except for polar vortex market conditions) shrinking regional price “basis”. In the second episode (see Please Come to Boston—New England Needs More Pipelines – Part I)” we showed how, in contrast, New England’s gas supply remains constrained by insufficient pipeline capacity. We also explained how the regional electricity market’s failure to provide incentives to owners of gas-fired power plants to lock in long-term gas-pipeline capacity is hampering efforts to build needed gas-delivery infrastructure.

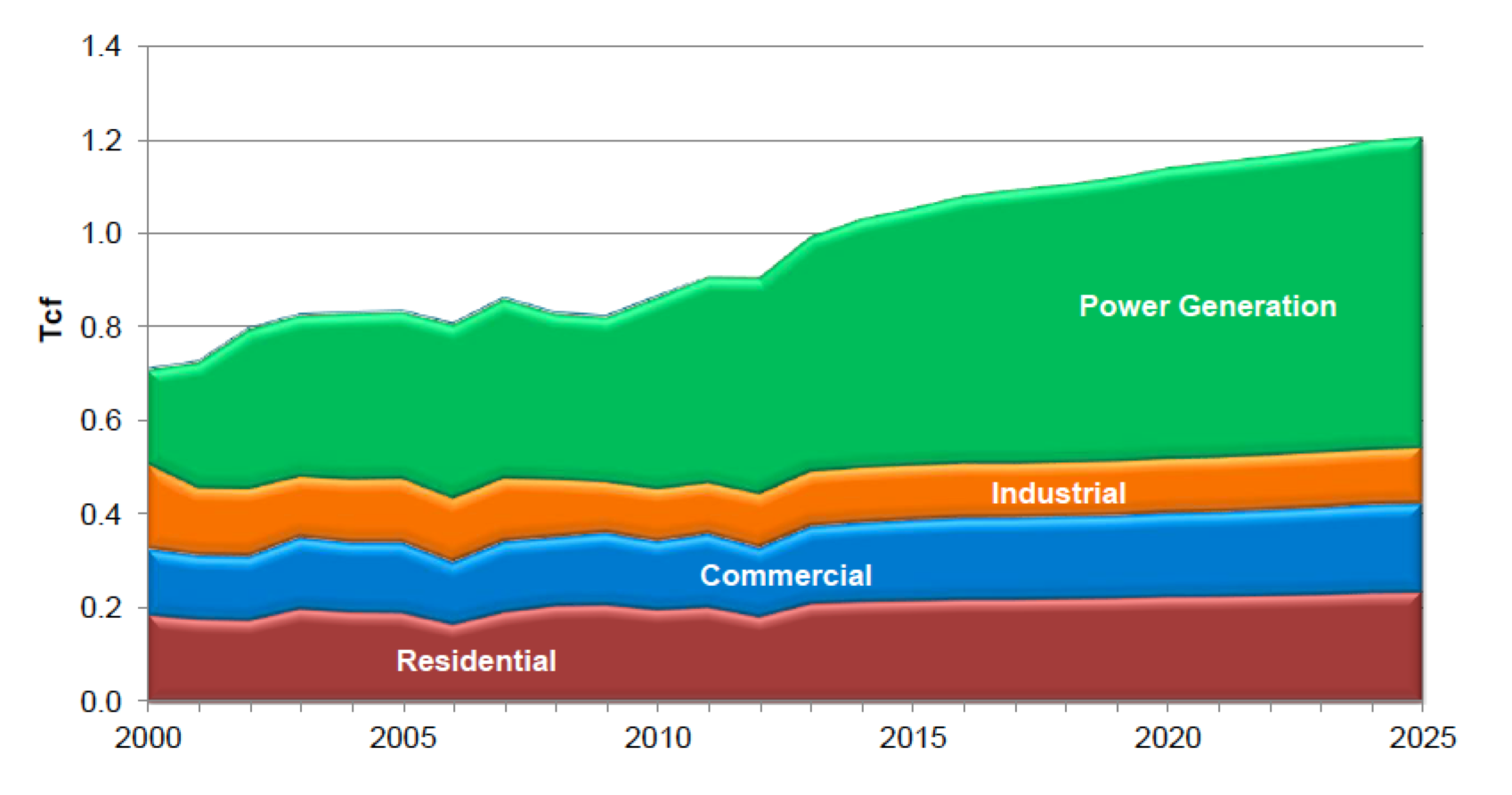

One thing is certain: Demand for natural gas in New England will continue rising, with the power generation sector leading the way. According to analysis prepared by ICF for the New England Independent System Operator (ISO) annual power sector gas consumption is expected to exceed 650 Bcf (up from 400 Bcf in 2012) to accommodate additional gas fired generation capacity (see Figure 1). Additional demand will also come from increased residential and domestic natural gas use.

Figure 1

Source: ICF International/NE-ISO

Despite the hurdles to building new pipeline capacity in New England that we discussed last time (see also Fuel for the City), two pipeline projects are well underway in the region, and are scheduled for completion by late 2016. One is Spectra Energy’s Algonquin Incremental Market (AIM) project, which will add up to 342 Mdth/d of capacity to the existing Algonquin Gas Transmission (AGT) pipeline through New York, Connecticut, Rhode Island and Massachusetts. The project will involve 21.4 miles of new pipeline, six new compressor units and other upgrades. The second project is the Connecticut Expansion on Kinder Morgan’s Tennessee Gas Pipeline (TGP). It will provide 72 Mdth/d of additional capacity into southwestern Massachusetts and northern Connecticut, and will involve 13 miles of new pipeline loops in the TGP 200 Line system in New York, Massachusetts and Connecticut, and the acquisition of an existing lateral pipeline.

However, while the AIM and Connecticut Expansion projects will certainly help meet New England’s rising demand for gas, they will not be enough, not by a long shot. So, what else is being planned to help bring the region’s gas-delivery infrastructure up to snuff, and what are the prospects for all—or at least much—of that new pipeline capacity being built? The Northeast Gas Association (NGA) provides a big-picture summary of what is on the drawing boards (see Figure 2).

About the song

“Please Come to Boston,” written and sung by Dave Loggins, was released in 1974; it rose to Number 5 on Billboard’s Hot 100 and to Number 1 on Billboard’s Easy Listening chart.

Comments

New England was nutso on that day. HQ is printing $$$ here: http://tinyurl.com/lw52yym . 1400MW to New England @$400/MW = $560,000/hr. Beats minimum wage

AGT 33.7$ basis HH it's 5YR high maybe all-time high... and well over NBP UK $11.20/mmBtu , TTF NL $10.92/mmBtu levels. AGT basis gives everett and canaport lng a business cases. The next day was monumental in power prices. PJM, NE, NY, MISO, ERCOT all had their fair share.

Some big problems came from the gas shortages for sure, and the shocker was the TET and Transco basis coming in above AGT. Unplanned coal and nuke outages exacerbated the already tight supplies.

Oil has been running around the clock during this cold stretch. Genscape explained Tet transco above AGT because of FO substitution in the Nepool. I don't totally buy it. I mean it might be part of the equation but was probably more due to the large draws off of transco-Z5 WGL that dried up the pipes even bedore the got to the Z6 and tet-M3 regions.

One trading consideration: trading model "demise", AGT is not "supposed" to be priced lower than transco= big problem for natural gas basis traders...

What's next: believe volaltity is still in the USNE corner. One lng spot cargo departed from trinidad ETA tuesday Jan 14th 10:30am destination: Canaport but check until the last minute for NWE, South-Europe to get nutso (we are in a LNG spot sellers market and they are very picky and can be juggling with price/destination details until the last min...

Simon

In reply to crazy NE by Simon Jacques

brian - thanks for your comments.

yes, IF hq were selling into the short-term market they might have been printing loonies, but all their deliveries are based on long-term contracts.

hq would be unable to get finacing for the transmission infrastruture if they were totally subject to new england's spot market -- hence the intense campaigns to get utilities to sign up for long-term contracts for the new, proposed lines from quebec.

if hq were to be paid spot prices for their power, they could barely make debt-service-coverage on the hvdc lines (new england on-peak, hub spot prices have been averaging $40 - $50/mwh in the past few years.)

yes, the quebeckers may be crying over money left of the table, but they are not willing to take the risk of being solely a price-taker.

paul

When you get price spikes in New England to ~$30, vs. ~$4 in PA, which shippers are able to capture that arbitrage?

Paul hope you like Brian's wink to HQ :), they still netted 400M$ from exports @50$/mwh av. in 12', I think because of very low marg. costs, their baseload can always bid agressively, indeed more difficult times for the NEPGA (not the New england professional gold assoc :-) how to kill two birds with one stone, ISO-NE isn't out of this mess ...

For conventional PPs key is spark spread, for lng terminals key is to lock a positive HUB Basis/International Gas Basis which will not happen all the time.

Dphelan, can't always physically because of line congestion but you mostly do it with DARTs spreads on the ICE and OTC gas swaps ex: AGT/TET. Simon