Eagle Ford crude production is increasing rapidly and the rush to deliver it to market has created an infrastructure boom. US Gulf imports are already declining as Eagle Ford and Bakken crude start to reach the Gulf Coast in significant quantities. Today we survey the transport costs that Eagle Ford producers pay to get their crude to market.

First a recap on the Eagle Ford series so far. In Part I we covered why the Eagle Ford shale is attracting producers like bees to a honey pot. Eagle Ford crude production is close to 600 Mb/d as of July 2012. We learned that Eagle Ford crude fetches better prices than similar quality Bakken crudes and touched on the discounts being applied to condensate. In Part II we began our review of Eagle Ford routes to market (either south to Corpus Christi or East to Houston) by describing large scale takeaway investments by Enterprise and Koch. In Part III we detailed additional takeaway projects being built or planned by Nustar, Magellen, Plains and Kinder Morgan. These projects - all expected online by 2013 have capacity for 1,650 Mb/d. Most forecasts show production increasing to about 1,200 Mb/d over the next five years - considerably below the takeaway capacity being built.

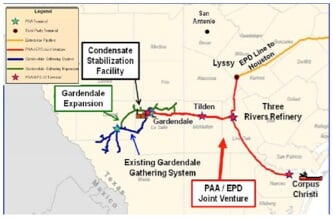

Yet the infrastructure announcements keep coming. On the day we posted that blog (August 9,2012) Enterprise and Plains All American announced a joint venture connecting their Eagle Ford infrastructure projects via a new 20-inch, 350 Mb/d capacity 35-mile pipeline segment from Three Rivers to Enterprise’s Lyssy station in Wilson County (see map below and story here). This link provides shippers with flexibility to divert crude and condensate from Gardendale in the Western section of the Eagle Ford either East to Houston on the Enterprise pipeline or South to Corpus Christi on the Plains pipeline. The joint venture is supported by an unnamed long-term shipper agreement covering approximately 210 Mb/d.

We turn our attention now to how Eagle Ford production gets to market. Just as we discovered in our analysis of the Bakken (see “The Buck Starts Here” Part III and Part IV), the value of crude oils to refiners depends on the availability of refining capacity that is suited to the crude type and the relative transportation cost to market.

Close by refineries in Three Rivers (Valero, 100 Mb/d), San Antonio (Nustar 15 Mb/d) and Corpus Christi (Flint Hills 279 Mb/d, Citgo 157 Mb/d, Valero 205 Mb/d) clearly represent primary targets for Eagle Ford crude and indeed these refineries are all in the process of making adjustments to their configurations to run greater quantities of Eagle Ford crude. The cost of pipeline transportation from Eagle Ford gathering points such as Gardendale down to Corpus Christi on the Gulf Coast (you can see the route in the map above) is approximately $1.70/Bbl plus whatever trucking cost it requires to get the crude to Gardendale. Delivery to Three Rivers from Gardendale on the TexStar pipeline is the same price ($1.70/Bbl) according to the TexStar Tariff. Don’t forget these tariff rates are estimates based on published data and will vary with individual circumstances and volume commitment.

Beyond the local refineries the obvious market for Eagle Ford production is PADD III Gulf Coast refining capacity - last pegged by the Energy Information Administration (2011 data) at 9.08 MMb/d. As we have noted, however, the new shale crudes like Eagle Ford and Bakken are very light sweet crudes that are not suited to refineries configured to run heavy crudes. In 2011 an average 7.5 MMb/d of Gulf Coast refining capacity was utilized. Of that 7.5 MMb/d, 2.8 MMb/d was light crude that could probably be replaced relatively easily by Eagle Ford. Of the light crude processed – 62 percent (1.7 MMb/d) was imported. With current Eagle Ford crude production at 600 Mb/d (July 2012) and expected to increased by 2016 to 1.2 MMb/d, the 1.7 MMb/d imports currently being processed in PADD III are the lowest hanging fruit for producers to target. The Eagle Ford transport costs should always compare favorably with these imported crudes from Africa or South America. US Domestic crude such as Eagle Ford and Bakken reaching the Gulf Coast is already making inroads into that import pool. A July 2012 Valero investor presentation states that Gulf Coast light/medium sweet crude imports averaged 952 Mb/d in 2011 and were reduced to 540 Mb/d during the first 4 months of 2012. Valero expect all Gulf Coast light/medium sweet imports to be pushed out of PADD III by 2013/2014. We at RBN agree.

As far as transport to these Gulf Coast refineries goes we noted the $1.70 /Bbl cost to transport Eagle Ford down to Corpus. The cost of transportation by pipeline from the Eagle Ford gathering stations to the Houston area is approximately $1.75 on the Enterprise crude pipeline system via Sealy. We estimate the cost to get Eagle Ford crude to St James Louisiana area refineries via pipe to Corpus Christi and then along the coast by barge to St James at $2.70/Bbl. From Corpus Christi, crude oil could also be shipped by barge to East Coast refiners for an estimated $12.25/Bbl.

For condensate producers the takeaway options are also by pipeline to Houston or Corpus. The only transport cost difference is pipeline tariffs. The published tariff rates exhibit the same prejudice against high API condensate that we saw from crude posters earlier in this series (see Part I). As a result there are gravity adjustment penalties to be paid when condensate travels on a crude pipeline. Another takeaway market for condensate is to ship to Corpus by pipeline, by barge to St James and then via pipeline to Edmonton Canada for use as diluent (see “It’s a Bitumen Oil- Does it Go Too Far?”). We estimate that cost to be $12.00/Bbl based on $1.70/Bbl to Corpus and a reported estimate from Corpus to Edmonton.

Comments

Will the need for barge transport from CC to St James be alleviated (by more than a marginal amount) by the reversal of the Shell Ho-Ho pipeline in est. 2013? If not, are there any other pipeline reversals in the works that you are aware of, or could there be an opportunity for a midstream company to build out infrastructure here given the potential overcapacity that is forthcoming within the Eagle Ford-area/Texas itself, assuming there is enough refining capacity (and as not to miss the point in the article, the right kind of capacity) to warrant more pipeline transport? As always, appreciate the articles and the insight.