WTI for prompt delivery closed $10.94/Bbl below Brent on Wednesday (October 23, 2013). Brent prices are disconnected from WTI and Light Louisiana Sweet because the Gulf Coast is awash with light sweet crude. West Coast crude prices on the other hand are supposed to march to a different tune – isolated from new shale and Canadian crude supplies and thus expected to continue tracking international Brent. But ANS prices on the West Coast have fallen to more than $5/Bbl below Brent in the past 2 weeks and seem to be tracking WTI. Is this just a temporary aberration or could it be signaling another step change in the road to US crude independence? Today we take a closer look at what’s going on.

US crude oil market analysis tends to be dominated by the spread between US domestic benchmark West Texas Intermediate (WTI) crude and international benchmark Brent – aka “The Spread”. However, the West Coast market is more concerned with pricing for the dominant grade consumed there - Alaska North Slope (ANS) crude. ANS is shipped to refineries in Washington State and California from the Valdez Marine Terminal at the southern end of the Trans Alaska Pipeline (TAPS). We have previously documented the decline in ANS crude production from its heyday 2MMb/d in the 1980’s to 520 Mb/d in 2012 (see After the Oil Rush). ANS production has actually improved to average 528 Mb/d so far in 2013 but it remains on a slow downward trend. Without changes to existing regulations and increased production, ANS is destined to be a dwindling resource supplied only to West Coast refineries (see Anchored Down in Anchorage).

In the past three years the US crude market East of the Rockies has been dominated by the disconnect between WTI and Brent prices that arose because new crude production from North Dakota and Canada got caught up in pipeline congestion in the Midwest. That disconnect led to WTI discounts to Brent getting up to $28/Bbl in 2011, averaging $18/Bbl in 2012 and then falling back to parity in the first half of this year (see Reunited). During that whole saga, ANS prices stayed more or less level with Brent crude. That is because the West Coast oil market is insulated from the Midwest – where crude prices were discounted – since there are no US pipelines across the Rockies. West Coast refiners had only limited access to lower priced US domestic grades (by pipeline from Canada and limited rail shipments from North Dakota) and had to pay international prices for their diet of ANS, Californian crude and imports from Latin America and Asia.

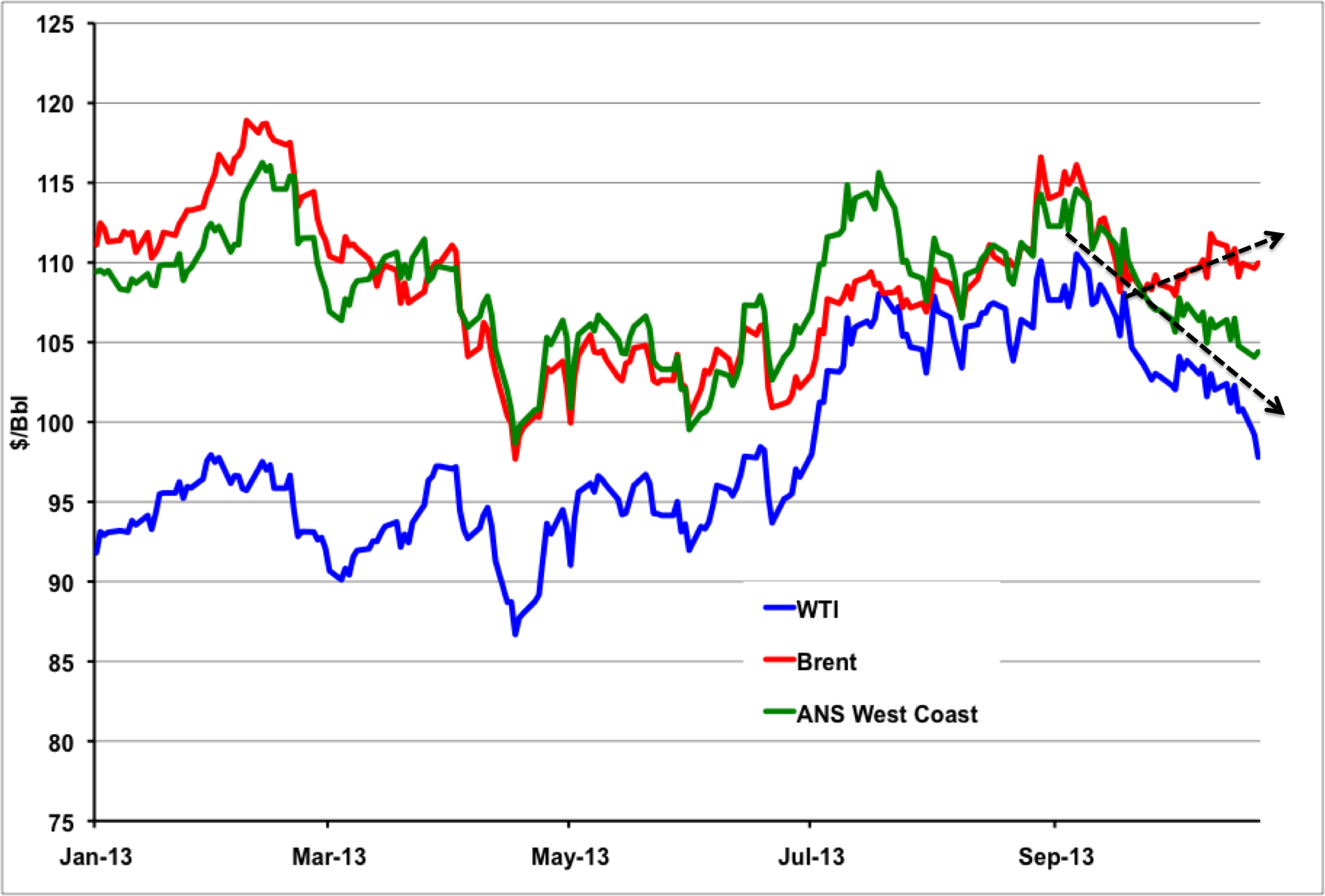

And it has been the prevailing sentiment among many analysts that even as the WTI discount to Brent narrowed sharply this July, ANS crude would continue to price close to Brent until sufficient quantities of lower priced crude from North Dakota and Western Canada made their way to West Coast refineries to compete with the flagship Alaska grade. That has not happened yet as we shall see. But in the meantime, as we described earlier this week, prices for Brent crude recently began to increase their premium to the Gulf Coast Louisiana Light Sweet (LLS) grade as well as WTI (see Goodbye Stranger?). Although the Gulf Coast disconnect could be attributed to a temporary surplus and high crude inventory levels during maintenance season, the surging Brent premium to LLS and WTI was also repeated unexpectedly on the West Coast against ANS. The chart below shows Brent (red line), WTI (blue line) and ANS (green line) since the start of 2013. Until the beginning of October ANS tracked pretty closely with Brent – following its historic pattern. In the past three weeks however Brent prices have increased while both WTI and ANS fell – moving in opposite directions (black dotted arrows on the chart). If continued, this trend would suggest that ANS prices are being driven more by US domestic crude rather than by competition from imports. That would be a startling development given West Coast fundamentals that still point to limited and falling production of ANS and very little competition so far from cheaper domestic US and Canadian crude.

Source: CME data from Morningstar and Alaska Department of Revenue

About the song

“What's Going On” is the title of the single from the 1971 album of the same name by Motown artist Marvin Gaye. It was written after Four Tops member Renaldo Benson, along with fellow Motown songwriter Al Cleveland, wrote the first version of the song that was given to Marvin Gaye for consideration. Gaye loved the tune but rearranged it and added a new melody, sharing in the songwriting credits on the song.

When Gaye played the song to Motown label head Barry Gordy, he hated it, saying the song was too political to be a hit. Motown executives Harry Balk and Barney Ales disagreed with Gordy's appraisal and helped Gaye record the song and put out the single. It immediately became a smash hit, going to #1 on the Hot Soul Singles chart and #2 on the Billboard Top 100 chart. Barry Gordy was stunned by the success of the single and gave Gaye the green light to record and produce a complete album. The album was recorded between June 1970 and May 1971 and became the first Marvin Gaye album to reach Billboard's Top Ten in the Top LP category, and peaked at #6, staying on the charts for a year.

Marvin Gaye helped to shape the sound of Motown in the sixties with a string of hit singles. What's Going On was a revolutionary departure from focusing on hit singles to shifting toward an album-oriented consciousness with a recurring social theme. Marvin Gaye died in 1984 at the age of 44, fatally shot by his father at their Los Angeles home. Among his many awards is a Grammy Lifetime Achievement Award, induction into the Rock and Roll Hall of Fame, and a star on the Hollywood Walk of Fame.

Comments

If this hypothesis were true, wouldn't you have expected ANS to widen vs Brent when WTS was very weak (in Dec '12/Jan '13)? Rather than WTI, I found it more interesting to chart ANS against LLS -- the two have moved in lock step for several years. When LLS rose to its premiums against Brent earlier this year, ANS followed. I wonder if there is a link between LLS & ANS, such that any Gulf Coast overssupply story that pressures LLS will also pressure ANS.