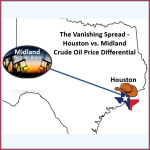

The Midland-to-Houston crude oil differential has undergone a dramatic round trip over the past several months. As the charts below show, the spread surged to its highest levels in years during the early months of the Iran war before collapsing back toward historical norms. After averaging less than $0.35/bbl through most of 2023-2025 (left graph), the differential briefly exceeded $3/bbl on a daily basis in April 2026 (right graph) and pushed the monthly average to levels not seen since major Permian pipeline capacity constraints were a recurring concern back in 2018-19.

Featured Articles

- Analyst Insight

Geopolitical Risk Premium Drives Surge in Crude Prices To Above $90/bbl

The start of March brought extraordinary volatility to crude markets. Multiple global benchmarks and regional grades posted sharp gains, with several trading at or near recent highs.

- Blog

How’s It Going to Be – How a Prolonged Conflict with Iran Could Disrupt U.S. Gasoline, Jet and Diesel Markets

The U.S. is seeing softer domestic demand for traditional fuels, but pockets of the country remain highly dependent on imported gasoline, jet fuel and diesel. Today, we’ll zero in on which PADDs are at the highest risk for shortages and price spikes if the Iran war drags on for an extended period.

- Analyst Insight

International Brent versus Domestic WTI Crude Oil Price Differential Blowout

The price differential between Brent and WTI has widened sharply in the past few days, reaching levels not seen in over a decade as the Iran war has created a growing gap between international seaborne and domestic inland crude markets.