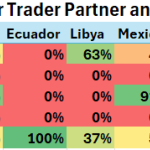

Crude imports dropped to 6.1 MMb/d last week, declining by 1.6 MMb/d after a previous increase of 1.17 MMb/d. Imports into PADD 3 were halved, falling to 1 MMb/d, partly due to a decline in Mexican supplies by 615 Mb/d and Colombian imports by 270 Mb/d; both countries send the majority of their barrels to the U.S. Gulf Coast (recent volumes shown below). On a positive note, Canadian imports increased by 220 Mb/d to reach 4.08 MMb/d, surpassing 4 MMb/d for the first time in ten weeks.

Featured Articles

- Blog

Tighten Up - The Stars Align and the Western Canadian Heavy/WTI Differential Narrows

Any number of things can impact the price of specific types of crude oil at various locations — supply interruptions, takeaway constraints and refinery outages, to name just a few. Every so often, the stars align and just about all those factors narrow the differential between, say, Western Canadian Select (WCS) and West Texas Intermediate (WTI) at the U.S. Gulf Coast to near-record levels. Well, that’s happening now, for the first time in five years. In today’s RBN blog, we discuss the shockingly small WCS/WTI differential and what’s driving it.

- Blog

Everybody Hurts - Trump's Tariffs Would Hurt Canadian Oil Producers More Than U.S. Refiners

Tariffs have served as a cornerstone of President Trump’s economic vision. In the campaign, he said he could impose tariffs as high as 25% on all imported goods from Canada — including crude oil — and he could deliver on that promise at any time. This has raised concerns, especially for Canadian producers and U.S. refiners, who depend on the efficient and economical movement of barrels between the trading partners. In today’s RBN blog, we look at how much Canadian crude oil flows to the U.S., how those imports could be affected by tariffs, and how Canadian producers and U.S. refiners would share the financial impact.

- Blog

Comin' to America, Part 2 - Shale, Oil-Sands Production Gains Impacting U.S. Refineries' Crude Slates

Ten years ago, East Coast refineries imported virtually all of the crude oil they needed — 60% from OPEC, 21% from Canada, and 19% from other non-OPEC countries. Only five years later, in 2015, the tables had turned. PADD 1 refinery demand for crude remained unchanged at 1.1 MMb/d, but only 14% of the oil refined there came from OPEC, 23% from Canada, and 21% from other non-OPEC countries — the other 42% was either railed in from the Bakken or shipped in from the Eagle Ford and Permian. But the changes didn’t end there. Imports rebounded sharply in 2016 and 2017, when new pipelines were built out of those basins that pulled barrels away from PADD 1 and into more competitive refining markets. In the fall of 2020, imports are falling back again but for a different reason — with COVID-19 demand destruction and other woes, East Coast refinery demand for oil is down by almost half, with more cuts on the way. Today, we continue a series on U.S. oil imports with a look at the East Coast.