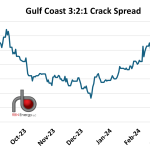

Utilizing data from RBN’s TradeView publication, the 3-2-1 refinery crack spread, the difference between the price of refined products (gasoline and diesel) and the price of crude oil in the Gulf Coast, rose more than 40% in the week ending March 15 (red dashed oval in chart below), its largest single week increase since mid-December, and the fifth largest weekly increase in the past four years. With the spread at just under $29/bbl as of March 15, this is its highest value since mid-September. In its simplest form, the 3:2:1 crack spread represents a rough measure of refinery profitability from the processing of crude oil into refined products such as gasoline and diesel, the two most widely used refined products in the U.S. Note that the 3:2:1 spread is strictly based on prices and does not include the cost of processing different crude oil streams and other factors which can be specific to each refinery and affect overall profitability from the production of gasoline, diesel, and other products.

Featured Articles

Fly Me To The Moon – Refining Margins Boom as Crude Inventory Hits the Roof

U.S. crude stocks are at their highest level in over 30 years and the contango market pricing structure continues to encourage increases in the stockpile. No one knows exactly how much storage space remains. The surplus is keeping U.S. crude prices low compared to international rivals but petroleum product prices (gasoline and diesel) are climbing higher, having bounced back from recent lows. Refining margins are sky high as bad weather and outages hamper operations. But as we describe today, the crude surplus remains a dark cloud on the horizon.

The Midwest Crack Spread Margins Really Make You Feel Alright!

Ever since US crude production began to increase in 2009 after 40 years of decline from its peak in 1970, refineries have been processing higher crude volumes. This summer (2014) crude processing volumes have been higher than at any time since the Energy Information Administration (EIA) began keeping records in 1982. Abundant supplies of reasonably priced crude in all regions as well as low refinery fuel costs are giving US refiners good reason to crank up their output. So much so that in the Midwest refinery output reached over 100 percent of capacity early in July. Today we describe the refining bonanza and how things might change in the not too distant future.

Cracking Up, Part 2 - Will High Crack Spreads Be Enough to Balance Refined Products Markets?

U.S. diesel inventories are at their lowest level for May since 2000 and East Coast stocks recently hit their lowest mark for any week or month since the EIA started tracking them in 1990. Crack spreads for diesel — and, more recently, for gasoline — have gone parabolic, giving refiners the strongest financial signal ever to produce more diesel and gasoline as we enter the summer travel season. More jet fuel too. The problem is, U.S. refineries already are running flat-out. And Europe? It’s facing big cuts in crude oil and refined-products imports from Russia as well as much higher prices for — and possible shortages of — oil and natural gas, the latter being the primary fuel for operating refinery hydrocrackers, which upgrade low-quality heavy gas-oils into high-quality diesel, gasoline and jet. It’s a mess, and not easily fixable, as we discuss in today’s RBN blog.