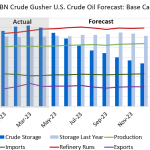

In response to the Russian invasion of Ukraine and subsequent sanctions, the US Strategic Petroleum Reserve (SPR) was called upon to ease the supply-short market. As a result, an unprecedented 180 MMbbl of crude oil was released onto the market, which still saw some of the highest crude prices we’ve seen in years. Now, as crude oil prices react to foreign and domestic economic news, the fundamental drivers of our crude market appear to remain bullish. As RBN’s Crude Oil Gusher team works on our crude oil forecasts, it has become more and more difficult to balance the scales without taking a big bite out of the commercial crude inventories this time.

If we look at our current base case forecast, we see that by December crude production will reach 12.7 MMb/d, and imports will average 6.5 MMb/d, exports will average 4 MMb/d, and refinery runs will average 16 MMb/d for the remainder of the year. At these rates commercial crude inventories will need to release 202 MMbbl or 43% of the current stockpile to make up the supply shortfall. A massive draw like this seems improbable though, as the start of such pulls would likely drive prices up and incentivize market players to adjust course, but one thing is for sure, if the current state of surging exports and sluggish supply growth doesn’t change, it could spell trouble for the nation’s commercial storage supply.