Crude oil distribution to Houston area refineries is still being re-plumbed to reflect the ongoing transition to domestic supply. Although plenty of new pipelines provide access for new crude flows into Houston, logistic challenges arise from a crude quality mismatch with refinery configurations. The handling of condensate – whether lightly processed for export or refined in a splitter is also increasing infrastructure overhead. Today we look at new crude infrastructure challenges in the Houston area.

In the First Episode of this series we reviewed the evolving crude supply demand balance into the Houston refining region that has 9 refineries and two new 50 Mb/d condensate splitters that are processing an estimated 2.4 MMb/d of crude between them. Crude supplies into Houston refineries used to be predominantly made up of waterborne imports but rising U.S. and Canadian production is increasingly replacing these overseas imports. In 2015 through May remaining waterborne imports were 0.9 MMb/d versus overland pipeline supplies that we estimated at about 1.5 MMb/d. Another 100 Mb/d of waterborne crude and condensate from the Eagle Ford are delivered to area docks by barge and tanker. These incoming supplies roughly balance with refinery demand. However - incoming pipeline capacity is less than 50% utilized even as more than 1 MMb/d of new pipes are expected online by early 2016 - suggesting that a lot more incoming crude is expecting to navigate the Houston area in the future and that infrastructure reconfiguration to accommodate new flows remains necessary. In this episode we look at logistics issues facing Houston and how these might be addressed.

A key crude logistics issue for the Gulf Coast refining industry in general and Houston in particular is overcoming the mismatch between refineries built decades ago in an era when available crude quality was expected to get heavier (i.e. with a lower API degrees gravity) and more sour (with a higher sulfur content) and new crude supplies from domestic shale basins that are light or ultra-light (higher API degrees gravity) and sweet (low sulfur). What that means today is that U.S. refineries – as configured – can only absorb so much domestic light crude and need to continue importing heavy and medium grade crudes in order to optimize processing. We discussed the topic in detail at our “Surviving The Flood” conference with Turner Mason & Company a year ago in Houston (August 2014 – see Here Comes The Reckoning Day). For Houston region refineries that means all remaining waterborne crude imports are medium and heavy crudes and that those imports are not likely to be totally replaced by domestic crude anytime soon because the refineries can’t handle much more light crude. But within that wider issue there are a lot more subtle changes going on that complicate the flow of crude in and around Houston.

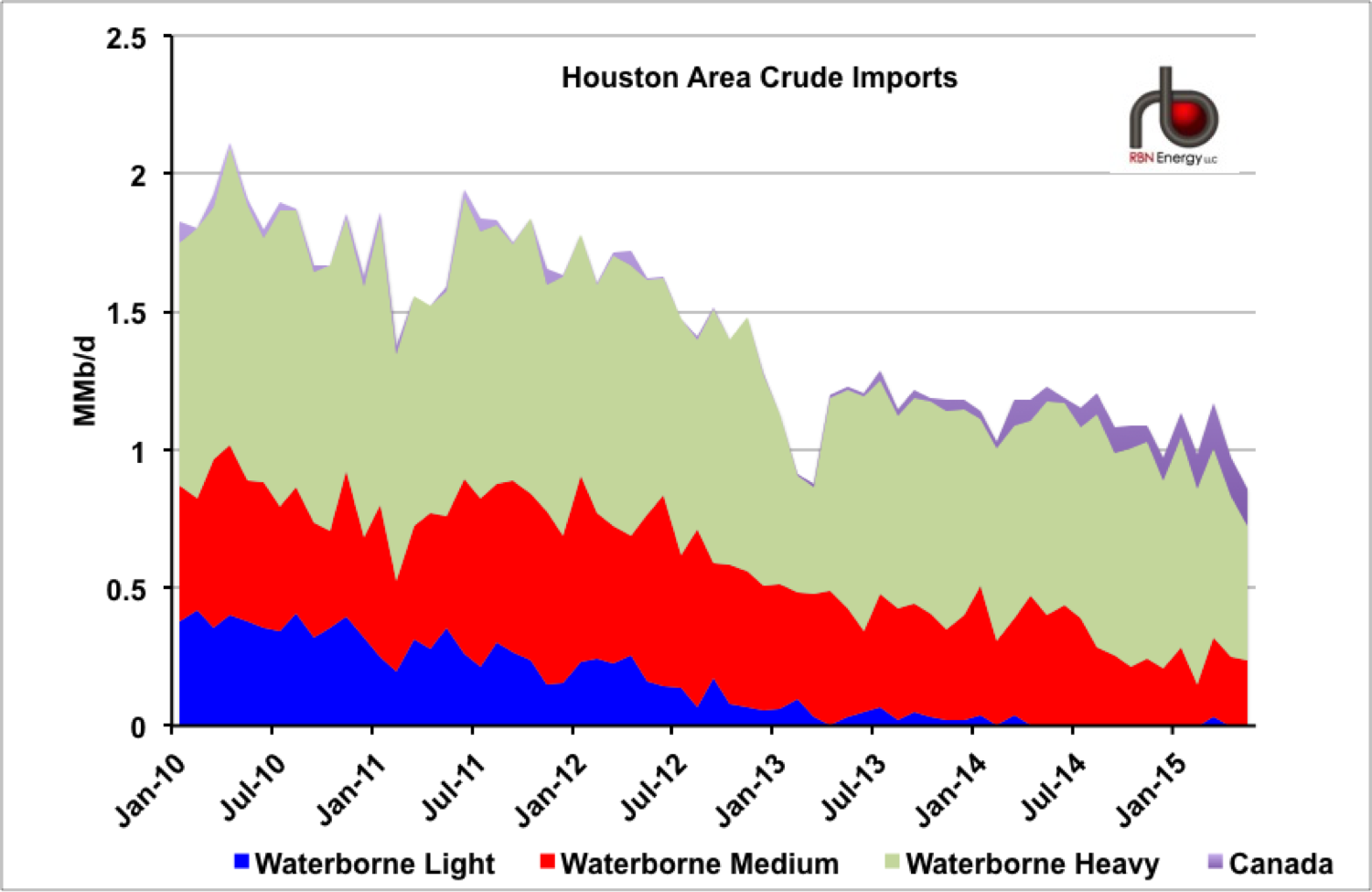

The chart in Figure #1 is based on data from the Energy Information Administration (EIA) monthly company level crude imports report through May 2015. It shows the history of waterborne crude imports to the 9 Houston refineries as well as area crude terminals since January 2010. You can see that imports of light crude (blue shading) fall from about 400 Mb/d in early 2010 down to a trickle by the end of 2013. Incoming domestic supplies have replaced these light imports. Medium and heavy crude imports (red and light green shading) fell over the same period from an average of 1.4 MMb/d in 2010 and 2011 to 1.0 MMb/d in 2014 and 0.9 MMb/d through May 2015. Lighter domestic crudes have replaced some of those medium and heavy supplies.

Refiners have blended very light crudes (including super-light crudes with an API over 55 – known as condensate) from the South Texas Eagle Ford basin with heavier imports. That has made sense because domestic light crude supplies exceeded demand – keeping their price at a competitive discount such that refiners can improve margins by processing such blends. The process of blending light and heavy crudes requires adequate crude tankage for blending and storage that – as we shall see later in the series – presents a logistics challenge for Houston refiners that infrastructure developers are still working to overcome. In addition – in the past year or so as the Enbridge/Enterprise Seaway Twin pipeline came online, increased supplies of Canadian heavy crude have been delivered to Houston (some heavy Canadian crude has also been delivered by rail – to the Kinder Morgan/Watco Greens Point terminal on the Ship Channel). The purple shaded area on the chart represents these Canadian imports that increased from nothing in 2013 to an average 60 Mb/d in 2014 and 129 Mb/d through May 2015. We discussed these increased Canadian imports reaching the Gulf Coast recently (see They Did It Seaway) as well as pipeline constraints in Western Canada that are preventing increased supplies reaching the Gulf Coast this year (see You Can Leave Your CAPP Off). More Canadian heavy crude is expected to flow into Houston when the 700 Mb/d Houston Lateral to the TransCanada Cushing Marketlink comes online – currently expected at the end of this year. But increased flows of heavy crude into Houston by pipeline will tend to complicate crude distribution logistics because this type of crude is typically segregated from lighter shale crude and therefore requires separate infrastructure.

Figure #1; Source: EIA, RBN Energy

About the song

Stairway to Heaven from rock legends Led Zeppelin’s fourth studio album was released in 1971. Composed by Jimmy Page and Robert Plant the song is often rated among the greatest rock songs of all time.

Comments

In reply to Brent import by Marcel Depart

Yes there is still crude imported by national oil companies like Saudi Aramco, PEMEX and PDVSA that are invested in U.S. refineries as well as sometimes for quality reasons (see https://rbnenergy.com/there-is-a-light-that-never-goes-out-the-resilience-of-light-crude-imports-to-the-gulf-coast )

But if U.S. continues to restrict exports then domestic crude prices will continue to be discounted versus imports meaning an overseas producer gets less for their light crude in the U.S. than in other markets such as Europe and Asia. Over time that tends to mean they will only sell the type of crude into the U.S. that is more in demand here than anywhere else - namely heavy crude - for which more U.S. refineries are configured than any other region.