Permian crude production is expected to increase 28 percent between 2013 and December 2018 to 1.8 MMb/d (Bentek). Existing pipeline takeaway capacity and local crude consumption are currently barely enough to handle production of 1.4 MMb/d. However, planned new pipeline capacity should comfortably handle output by the end of 2015. Today we review the impact of new Permian takeaway capacity.

In the previous episode in this series we looked at Permian Basin crude production, existing pipeline takeaway capacity and refinery consumption (see Rock The Basin – A Tight Pipeline Balance For Permian Crude). We noted the tight balance between increasing production and pipeline capacity – with both at about 1.4 MMb/d – leaving Permian crude prices vulnerable to pipeline or refinery disruptions. This time we look at new pipeline capacity coming online in the next two years out of the Permian and compare it to the production forecast.

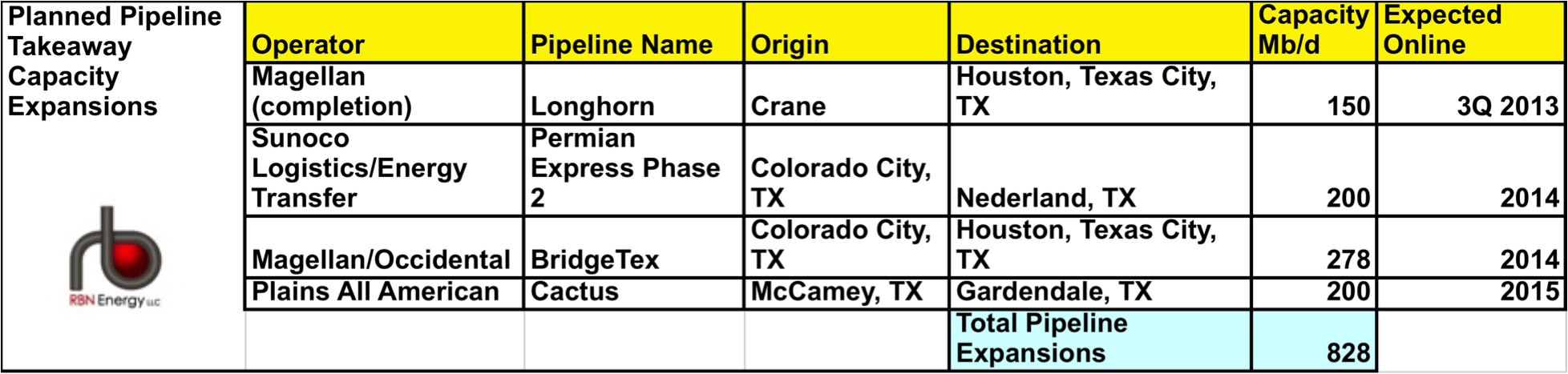

The table below lists four new or expanded pipeline projects currently planned to increase takeaway capacity from the Permian Basin. If these projects are completed, they are expected online by the end of 2015. We covered the first three of these pipelines in our original series on Permian (see The New Adventures of Good Ole Boy Permian – The Race to the Gulf Coast). There is an updated version of the map from that blog further below here. The Magellan Longhorn pipeline from Crane to Houston is already operating at 75 Mb/d but will be expanded to flow up to 225 Mb/d by the end of 2013. The 200 Mb/d Sunoco Logistics/Energy Transfer Partners Permian Express Phase 2 pipeline is expected online during the first half of 2014. Permian Express 2 will run parallel to the existing Sunoco West Texas Gulf pipeline between Colorado City and the Nederland, TX terminal that serves the Beaumont/Port Arthur refining complex. Sunoco are also canvassing shipper interest in an extension of the Permian Express to St James, LA. The 278 Mb/d Magellan/Occidental BridgeTex pipeline is a brand new pipeline that will run between Colorado City and the Magellan terminal in East Houston and is expected online in mid-2014. Magellan is building out pipeline connectivity to Houston and Texas City refineries from their East Houston terminal (see The Stocks of Magellan).

Source: RBN Energy

The fourth pipeline in the table is the newly announced Plains All American Cactus pipeline that would run between McCamey, TX and Gardendale, TX. The proposed 200 Mb/d Cactus pipeline will link Permian takeaway capacity with crude pipeline takeaway infrastructure for the Eagle Ford basin in South Texas. The map below shows the new pipelines in the table with the Cactus route marked with a blue dotted line. The Cactus line will terminate at Gardendale - a gathering system hub for the oil and condensate rich window of the Eagle Ford. Plains already operate a pipeline from Gardendale to Three Rivers that links to another Plains pipeline carrying crude south to Corpus Christi on the Texas Gulf Coast. Plains is also currently completing construction of a new joint venture pipeline with Enterprise Products Partners to link their Three Rivers terminal to the Enterprise Crude and Condensate pipeline that runs from Lyssy, TX to Houston. These existing pipelines linking Cactus to Three Rivers, Corpus and Houston are marked in solid blue on the map. Provided the Cactus pipeline is permitted and approved Plains expect it to be in service during 2015.

Comments