It is a vast understatement to say that the natural gas world is in a state of significant transformation in the United States. On the surface, the shale production story and its impact on supply, and by extension demand on a national basis seem profound as is, but the truly dramatic stories are those played out on a more granular, regional level. Stories played out not just on an annual basis but also on a seasonal basis. Today we look at changing northeast gas storage requirements.

The Northeast region is going through substantial change that requires new infrastructure to adapt to a ‘new’ supply dynamic. Bob Bookstaber’s recent blog series (see Northeast Gas Parts I, II, III, IV) covered the myriad of pipeline projects aimed at the region in the coming years. In this post we focus on the storage challenges that arise from the new Northeast supply dynamic.

From a big picture perspective storage for natural gas bridges the delta between a ratable (consistent, for the most part) supply and seasonal/inconsistent winter weighted demand. Gas is injected in the summer and withdrawn in the winter to accommodate these seasonal variations. Weather and physical constraints send signals to the market that create price incentives to inject or withdraw gas. The shale phenomenon is driving shifts in those price signals.

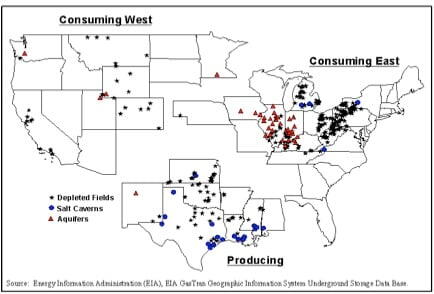

First a short primer on natural gas storage. The Energy Information Administration (EIA) breaks US natural gas storage facilities into three broad regions: the Consuming Northeast, the Producing Region and the Consuming West (see the map below). Storage in the United States is primarily comprised of three types (see table below the map); depleted reservoirs (big and slow), salt caverns (small and fast ) and aquifers (closer to big and slow than small and fast).