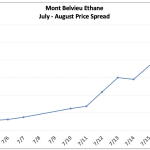

The NGL market has been abuzz over the last couple of weeks with the run-up in Mont Belvieu ethane and NGL prices. Mont Belvieu spot ethane prices hit a high of 46 cents/gal on July 16 and currently sit around 40 cents/gal, up about 40% from the beginning of the month. The market rally has been most pronounced in the prompt (current) month prices which has widened backwardation. As shown on the chart below, the August “out month” discount to July increased from 1 cent/gal at beginning of the month to 8 – 10 cent/gal currently. The strong front-month prices are reportedly being driven by midstream buying to cover contractual obligations. The prompt physical market has also been strong with “wet” or “ratable” barrels trading at a 1.5-2 cents/gal premium over any month barrels.

Featured Articles

Fly Me to the Moon - Ethane Prices Rocket into Space, then Crash to Earth on Tuesday. What Happened?

In just over a month, the price of Mont Belvieu purity ethane doubled, from 19 c/gal to 39 c/gal on Friday. Sure, the price of natural gas was up about 15% over the same period. But that increase was nowhere near ethane’s, so it was certainly not the price of gas that was making ethane take off. In fact, with ethane rocketing into space and gas prices still in the dumper, the ethane-to-gas ratio — a key measure of the value of ethane — skyrocketed, soaring from 1.2X in mid-June to 2.2X on Friday. A ratio at this level has only happened twice before in the past decade: once in 2018 due to a collision between fractionation capacity and new petchem plants coming online, and then again in 2020 during the COVID petchem demand surge. But the most recent price surge didn’t last long. On Tuesday ethane came back to earth, crashing 22% in a single day, and the ethane-to-gas ratio deflated down to 1.6X. So what’s happening? There are a lot of conspiracy theories out there that we won’t repeat here. Instead, in today’s RBN blog, we’ll lay out what we think are the most likely contributing factors behind this wild ride.

Hotel Fractionation - Far-Reaching Impact of the Unprecedented Shortfall in NGL Fractionation Capacity

Y-grade, welcome to the Hotel Fractionation. You can check in any time you like, but you can never leave! OK, so that’s a bit of an overstatement. But there is no doubt that the U.S. NGL market has entered a period of disruption unlike anything seen in recent memory. Mont Belvieu fractionation capacity is, for all intents and purposes, maxed out. Production of purity NGL products is constrained to what can be fractionated, and with ethane demand ramping up alongside new petchem plants coming online, ethane prices are soaring. But that’s only a symptom of the problem. Production of y-grade — that mix of NGLs produced from gas processing plants — continues to increase in the Permian and around the country. Sooo … If you can’t fractionate any more y-grade, what happens to those incremental y-grade barrels being produced? How much can the industry sock away in underground storage caverns? Does it make economic sense to put large volumes of y-grade into storage if it will be years before it can be withdrawn? — i.e., “you can never leave.” And what happens if y-grade storage capacity fills up? Today, we begin a blog series to consider these issues and how they might impact not only NGL markets, but the markets for natural gas and crude oil as well.

Wild Ride - NGL Production Growth vs. Constrained Fractionation Capacity - Drilling Down into the Details

To fire on all cylinders — especially during a period of strong high crude oil prices and rising production — the U.S. energy sector depends on midstream infrastructure networks that can efficiently handle the transportation and processing of every type of hydrocarbon that emerges from the wellhead. It’s no secret that rapid production growth in the Permian has left the red-hot West Texas play short of crude-oil pipeline capacity, and midstream companies there have also struggled to keep pace with natural gas takeaway needs too. What’s less well known is that fractionation capacity at the all-important NGL hub in Mont Belvieu, TX, is nearly maxed out, and that some Permian producers — and others — are now scrambling to find other places to send their incremental NGL barrels for fractionation into purity products. We put this issue front-and-center earlier this week in Hotel Fractionation. Today, we discuss highlights from the first of two planned Drill Down Reports on fractionators and other key assets at the nation’s largest NGL hub, and the potentially broader effects of a fractionation-capacity shortfall.