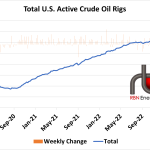

Lower 48 crude oil production was back up 100 Mb/d to 11.9 MMb/d last week, while Alaskan output was mostly flat near 400 Mb/d. This means total U.S. production was up to 12.3 MMb/d, matching recent highs. The increase was mainly due to a re-benchmarking, which is an adjustment to reported volumes after the EIA compares its Short-Term Energy Outlook (STEO) and its Petroleum Supply Monthly (PSM) with current data and identifies any major discrepancies. This re-benchmarking increased volumes by around 105 Mb/d. The U.S. has the means to increase supplies, but with stagnant rig growth this year, there doesn't seem to be much of an appetite for it from producers. This, in turn, leaves many earlier forecasts of domestic supplies reaching 13 MMb/d by the end of 2023 likely just a pipe dream.

Featured Articles

Crude Supply Boost Not The Real Fix It Appears

EIA's New Crude-Supply Figures Add Visibility to Market

Un-Thinkable - Is the Market Ready for 100-Bcf/d U.S. Natural Gas Production?

The once unthinkable level of 100 Bcf/d for U.S. natural gas production is just around the corner, it would seem. Lower-48 gas production last week hit a new high of 96.4 Bcf/d, after surpassing 95 Bcf/d not too long ago (in late October). That’s remarkable considering that production was only 52 Bcf/d just 12 years ago. Gas demand from domestic consumption and exports this year has set plenty of records of its own, but the incremental demand has not been nearly enough to keep the storage inventory from building a significant surplus compared with last year. CME/NYMEX Henry Hub prompt gas futures prices tumbled nearly 40 cents last week to $2.28/MMBtu, the lowest November-traded settle since 2015. Today, we break down the supply-demand fundamentals behind this year’s bearish storage and price reality.