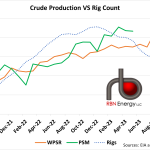

The Weekly Petroleum Status Report (WPSR) showed that Lower 48 production shot up 400 Mb/d last week to 12.2 MMb/d, the highest total volume since March 27, 2020, right before the COVID crash. Total U.S. production was listed at 12.6 MMb/d when adding in Alaskan supplies. This is also the largest single week jump that was not a rebound from a recent storm related loss, since November 2018. The increase was due to re-benchmarking, which is an adjustment to reported volumes after the EIA compares its Short-Term Energy Outlook (STEO) and its Petroleum Supply Monthly (PSM) with current data and identifies any major discrepancies. This re-benchmarking boosted production by 417 Mb/d, which is needed by the industry following the largest weekly crude inventory draw in history. The increase finally brings the production numbers more in line with the Petroleum Supply Monthly, which has shown average production in the first five months of the year to be at 12.64 MMb/d.

Oil rigs continue to fall, now sitting at just 525 active rigs. The last time there were only 525 active rigs operating in the U.S., total crude production was at 11.6 MMb/d, a full 1 MMb/d lower than today. Again, much of the increase in production reported today was simply the WPSR more accurately reporting what the monthly data has been showing all year long, but that does not mean this increase is here to stay. Unless the active-rig-to-production ratio is becoming significantly more efficient, or producers are able to reduce the decline curve of existing wells, it would seem logical that production has to follow the decline in rig activity sometime in the coming weeks. This should in turn continue to support higher prices as demand remains strong.