Last week once again brought extreme volatility to the crude oil market, echoing chaos not seen since the COVID era. Early losses stemmed from fears of a global trade war, weak economic outlooks, and rising oil supply, worsened by President Trump’s hardline stance on China and OPEC+’s supply hike, with WTI front-month futures hitting a four-year low of $55.12 midweek. However, a surprise 90-day tariff pause triggered a sharp rebound, with WTI ending Friday at $61.50 and Brent ending the week at $64.76 as mentioned in this week's TradeView report. Both benchmarks closed the week with slight declines among economic concerns and lingering oversupply fears, reinforced by continued deflation in Chinese consumer prices.

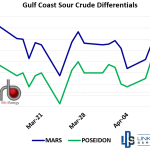

While weakness was seen in outright crude prices throughout the week, Mars rallied to a four-week high Friday as the sour supply tightened. After starting off the week at a premium of $0.43 above NYMEX-CME Domestic Sweet (DSW) — the commonly quoted prompt month futures contract price of crude oil, Mars found short-term support mid-week following the shutdown of Keystone pipeline, before rising to end the week at a premium of $1.14/bbl over DSW. Mars serves as a key price indicator and benchmark for medium sour crude oil produced offshore in the Gulf Coast, reflecting the availability of sour crudes in the region and correlating with heavier crudes that the United States imports from other countries to run its complex domestic refineries.