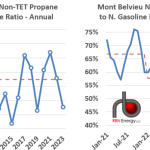

Before the shale era, the price relationship between two NGLs – propane and natural gasoline, was relatively stable, at about 65%. Both varied primarily with crude prices, with the relationship diverging during periods of high propane demand such as cold winters. But the shale revolution put an end to that stable relationship, with massive production growth resulting in propane surpluses requiring significant exports to balance the market, but with inadequate export capacity available in some years. As shown in the left graph below, since 2012, the ratio of propane to natural gasoline has vacillated between a low of 42% in 2015 to a high of 67% in 2021, with the most significant determinants of that relationship the demand for propane in international markets and the capacity available to meet that demand and relieve domestic propane surpluses through exports.

Featured Articles

Can't Get Enough of It - Are We on the Verge of a Propane Supply Shortfall?

During the last two weeks of April, a barrel of propane in Mont Belvieu was more expensive than a barrel of WTI crude oil in Cushing. That’s never happened before. You might think that such an aberration could be blamed on the wacky April-May 2020 COVID crude market, but that is only part of the story. Propane production is falling and pre-COVID projections of continued supply growth are out the window. But new gas processing plants, pipelines, fractionation facilities, dock capacity and downstream demand have come online in recent years, in anticipation of those ill-fated additional supplies. Already we are seeing flows, price relationships and differentials convulsing in response to the new reality, and projections of future supply/demand imbalances suggest a previously unthinkable possibility: a market that can’t get enough propane supply, especially if the winter of 2020-21 is a cold one. In today’s blog, we will explore the evidence of these market developments that is already visible and look to what may be ahead for propane supply and demand.

Jumpin' Jack Flash, It's a Gas: Propane - Propane Markets Writhe Due to Supply/Demand Uncertainty

So far in April, there was an unexpected run-up in propane prices early in the month, followed by a 21% swoon in the past 15 days of trading. The forward curve suggests smooth sailing from now through next winter season, but that seems unlikely, given recent market developments. Propane inventories, which are supposed to be building this time of year, actually fell last week, putting stocks at 16.9 MMbbl below this point in 2020, according to EIA statistics released last week. The data also showed that weekly exports spiked to the second-highest peak of all time at 1.7 MMb/d, while production declined two out of the past three weeks. And just over the horizon, there’s the potential for a big increase in Chinese propane demand as new petrochemical plant capacity comes online over the next three years. Today, we look at how these issues are likely to shape the propane market over the next few months and suggest that you consider attending our upcoming virtual conference, where we will pose these questions to industry leaders from production, midstream, exports, and retail market segments.

What's Price Got to Do with It - High Propane Prices Fail to Put the Brakes on Exports

The high-demand season for propane is just around the corner: crop drying, then winter heating demand. This is when propane marketers make most of their money; so under normal circumstances it’s a happy time, when all participants across the supply chain are making last-minute preparations for the season of peak propane demand. But this year is different. There is palpable concern in the market about the level of inventories available to meet demand, and the possibility that propane could be in short supply. How could this be? As we have covered many times in the RBN blogosphere, U.S. propane production is more than double domestic demand. So how could a shortage possibly happen? The answer is pretty simple: exports. The U.S. exports more of its propane production than it uses here at home. This year the domestic market needs more barrels, so all that needs to happen is for U.S. prices to increase enough to shut off exports, right? Wrong. Propane prices have been spiraling up all year, and August prices are higher than they’ve been since 2013. But exports are still running strong, and so far, inventories are not building fast enough. In today’s blog, we’ll look at the drivers behind this seeming market aberration and consider why the upcoming winter season looks like uncharted territory for propane marketers.