Demand in the Northeastern US during the week ended February 4 decreased by 3.6 Bcf/d from the prior week, with lower demand during and after the weekend as the weather warmed up. Overall, Northeast demand averaged 29.2 Bcf/d. Res/Comm demand led the downward turn, decreasing by 3 Bcf/d week on week, while Power demand fell by 0.6 Bcf/d and Industrial demand was flat week on week. Demand for natural gas in the region is predicted to decline by another 2.3 Bcf/d during this coming week as the weather continues to get warmer.

Featured Articles

- Analyst Insight

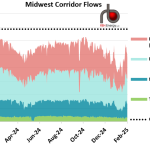

Northeast Gas Outflows Decline on Compressor Outage as Power Demand Up

Outflows of natural gas from the Northeast decreased last week as flows through TETCO are still down following a compressor outage.

- Blog

Turn the Page - Producer Restraint, Tighter Balances Disrupt Appalachian Gas Market Trends

Before the bullish winter of 2021-22, it appeared the Northeast natural gas market was headed for familiar territory: worsening seasonal takeaway constraints and deeper, constraint-driven price discounts starting as early as this spring. Instead, the market went in the other direction the past few months. Takeaway utilization out of Appalachia has been lower year-on-year and, for the most part, Appalachian supply basin prices have followed Henry Hub higher even as that benchmark rocketed to 14-year highs. That’s not to say that constraints out of the Northeast aren’t on the horizon. But the market is now poised to escape the worst of it this year, despite the completion of the last major takeaway pipeline project in the region, Mountain Valley Pipeline (MVP), being pushed out another year or longer, if it crosses the finish line at all. In today’s RBN blog, we provide an update on regional fundamentals and what recent trends mean for gas production growth and pricing in the region.

- Analyst Insight

Northeast Gas Demand Declines, But Unaffected by Short-Lived Export Tax

Demand for natural gas declined for the week ended March 11 compared to the prior week, with the short-lived Ontario export tax making little impact on power burn.