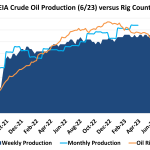

Crude oil production came in at 12.2 MMbbl/d for the second week in a row in the week ended June 23, according to the EIA's Weekly Petroleum Status Report, maintaining a near-flat growth trend over the past six months. However, the EIA's monthly U.S. crude oil production data (widely considered to be less timely, but more accurate, than the weeklies) has been trending upward in 2023. Production increased from 12.1 MMbbl/d in December 2022 up to 12.5 MMbbl/d in January 2023, then jumped again to 12.7 MMbbl/d in March. Given the flatness of the weekly production data, we expect monthly production data to begin to flatten as well.

Regarding the rig count, weekly U.S. oil rigs have been contsricting over the past six months, likely due to weaker commodity prices, higher costs, and a continued focus of E&P majors to divert cash to shareholders as opposed to aggressive drilling. Oil rigs peaked at 627 at the beginning of December 2022 and have fallen to 546, according to the most recent Baker Hughes report, marking an approximate 13% decline. The U.S. frac spread count (a measurement of how many crews across the U.S. are drilling wells in preparation for hydraulic fracturing, or "fracking," of shale) has also been declining. The number of frac crews peaked at 300 toward the end of November 2022, and has since fallen to 277, according to Primary Vision. This marks an approximate 8% decline.