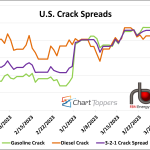

Toward the end of last week and into this week, the diesel crack spread has fallen sharply, more so than the gasoline crack or 3-2-1 crack spread. The margin refiners make producing diesel from a barrel of oil is tanking, falling from $40.41/bbl on March 28 to $34.17/bbl by Friday and $28.81/bbl as of Tuesday this week. This is due to several factors, including global prices for middle distillates such as gasoil and diesel falling due to the slowing economy, increased refinery output, and the replacement of fuel from Russia with volumes from the Middle East. Also, the warm winter in Europe and the Northeast U.S. means less demand for fuel oil used for heating homes. Finally, the Title Transfer Facility (TTF) in the Netherlands, the most liquid pricing location for natural gas in Europe, has been much weaker than expected lately. This means that companies that might have burned diesel when gas prices were high have since switched back to gas, decreasing demand for diesel in Europe.

Featured Articles

Behind The Margins – Will Lower Gasoline Prices Threaten the Gulf Coast Refining Party?

Recent third quarter earnings reports from US refiners have reflected lower refining margins squeezed by higher feedstock prices for inland crudes like West Texas Intermediate (WTI) rising to the same level as coastal crudes like Light Louisiana Sweet (LLS) while product prices stood still. In the past two weeks domestic crude prices have fallen below $100/Bbl in the face of a Gulf Coast supply glut. But despite lower crude costs, refinery margins have continued to weaken. The primary culprit has been sharply falling gasoline prices. Today we review what Gulf Coast refiners could do to improve margins.

Cracking Up, Part 2 - Will High Crack Spreads Be Enough to Balance Refined Products Markets?

U.S. diesel inventories are at their lowest level for May since 2000 and East Coast stocks recently hit their lowest mark for any week or month since the EIA started tracking them in 1990. Crack spreads for diesel — and, more recently, for gasoline — have gone parabolic, giving refiners the strongest financial signal ever to produce more diesel and gasoline as we enter the summer travel season. More jet fuel too. The problem is, U.S. refineries already are running flat-out. And Europe? It’s facing big cuts in crude oil and refined-products imports from Russia as well as much higher prices for — and possible shortages of — oil and natural gas, the latter being the primary fuel for operating refinery hydrocrackers, which upgrade low-quality heavy gas-oils into high-quality diesel, gasoline and jet. It’s a mess, and not easily fixable, as we discuss in today’s RBN blog.

It's a Small World After All - Global Implications of the U.S. Petroleum Products Glut

West Texas Intermediate (WTI) crude oil at Cushing is languishing back in the low $40s/bbl after a brief period of exuberance in the late spring. The blame for this latest oil-price retreat has shifted from high inventories of crude oil –– both on land and on tankers floating offshore –– to bloated petroleum-product inventories. There is some debate about how concerned the market should be about the increase in product stocks. In the opening episode of this blog series, we take a look at petroleum product cargo flows, and what they are telling us about the health of the market. We start today with middle distillates –– diesel and jet fuel.