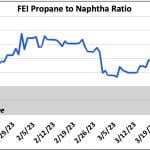

Asian propane prices have weakened relative to naphtha since the end of winter. The closely watched Asian FEI propane to naphtha spread has gone from near parity in mid-March to deep discount of -$96/mt as of April 16. The typical rule of thumb is that Asian steam cracker operators are likely to switch to LPG feedstock whenever the propane discount to naphtha is over -$50/mt or the propane-naphtha ratio is below 90% (at least for the flexible steam crackers that can crack LPG and naphtha). The chart below shows the ratio of the Asian FEI propane price to naphtha in the same region. In mid-April, the ratio hit a low of 85%, the weakest level since July 2020, which implies that Asia crackers will tend to favor propane feed over naphtha.

Featured Articles

- Blog

Jumpin' Jack Flash, It's a Gas: Propane - Propane Markets Writhe Due to Supply/Demand Uncertainty

So far in April, there was an unexpected run-up in propane prices early in the month, followed by a 21% swoon in the past 15 days of trading. The forward curve suggests smooth sailing from now through next winter season, but that seems unlikely, given recent market developments. Propane inventories, which are supposed to be building this time of year, actually fell last week, putting stocks at 16.9 MMbbl below this point in 2020, according to EIA statistics released last week. The data also showed that weekly exports spiked to the second-highest peak of all time at 1.7 MMb/d, while production declined two out of the past three weeks. And just over the horizon, there’s the potential for a big increase in Chinese propane demand as new petrochemical plant capacity comes online over the next three years. Today, we look at how these issues are likely to shape the propane market over the next few months and suggest that you consider attending our upcoming virtual conference, where we will pose these questions to industry leaders from production, midstream, exports, and retail market segments.

- Blog

You're the One That I Want - RBN's Steam Cracker Feedstock Model And Its Uses

Every day, about 1.8 million barrels of NGLs, naphtha and other ethylene plant feedstocks are “cracked” to make both ethylene and an array of petrochemical byproducts. And every day, decisions are made for each steam cracker on which feedstock—or mix of them—would provide the plant’s owner with the highest margins. Within each petchem company, these decisions are optimized by staffs of analysts and technicians using sophisticated and complex mathematical models that consider every nuance of a specific ethylene plants’ physical capabilities. Fortunately for us mere mortals, it is possible to approximate these complex feedstock selection calculations for a “typical” flexible cracker using a relatively simple spreadsheet model. Today we continue our series on how the raw materials for ethylene plants are picked with an overview of RBN’s feedstock selection model, a review of feedstock margin trends, and an explanation of how the model also can be used to indicate future NGL and naphtha prices and to assess the prospects for various industry players.

- Blog

What’s Crackin’ Dude? Ethane Hits Record High Steam Cracker Margin

On September 19, 2014, the operating margin for a representative Gulf Coast steam cracker running ethane hit a record high – an astonishing 70.4 cents per pound. Steam cracker margins depend not only on the spread between feedstock costs and the market price of ethylene but also on the varying amounts of propylene, butadiene and other byproducts that result from using different feedstocks. Understanding steam cracker profitability in the context of recent market developments is critically important, and it is the subject of RBN’s latest Drill-Down Report. In today’s blog we provide highlights of the report, which examines what is behind the ongoing shift from heavier to lighter NGL feedstocks, unveils RBN’s downloadable Steam Cracker Feedstock Selection Model, and discusses how new U.S. cracker capacity, NGL exports and other factors will impact these markets.