There’s been a lot of talk--and angst—this summer and early fall about the flood of crude oil headed to the Houston area from the Eagle Ford, the Permian Basin and other burgeoning oil-production regions. The angst seems worst for crude producers, who rightly wonder whether Houston’s looming shortfall of storage capacity will further disrupt crude oil logistics, contribute to more downward pressure on crude prices, or worse. Understanding what’s ahead requires an in-depth look at the changing crude flows into Houston and that is precisely the subject of RBN Energy’s latest drill-down report. In today’s blog, we provide highlights of the report, which is available for download by RBN Backstage Pass holders, and discuss how the shift from waterborne to pipeline delivery of crude already is affecting the market.

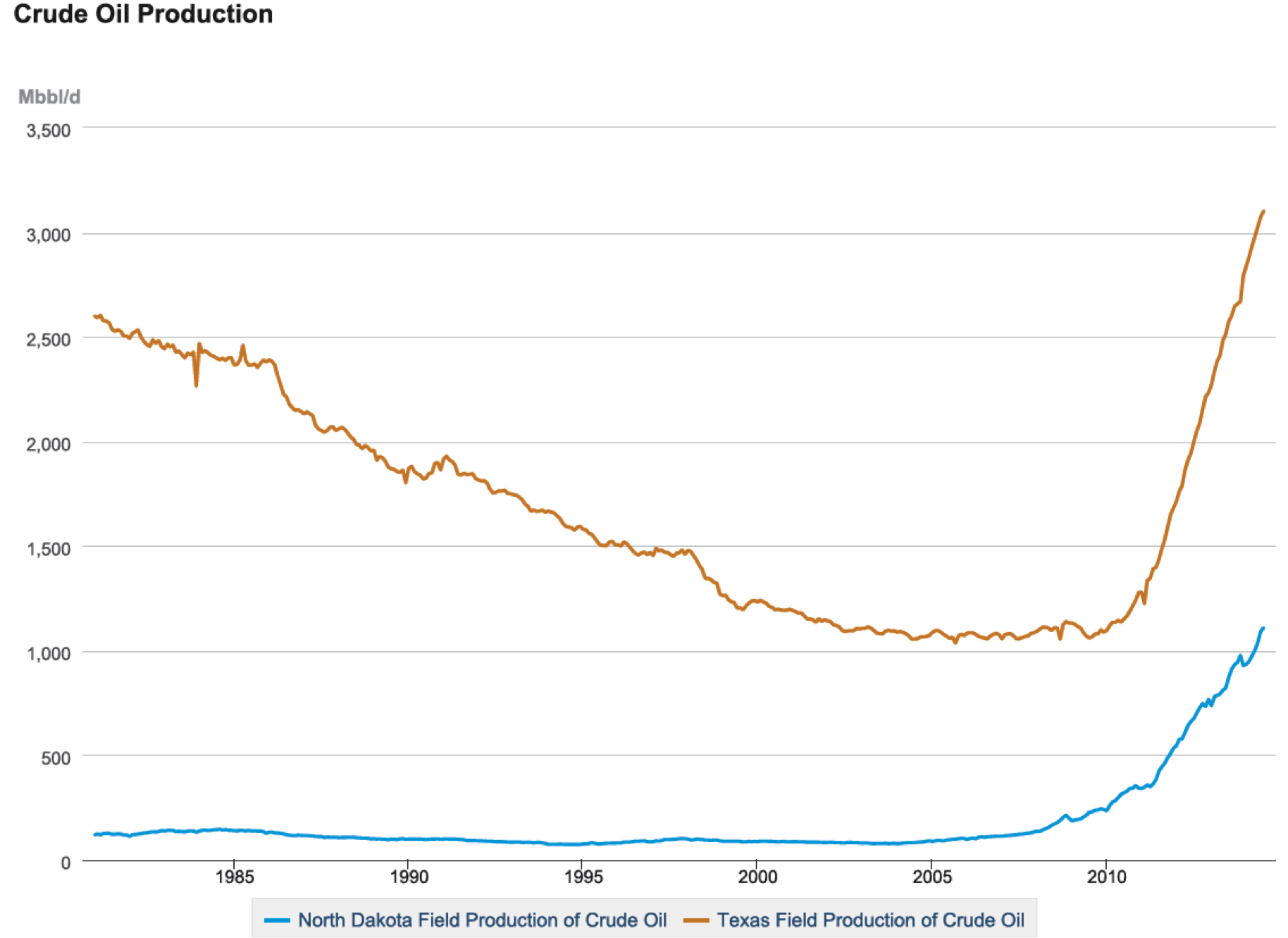

Those of us old enough to remember Apollo 13, OPEC oil embargoes, and the glitter rock of David Bowie and Iggy Pop have witnessed a lot of ups and downs in space travel, the energy business and rock-star fashion. But few, if any, changes have been more amazing to watch (and blog about) than the skyrocketing growth in crude output in the big US shale plays—the Eagle Ford, the Permian and the Bakken chief among them. While the word “transformational” may be a tad overused, how else can you describe the market effect of oil production in Texas rising 155% (to 3.1 MMb/d) over the past 48 months (according to the US Energy Information Administration, or EIA), and crude output in North Dakota jumping 223% (to 1.1 MMb/d) over the same period? (See Figure #1.) All that crude—and crude from the Niobara and Anadarko, and even the Canadian oil sands—is reducing the need for waterborne imports, and spurring development of new pipelines to the Gulf Coast (and Houston in particular) as well as new storage capacity. And, because so much of the new production is light sweet crude (or, in the case of some production like Eagle Ford, very light or super-light condensate), Gulf Coast refineries designed and built to process heavy crude are scrambling to adjust, either by investing in new infrastructure to handle light crudes or (more often--at least for now) resorting to extensive blending of very light crude with heavier crudes. (Blending requires storage capacity too.)

Figure #1;

Source: US Energy Information Administration (Click to Enlarge)

As we discussed in our recent blog, “Crude Falls to Pieces—How Far Will It Tumble?”, oil prices have experienced a steep decline in recent months as production increased (not just in the US but, after earlier disruptions, in Libya and Iran) and global demand stalled. U.S. oil prices potentially falling below $80/Bbl are bad enough (as far as producers are concerned). Worse yet are expected West Texas Intermediate (WTI) discounts in the futures market forward curve of $10/Bbl to the international benchmark Brent from late 2015 to the end of 2018. Those discounts (three times the November 2014 discount of less than $3/Bbl) are tied primarily to two factors: (1) rising production of domestic crude and (2) expectations of a continued ban on US crude exports (to anywhere other than Canada, that is). Domestic crude price stability is not helped by concern that the growing flood of crude headed to the Gulf Coast will be hampered from reaching refineries by inadequate crude storage and distribution infrastructure. Producers do not have much short-term control over crude flow--they need storage to even out the rate supplies flow to market. If refiners curtail buying, for example because of planned or unplanned maintenance, producers have to deal with the surplus, and storage is the primary vehicle to do that. Even the possibility of exporting crude--a frequently discussed solution to the oversupply of US crude--increases the need for operational storage in and around Houston.