It’s been quite a year already — and we’re just halfway through it! We began 2026 with energy markets looking very well supplied, with commodity prices generally expected to soften in the short term. But things quickly changed, first as a result of U.S. intervention in Venezuela, then much more dramatically with the Iran war and the closure of the Strait of Hormuz, followed in recent weeks by an uncertain cease-fire. Prices have surged at times this year for crude oil, natural gas, NGLs, refined products and petrochemicals, along with the multitude of consumer products that utilize those feedstocks. Fortunes were made (and lost) as a result. To survive such swings, you need a deep understanding of the fundamental forces impacting markets so that you can anticipate, identify and act on their secondary and tertiary effects. That’s the subject of today’s RBN blog and the focus of our upcoming School of Energy: Foundations, set for September 9-10 in Houston. Fair warning, today’s blog serves as an unabashed advertorial for the conference.

In observance of Independence Day, we are giving our analysts a break and revisiting a recent blog about the importance of market fundamentals and our upcoming conference. If you didn’t read it then, this is your opportunity to see what you missed. Happy 250th, America!

The swings in the global energy market have been significant so far in 2026, with the U.S. at the center of it all. There is no shortage of information and analysis out there, some of it seemingly contradictory. So, how do you know what data is important, which indicators to watch, and how to apply it all? Learning how to identify and analyze that information is what School of Energy is all about. To see how those pieces can come together, let’s look at some recent examples.

If you want to analyze the energy market’s volatility this year, there’s no better place to start than crude oil. By some estimates, up to 1 billion barrels of supply were shut-in due to the Middle East conflict and U.S. crude exports surged to unprecedented levels. Is the sharp rise in exports likely to be around for the long term, or is it a short-term phenomenon? It’s a complicated question, but to know the answer, you first need to know the fundamentals of U.S. crude oil supply and demand.

The supply of U.S. crude has been a growing focus of industry insiders and politicians alike as benchmark prices rose sharply in the near term as the Middle East conflict raged but remained lower in future months, a phenomenon called backwardation. To forecast how producers might respond in that scenario (or the opposite, contango), School of Energy will take students through the economics of production, how crude oil drilling impacts other commodities, and even equip you with an Excel-based production model along with instructions on how to use it. We’ll have two experts in the field at the conference: Brandon Myers, Head of Research at Novi Labs, will give us their latest evaluation of major U.S. supply basins; and Taylor Noland, Senior Crude Markets Consultant for Novi Labs, will discuss the prolific Permian Basin, from history and the major producing corridors to current-day pipeline flows and output.

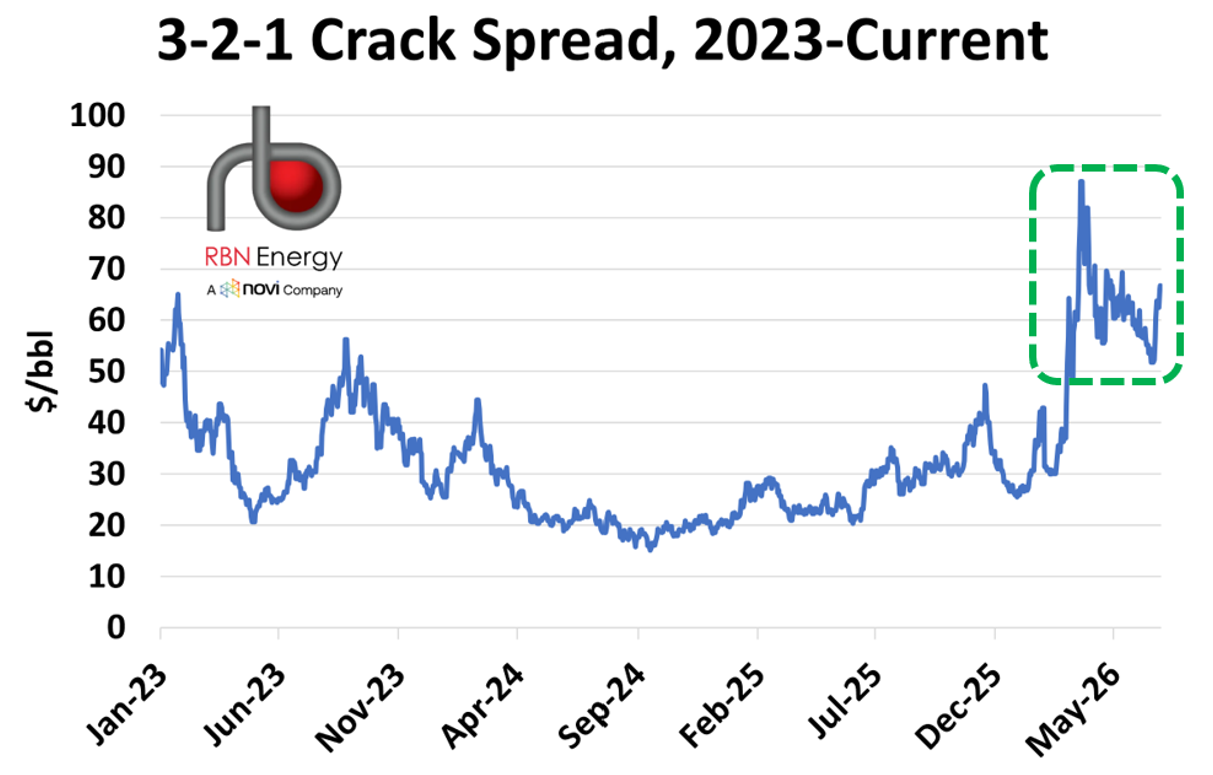

The demand side of the U.S. crude balance comprises two parts: refinery runs and crude exports. Robert Auers, Managing Director of Refined Fuels at Novi Labs, will lead the discussion around the U.S. refining sector, covering everything from the basics to more detailed analysis using crack spreads and refinery yields. As shown in Figure 1 below, the 3-2-1 crack spread, a widely used benchmark for estimating oil refinery profitability, has been consistently above $50/bbl since March (see dashed green box), well above the prior three years. For crude exports, Novi Labs President of Consulting Rusty Braziel will explain the factors that drive the U.S. market, including the top destinations for U.S. crude.

Figure 1. 3-2-1 Crack Spread, 2023-Current. Source: Chart Toppers

About the song

“Nobody Told Me” was written by John Lennon and appears as the fifth song on side one of John Lennon and Yoko Ono’s sixth and final studio collaboration album, Milk and Honey. Lennon originally wrote the song for Ringo Starr, but after Lennon’s murder in December 1980 it was held for inclusion on the posthumous Milk and Honey LP. The up-tempo song describes a world full of contradictions. With its refrain of “Nobody told me there would be days like these, strange days indeed,” Lennon contemplates that life is always going to contain mysteries. Released as a single in January 1984, it went to #5 on the Billboard Hot 100 Singles chart. Personnel on the record were: John Lennon (vocals, rhythm guitar), Earl Slick, Hugh McCracken (lead guitar), Tony Levin (bass), George Small (keyboards), Andy Newmark (drums) and Arthur Jenkins (percussion).

Milk and Honey was recorded between October and December 1980, with additional recording taking place between 1982 and 1983. It was the follow-up album to Lennon and Ono’s Double Fantasy LP. After Lennon’s murder, it took Ono three years to complete the album. Most of the Ono material on the album was new recordings made after Lennon’s death. The album has John Lennon and Yoko Ono listed as producers, even though Jack Douglas produced all the Lennon recordings. Douglas sued Ono and received an undetermined share of the revenues from the album. Released in January 1984, the album went to #11 on the Billboard 200 Albums chart and has been certified Gold by the Recording Industry Association of America. Three singles were released from the LP.

John Lennon was an English singer, songwriter and musician from Liverpool. He is known as a founder and member of The Beatles, a band that changed the course of popular music and culture worldwide. As a solo artist, he released 11 studio albums, three live albums, 15 compilation albums and 23 singles. He has an MBE and is a member of the Rock and Roll Hall of Fame twice, as a solo artist and as a member of The Beatles. He is a member of the Songwriters Hall of Fame and has a star on the Hollywood Walk of Fame. Lennon was murdered outside his apartment in New York City in December 1980 at 40.

Yoko Ono is a Japanese artist, musician and filmmaker. She married John Lennon in March 1969. As a solo artist, she has released 14 studio albums and 40 singles. She is the author of 14 books and has directed or appeared in 22 films. At 93, Ono and her son, Sean Ono Lennon, are the executors of John Lennon’s estate.

"About the Song" -- written by Mickey McMahan , RBN Director of Musicology