Anyone stepping out of a time machine might conclude that the world has become a giant game of chance, with sports betting ads flooding the airwaves and prediction markets offering wagers on everything from the duration of world leader handshakes to pop culture trivia. Given that the Iran war-driven surge in oil prices doubled E&P profits in Q1 2026, it would seem that the closest thing to a “sure thing” in this marketplace would be a surge in capex to capture fatter cash flows as the political standoff sustains higher realizations. But that would have been a losing bet, as industry 2026 capex remained virtually unchanged. In today’s RBN blog, we review oil and gas producers’ current investment and production guidance while analyzing potential future strategy as the economic impacts of the Iran war evolve.

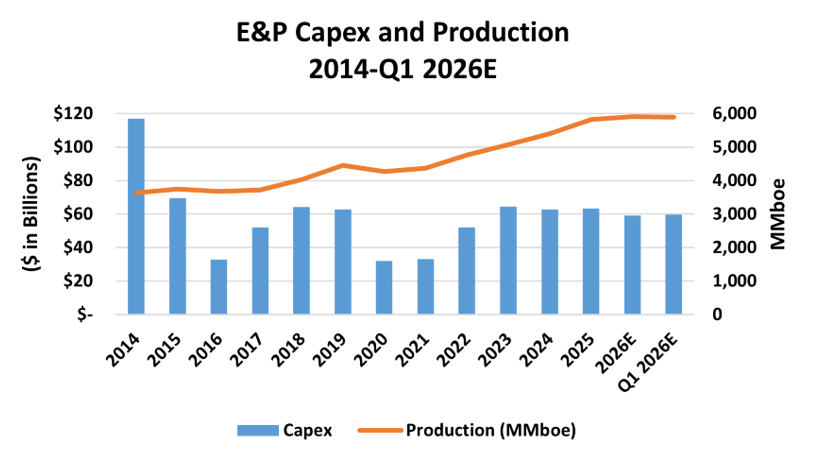

As shown in Figure 1 below, E&P capital spending (blue bars and left axis) has been trending lower since the post-pandemic peak in 2023. After slashing investment in 2020 and 2021 as the onset of the pandemic threatened the financial stability of a chronically overspending E&P industry, producers rode a wave of sustained high commodity prices in 2022 and 2023 to increase drilling to offset steep shale decline rates. Inflation as well as increased acquisition-related activity helped spur a 58% increase in 2022 and a 24% rise to $64.5 billion in 2023, which resulted in a 14% production gain.

(What can your acreage position tell you about your assets? To learn how the Novi Insights platform can be used to examine operator activity, production performance and infrastructure access, sign up for a free webinar and Q&A session from 2-2:30 pm (Central) on Thursday, June 11, led by Hollee Baird, Novi’s Data & Analytics Technical Advisor. Click here to learn more and to register.)

Figure 1. E&P Capex and Production, 2014-Q1 2026E.

Source: Oil & Gas Financial Analytics LLC

U.S. Propane Inventories Build While Exports Fall

U.S. propane inventories continued to build in late May, rising 2.1 MMbbl to 83.3 MMbbl and remaining well above historical levels. Meanwhile, propane exports fell sharply from the prior week to 1.65 MMb/d, though volumes remained higher than the same week last year.

About the song

“The Gambler” was written by Don Schlitz and appears as the first song on Kenny Rogers’ sixth studio album of the same name. Schlitz wrote the song in 1976 while working as a night shift computer operator in Nashville. The song uses a poker game as a metaphor for overcoming life’s challenges. Its catchy chorus — “You got to know when to hold ’em, and know when to fold ’em” — helped propel the song to become an international hit. It was first recorded by Bobby Bare in 1978 and appeared on his Bare album, but was never released as a single. Kenny Rogers released it as a single in November 1978 and it went to #1 on the Billboard Hot Country and #16 on the Billboard Hot 100 Singles charts. Many artists have covered the song over the years. Rogers won a Grammy Award for Best Male Country Vocal Performance for the song in 1980. Personnel on the record were: Kenny Rogers (lead vocals), The Jordanaires, Dottie West (backing vocals), Ray Edenton, Jimmy Capps (acoustic guitar), Billy Sandford (electric guitar), Pete Drake (steel guitar), Pig Robbins (piano), Bob Moore (acoustic bass), Tommy Allsup (tic-tac bass), and Jerry Carringan (drums, shakers).

The album, The Gambler, was recorded at Jack Clement Recording in Nashville in the summer of 1978. Produced by Larry Butler, it was released in November 1978 and went to #1 on the Billboard Top Country, and #12 on the Billboard 200 Albums charts. It has been certified 5X Platinum by the Recording Industry Association of America. Two singles were released from the LP. A television movie, Kenny Rogers as the Gambler, was released in 1980. It was directed by Dick Lowry and starred Kenny Rogers as Brady Hawkes, the gambler.

Kenny Rogers was an American singer, songwriter, musician and actor. He began his professional career as a musician in Houston, playing rock and roll in the club circuit in the late 1950s before joining the New Christy Minstrels as a singing bassist in 1966. He left them to form The First Edition, which had their first hit record in 1968 with the psychedelic “Just Dropped In to See What Condition My Condition Was In.” Rogers charted more than 120 songs in different genres and sold more than 100 million records worldwide. As a solo artist, he released 39 studio albums, 43 compilation albums and 80 singles. He was featured in four motion pictures and made numerous television appearances. He won a Grammy Award, an ACM Honor Award, an ASCAP Golden Note Award, several ACM and CMA Awards, has a star on the Hollywood Walk of Fame, and is a member of the Country Music Hall of Fame. He played his last concert in Nashville in October 2017 and died in Sandy Springs, GA, in March 2020 at 81.

"About the Song" -- written by Mickey McMahan , RBN Director of Musicology