Over the past two weeks, crude oil prices at Clearbrook and Guernsey have, for the second time this year, closed the gap between the Bakken and West Texas Intermediate (WTI) prices. Bakken prices are up and there is a simple explanation why. New rail terminals - both in the Bakken and at refining centers on the East and Gulf Coasts. In today’s blog we explain why Bakken prices are rising and what the implications are for rail shippers out of the region.

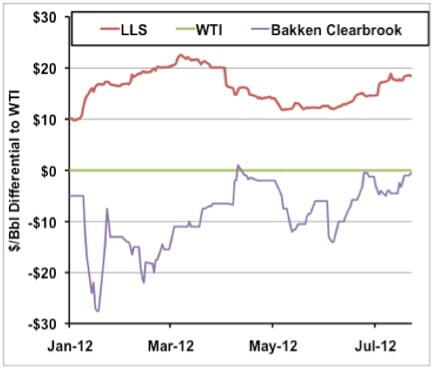

The chart below shows the Bakken discount to WTI (magenta line), WTI (green line at zero) and the Light Louisiana Sweet (LLS) premium over WTI (red line). To understand the chart we need to make two big points clear so lets go ahead and make those points first while you look at the chart. We will explain each point in detail in a minute. The first big point is that the Bakken discount to WTI is narrowing and has crossed into positive territory a couple of times since May – right now the discount is $0.50/Bbl. The second big point is that the LLS premium to WTI (red line) has widened over the same time period since the Bakken Discount to WTI started to narrow.

Now lets talk through the first big point. The Bakken discount to WTI is narrowing. Generally speaking if producers sell their crude in North Dakota, the price they receive is related to WTI. We explained how this works in Part I of “The Bakken Buck Starts Here”. Bakken prices at the Clearbrook and Guernsey hubs traded at hefty discounts to WTI for much of the first quarter of this year (and a large part of last year) because of pipeline capacity constraints out of the Bakken and a logjam at Cushing OK that is preventing rising Canadian and Bakken crude production from reaching Gulf Coast refineries. That meant the Midwest refinery market was oversupplied and Bakken barrels were discounted against WTI. The good news for Bakken producers selling crude in North Dakota is that as the chart shows, the Bakken discount to WTI is disappearing. Why is this happening? The answer is new rail terminals – both in North Dakota and at refining centers outside the Midwest.

First the Bakken terminals - we reported previously on extensive plans for building new rail takeaway capacity (see “Bakken: If Railing Crude is Wrong I Don’t Wanna be Right” and “Rail it on Over to Albany – Moving Bakken East”). The chart below from the North Dakota Pipeline Authority tells us all we need to know on the topic. By the end of this year, rail capacity out of the