Yesterday the Intercontinental Exchange Brent premium to WTI NYMEX closed at $9.31/Bbl, its lowest value since January 2012. Spread watchers have long anticipated this narrowing but it throws a spanner in the economics of crude by rail shipments from North Dakota. Today we suggest that the Brent/WTI spread may have narrowed before crude supply fundamentals justify the move and that it could widen again quickly to $15 or higher.

This is the latest episode in our ongoing series tracking the two crudes that arguably most influence US prices – North Sea benchmark Brent and US Benchmark West Texas Intermediate (WTI). If you are new to the Brent/WTI spread saga you can refer back to the first three paragraphs of the previous episode in this series for an introduction (see Are They Never Ever Getting Back Together Again). You can also follow the Brent/WTI spread daily via RBN’s Spotcheck - click here if you have trouble accessing.

The Spread Narrows

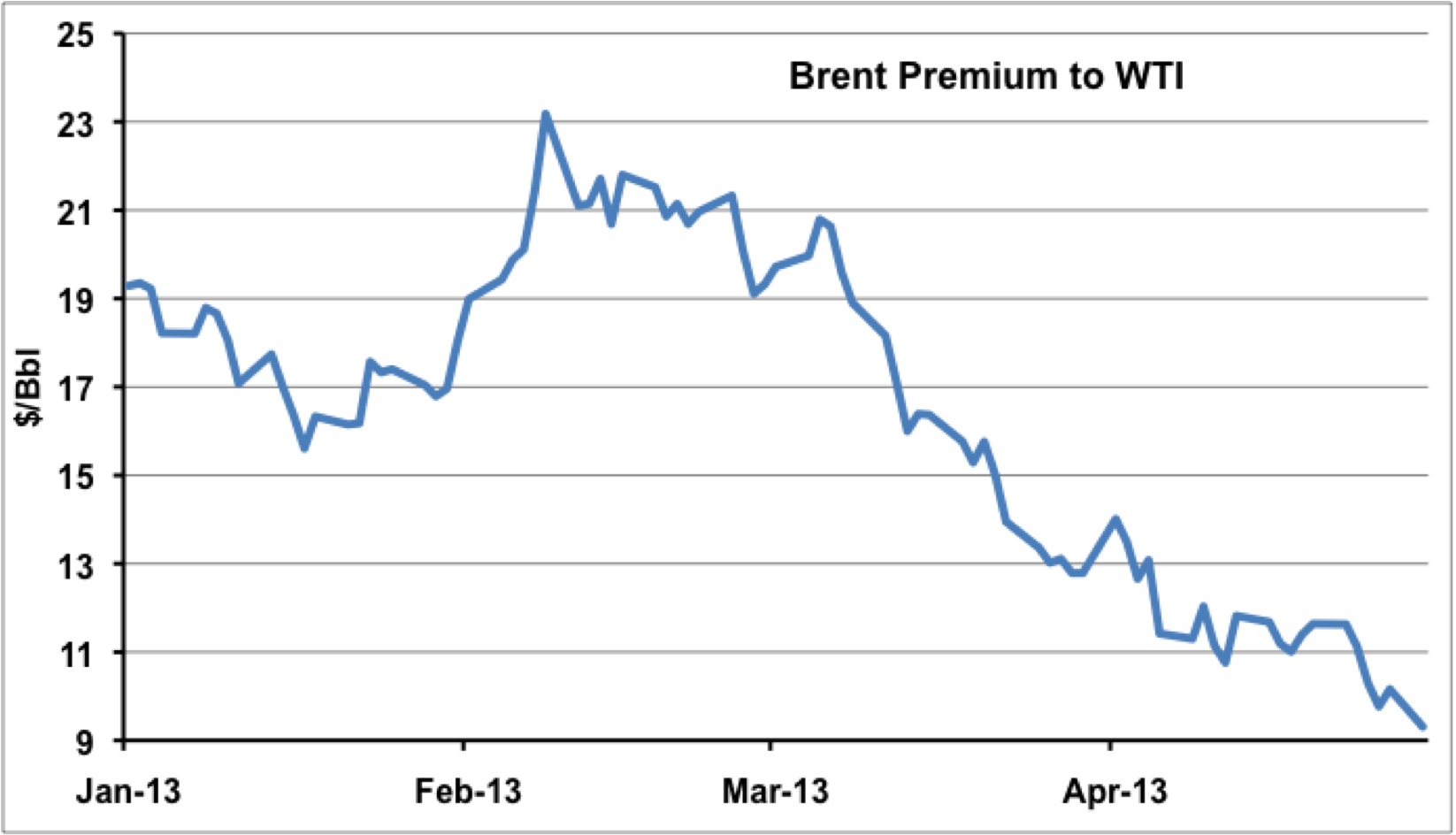

The chart below shows the spread between Brent nearby futures prices on the Intercontinental Exchange (ICE) and WTI nearby futures prices on the CME NYMEX Exchange from the start of this year until yesterday (April 29, 2013). In our previous analysis of the Brent/WTI relationship in March (see Are They Never Ever Getting Back Together Again) we observed some narrowing of the Brent premium to WTI bringing the spread to just under $14/Bbl on March 22, 2013 down from $23.18/Bbl on February 8. That narrowing momentum has continued and last Thursday the spread closed under $10/Bbl for the first time since January 2012.

Source: CME data from Morningstar

Yesterday (April 29, 2013) the Brent premium to WTI fell again to $9.31/Bbl on stronger US economic data. Brent prices have fallen relative to WTI since the start of April primarily because US East Coast gasoline prices fell on tepid demand. European refineries traditionally expect to sell a lot of gasoline into the East Coast market during the summer. That is because East Coast refineries do not have the capacity to meet local gasoline demand (see Don’t Let The Sun Go Down On Me). With lower gasoline prices on the US East Coast European refiners don’t make money from exports so they cut back refinery crude runs. That means they purchase less crude which puts downward pressure on Brent prices. Last week East Coast gasoline stocks increased over the previous week according to Energy Information Administration (EIA) data indicating continued weak demand for gasoline imports from Europe and putting further downward pressure on Brent prices. Meanwhile WTI prices have been relatively strong over this period based on better economic news in the US and an expected increase in the ability to move crude out of Cushing by pipeline thereby easing the Cushing stockpile.

Relief For the Cushing Stockpile?

A number of nearly completed and committed pipeline projects are underway that will provide over 1 MMb/d of new crude oil capacity to relieve the Cushing stockpile by early 2014. The Magellan Longhorn reversal should begin operation in Mid April (that would be last week) according to Magellan Midstream Partners statements in March. Magellan said the pipeline would commence with an initial capacity of 70 Mb/d ramping up to 225 Mb/d by 3Q 2013. Longhorn runs from Crane in the Permian Basin of West Texas to Magellan’s East Houston Crude Terminal (see The New Adventures of Good Ol Boy Permian). Expansions to the Sunoco Logistics Partners West Texas Gulf pipeline are expected to be online during the second quarter of this year and will add another 80 Mb/d of crude capacity from the Permian Basin to Houston and Nederland (Port Arthur). Sunoco’s Permian Express Phase 1 project will add another 90 Mb/d of capacity between Wichita Falls, TX and Nederland also in the second quarter this year, expanding to 150 Mb/d by early 2014.

However, although the new pipelines coming into operation from the Permian reduce pressure on supplies from that Basin into Cushing overall crude stocks at Cushing remain stubbornly high. Last week the EIA reported that Cushing stocks were up slightly over the prior week at 51.2 MMBbl and still just 2 percent below their all-time high in January 2013. We believe that the Cushing Stockpile will continue to exert downward pressure on WTI prices at Cushing at least until the beginning of 2014 after the TransCanada Keystone Gulf Coast Pipeline opens between Cushing and Houston providing 700 Mb/d of incremental capacity (expected late 2013) and the Seaway pipeline from Cushing to Houston doubles capacity to 800 Mb/d (expected 1Q 2014).

Impact on Crude by Rail Economics From the Bakken

Meanwhile if the recent narrowing of the Brent premium over WTI persists there will be a significant side effect on the economics of moving crude to market by rail from the Bakken. RBN Energy has closely tracked the rapid development of crude by rail operations during 2012. These began because pipeline capacity out of the Midwest could not handle growing crude production from basins like the North Dakota Bakken (see the Crude Loves Rock’n’Rail series). Using rail became viable when Midwest crude oversupply led to price discounts to Bakken crude at Cushing, OK that justified the higher cost of moving crude directly to coastal markets by rail. As we have discussed previously 18 new crude rail loading terminals have become active in North Dakota – 13 of them built to handle 100 tank car plus unit trains (see A Plethora of Rail Terminals in the Williston Basin). According to North Dakota Pipeline Authority data for February 2013 these terminals were shipping 68 percent of the crude oil leaving North Dakota (about 475 Mb/d after local refinery consumption). Industry data suggests that these shipments are largely headed for Gulf Coast destinations such as St. James, LA. There they can fetch higher prices based on the Light Louisiana Sweet (LLS) crude benchmark that tracks international prices set by Brent. Bakken crude is also being sent by rail to the East and West Coast markets where prices are set by Brent and Alaska North Slope (ANS) prices respectively. (In turn, ANS prices are also set by international competition using Brent as a benchmark.) If you rail the crude to the East or West Coast – you get a higher price.

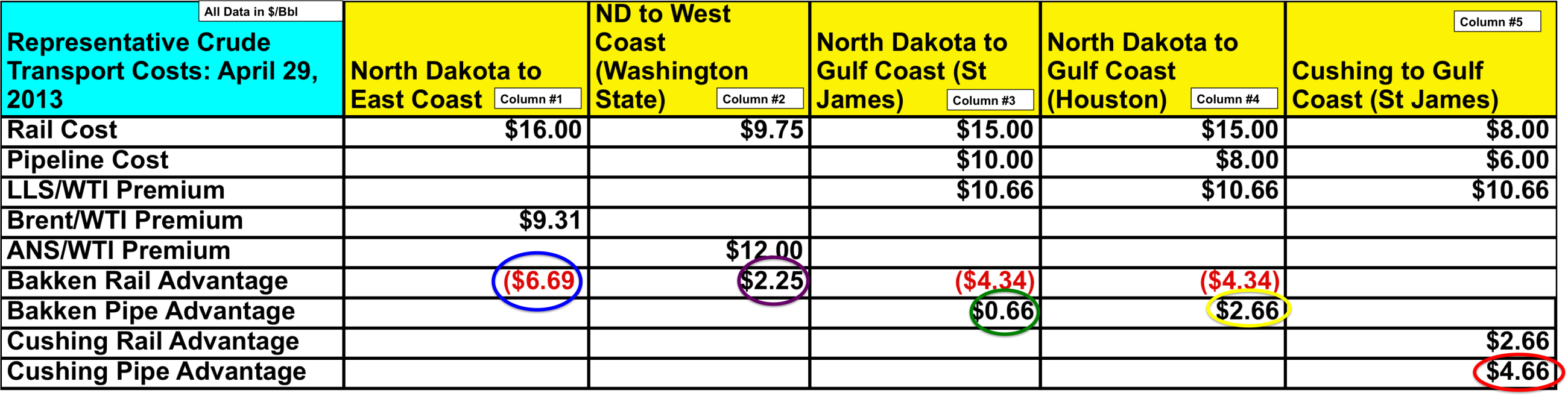

However with the Brent premium to WTI now falling below $10/Bbl we looked at the impact on the economics of rail transport from the Bakken to coastal destinations to see if they still make sense. The table below shows industry published costs for rail transport from North Dakota to East, West and Gulf Coast destinations and then compares those costs to yesterday’s crude price differentials. We also included estimated pipeline costs and at the bottom of the table, the estimated cost of moving crude by rail or by pipeline from Cushing, OK to the Gulf Coast.

Source: RBN Energy, Company Presentations

The purpose of the table is to compare recent premiums over WTI Cushing at coastal destinations with the transport costs by rail from North Dakota. Bakken crude in North Dakota has recently been priced at a slight premium to WTI (~$1/Bbl) at Guernsey, WY and a slight discount (~$1/Bbl ) at Clearbrook, MN. If the premiums to WTI at coastal destinations are higher than rail transport costs then Bakken producers realize a higher price for their crude. If the rail costs exceed the price premiums then Bakken producers will have to discount their prices to compete with benchmark crudes at coastal destinations. The table uses yesterday’s (April 29, 2013) price premium over WTI Cushing for Brent on the East Coast ($9.31/Bbl), ANS on the West Coast ($12/Bbl), and LLS at the Gulf Coast ($10.66/Bbl). Shipping costs used are based on company published estimates and pipeline tariffs. All values are in $/Bbl.

Each column in the table represents a transport destination option so by walking through them one at a time we can see how narrowing coastal premiums to WTI are impacting the economics of shipping crude by rail. Column #1 represents Bakken crude shipments to the East Coast. There are no pipeline alternatives to rail for this market, so the economics of shipping Bakken crude rely on the Brent premium to WTI being greater than the cost of rail transport – estimated at $16/Bbl. But the Brent premium is now only $9.31/Bbl so refiners would only pay Bakken producers WTI + $9.31/Bbl for their crude. That means Bakken producers have to swallow a $6.69/Bbl discount to compete against Brent on the East Coast (blue circle on the table). If Bakken producers don’t discount their prices to match Brent then East Coast refiners will simply import Brent or other crudes priced according to Brent.

Column #2 represents Bakken crude shipments to the West Coast (Washington State). Estimated rail transport cost is $9.75/Bbl versus a $12/Bbl premium for ANS crude on the West Coast. That means Bakken crude should attract a $2.25/Bbl premium over WTI in Washington State (purple circle). In other words it is still economic for Bakken producers to ship to the West Coast. Like the East Coast there are no pipeline transport alternatives to rail on the West Coast. If shipments by rail go further south to California (there are fewer destination terminals built there yet) the rail cost goes up by $3-$5/Bbl so Bakken producers would have to discount their prices to WTI in order to compete with ANS.

About the song

One Step Beyond was the Debut Album of the British “ska” group Madness released in 1979

Comments

I am a raw novice at crude pricing, so ...! But, it seems to me that your focus on the producers is backwards. I think the focus should be on the customers for crude (the refiners) and the price they must pay to obtain crude.

The availability of rail transport for crude reduces or eliminates Cushing as major driver of pricing in the US crude market. I think Cushing's future importance is only as one of several refining centers.

The Bakken producers will be the primary supplier to the Cushing refiners, but the rail option they have many other potential customers as well. So Bakken producers will look at the price each refiner market will pay and sell as much as they can at the best prices, net of transportation.

The question is what price will the Cushing refiners have to pay for crude -- which is the WTI price. I think this is now a dependent variable, not an independent variable as it was in the past.

With rail, the coastal refiners have a choice of Brent-priced (or ANS) crude or US-sourced crude, so they will drive prices for US crude. The Houston and St. James refiners will only pay Brent based prices, so the price the Cushing refiners pay should be the Gulf coast price less the transportation cost to those refiners. So, your numbers suggest WTI should be $6 (pipe) to $8 (rail) per barrel less than Brent, adjusted for quality differences.

Does this make sense?

Jim Beetem

.

In reply to Brent-WTI Spread by Jim Beetem

Thanks for the comment Jim,

Producers will seek out the best "netback" meaning market price less transport cost

It follows that they will (given a choice) always choose the lowest cost transport available to where prices are high

Like all US crudes, Bakken prices will continue to be set in relation to Cushing - not just because of its physical location in the Midwest but because it is the delivery point for the NYMEX futures contract. The futures market decides prices for WTI (see The Cost of Crude at Cushing) based on many factors. Using WTI as a benchmark provides transparency, liquidty and ease of price risk management. Brent performs a similar function in the western world outside the US. So long as the US imports crude at the coasts, Brent prices will influence crude at those locations as the "alternative" to domestic grades.

If Brent has a premium to WTI then producers will sell at the coast for a higher price if the netback is better

If the netback is better at Cushing then producers will send crude there

The spread between Brent and WTI is therefore a crucial determiant of the transport cost that a producer is motivated to spend getting crude to coastal markets

If the spread does not justify transport costs to the coast (eg by rail) then increased volumes going to inland destinations (eg Cushing) will exert downward pressure on prices there - and increase demand for Brent priced imports at the coast - widening the spread again until refiners acquire adequate supplies.

Sandy

In reply to Thanks for the comment Jim, by Sandy Fielden

Hi Sandy,

Do you have any idea how much the increased leasing rates on oil rail cars had added to the cost of shipping by rail? Seems to me that as the WTI/Brent spread weakens, leasing rates will have to go down.

Alex

The prices will most likely to trade close to par (taking into account the product price diffs), as rail operators will cut prices. As crude still promises volume growth.

Shouldn't the "Bakken Rail Advantage" also take into account the quality differentials and transportation costs for Brent based crudes when comparing to Bakken? You have considered transportation costs for Bakken but not for the Brent based crudes.

For example, on the East Coast a refiner may look at a grade like Qua Iboe (West African light crude) in comparison to Bakken (a light crude) and consider them "equal" in quality. Qua Iboe normally trades at a premium to Brent, and then it must be transported to the East Coast via tankers. So the delivered price of an "equivalent Brent' on the East Coast may be much closer to the delivered price of Bakken on the East Coast.

It will be interesting to watch where the Brent/WTI differentials go, and how that impacts the destination for Bakken via rail - I know that here on the East Coast there are a lot of new unloading facilities getting built and I wonder how those will change if the differential stays as narrow as it is right now.

Chris