The Dominion South Point strip price for the balance of 2015 (March-December) has been settling consistently under $1.90/MMBtu, while Transco Zone 6 in New York is averaging around $2.80/MMBtu in this week’s forwards market. Meanwhile, Northeast and US gas production remain near record levels. The breakeven price environment and looming oversupply leaves producers and the industry vulnerable to the downside. Where and when will prices bottom out? What, if anything, would trigger a rebound? Today Part 4 of our Forward Curve Series, focuses on fundamental factors driving Northeast forward curves over the next few years.

In Part 1 of this series we looked at the factors that influence natural gas forward curve prices in the US market, the big five being: supply, demand, storage, transportation/infrastructure and weather. In Part 2 and Part 3, we dove into the Northeast gas market, examined the region’s transformation to become a net producer and reviewed the dramatic reshaping of its forward curves. The trigger for this transformation is local production growth from the Marcellus/Utica shales, which tipped the Northeast supply/demand balance in less than a decade from perpetually supply-short to largely self-sufficient and on the brink of oversupply. In the new gas world, Northeast forward curves have shifted from what were historically premium prices (above Henry Hub) to major discounts ($1.00/MMBtu or more below Henry Hub). Given where Henry Hub is trading these days ($2.00/MMBtu and $3.00/MMBtu handles through at least 2021), that means outright prices in the Northeast are skirting breakeven levels for producers for the next few years. There is no obvious reverse on this bullet train. But where are the curves headed? This time, we look at fundamental factors at play.

Northeast production is not done growing

Production ended 2014 and started 2015 well above the 2014 average. This means that even if Northeast production were to remain flat to current levels around 19 Bcf/d for the remainder of 2015, gas production would still average nearly 3.0 Bcf/d higher year over year. Looking at it another way, gas production would have to decline by about 3.0 Bcf/d from current levels to be flat with the 2014 average, which is unlikely in the near term. Our friend Kyle Cooper recently estimated 60 Marcellus rigs would be required to maintain current production levels. The latest rig count for the Marcellus is 75 rigs, per Baker Hughes. Existing hedges, lower drilling service costs (in response to lower demand at current price levels) and shifting resources to high-yield areas (“sweet spots”) are other factors that could help producers maintain or grow volumes while lowering costs (see It Don’t Come Easy).

Eventually, existing hedges will run out, new attractively priced hedges will be hard to come by and the price slump is likely to catch up to producers. But in the near to mid-term, the sustained production levels mean the Northeast market is far from balanced and supply will continue to weigh heavy on the forward curve.

Northeast demand is not enough

On the other side of the equation, Northeast demand (from the power generation, residential/commercial and industrial sectors) is growing but much slower than production. As a result, it’s not likely to be a game-changer for the forward curve in 2015. The good news is that market conditions (lower gas prices) and the regulatory environment are favoring gas over coal in the power generation sector. Platts analytics group Bentek Energy notes that 2 GW of coal-fired power generation capacity was scheduled to come offline in the Northeast in December and another 7 GW is expected to retire in 2015, together the equivalent of about 0.5 Bcf/d of gas demand (assuming 7.5 heat rate and 30% utilization rate). The 620-megawatt Vermont Yankee nuclear power plant was also decommissioned this past December. These trends support the Northeast gas forward curve, but they are not nearly enough to offset the year-over-year production gains in the near-term.

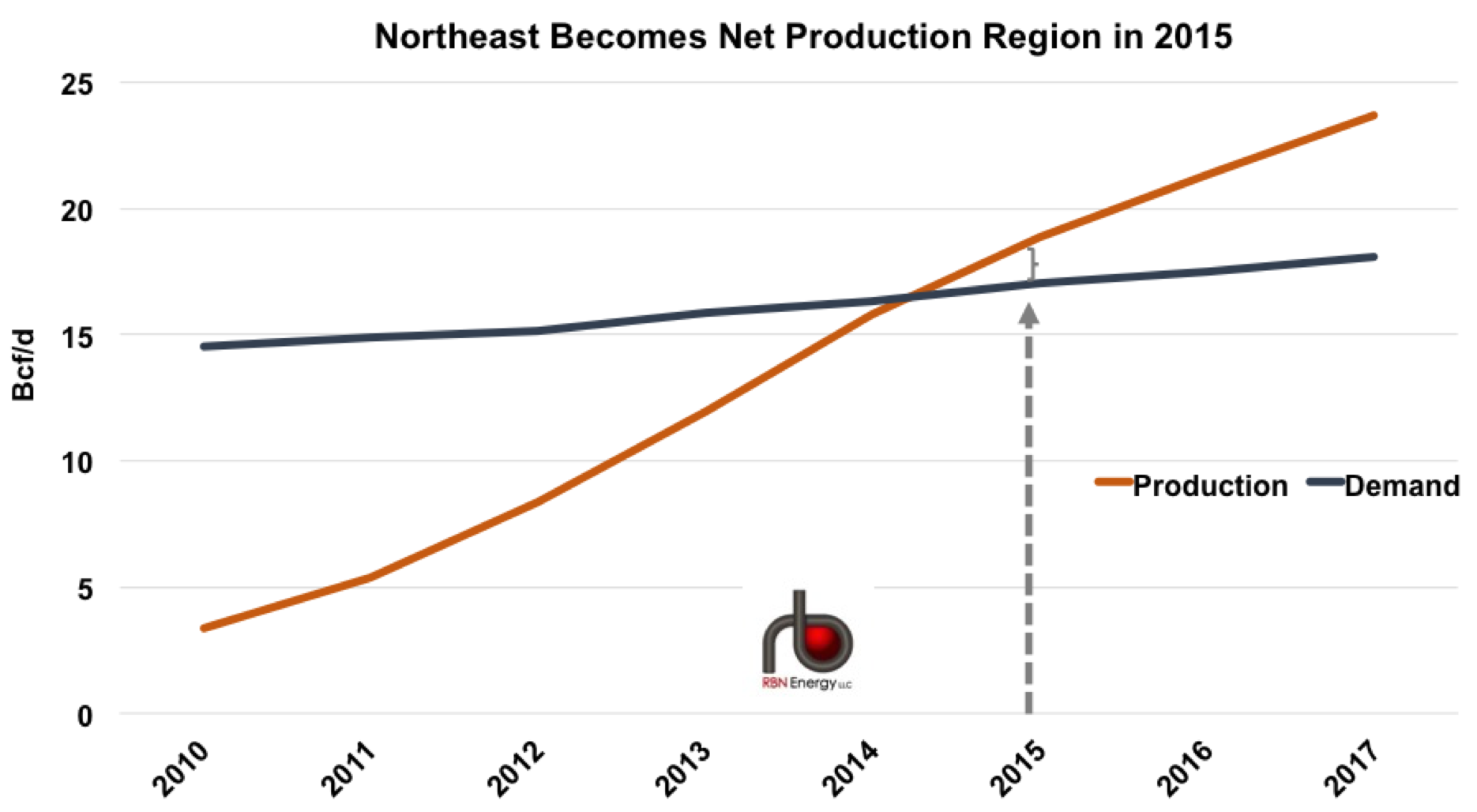

Weather, which influences both power and residential/commercial demand, is always the wild card. But what is evident already is that this winter has been much milder than last year’s record-setting, polar vortex-induced cold, adding to supply imbalance in the region. In fact, barring prolonged extreme weather events, we expect Northeast production to exceed demand on an annual average basis for the first time in 2015 (the region has already experienced this for parts of the year since 2013). Figure 1 below shows historical annual Northeast production (red line) versus Northeast demand (blue line), including our forecast over the next two years, assuming normal weather. Even assuming production stays flat to current levels and some demand growth from last year, there will be surplus supply in the region. That means excess gas supply will need to head to storage or be shipped out of the region.

Figure 1

About the song

"Living In Fast Forward" was released by Kenny Chesney in January 2006 and reached #1 on the Billboard Hot Country Songs chart. It was written by David Lee Murphy and Rivers Rutherford.