Throughout the three year-long disruption of the US crude oil distribution system caused by rising domestic and Canadian production trying to find a path through the Midwest, the Seaway pipeline reversal project has been a market bellwether of progress to unwind the congestion. In 2Q 2014 the final phase will come online - opening up an additional 450 Mb/d capacity between Cushing and Houston. As the Seaway project has been built out, the crude surplus in the Midwest appears to have moved to the Gulf Coast. Today we detail the impact of Seaway Phase 3 on Gulf Coast crude supplies.

The first episode in this series described 4 MMb/d of current and planned expansions to crude transportation capacity into the Texas Gulf Coast region (see Handling The Texas Gulf Coast Crude Flood). Our analysis showed that the new incoming light crude capacity will exceed Texas Gulf Coast demand by somewhere north of 0.5 MMb/d by the end of 2015. In episode two we described how some of these excess crude supplies would move east on the reversed Ho-Ho pipeline (see Gulf Coast Crude West to East Flows). In episode three we looked at how shippers could divert supplies away from Texas Gulf Coast congestion (see Texas Gulf Coast Bypass Options). Episode four looked at progress bringing TransCanada’s Keystone XL Gulf Coast extension (a.k.a, Cushing Marketlink Pipeline (CMP)) online (see Keystone Marketlink Comes to Texas). This time we look at the impact of the twin Seaway Pipeline from Cushing to Freeport that is expected online during the second quarter of 2014.

Member Updates on the Cushing Marketlink Pipeline

Before we get to Seaway, we want to mention a number of valuable RBN member comments received after our last episode (you can read these at the bottom of the blog page). One member offered insight into when the Cushing Marketlink Pipeline will come online – a topic that has received a lot of attention in the press since then. The last word from TransCanada is that the pipeline will commence flow in “mid-to-late January”. We shall see. Another member provided insight that the pipeline is designed to run with a full load of heavy crude – i.e. it will ship 700Mb/d of heavy crude – contradicting what we had learned elsewhere – that the pipeline capacity for heavy crude would be less because the latter does not flow as easily as light crude. That member also pointed out that the Houston Lateral expected online by the end of 2014 will have the capacity to ship the entire 830 Mb/d of crude from Cushing into Houston rather than just 130 Mb/d as we suggested. That possibility – facilitated by a valve mechanism at the Liberty terminal will give TransCanada the flexibility to switch the full pipeline flow (or presumably a subset thereof) between Houston and Port Arthur to meet shipper requirements. [On an editorial note, we welcome comments from RBN Members on our blogs - that are read every day by thousands of industry professionals – please be patient if they take a while to show up on the website as we screen the content to save your blushes.]

Seaway

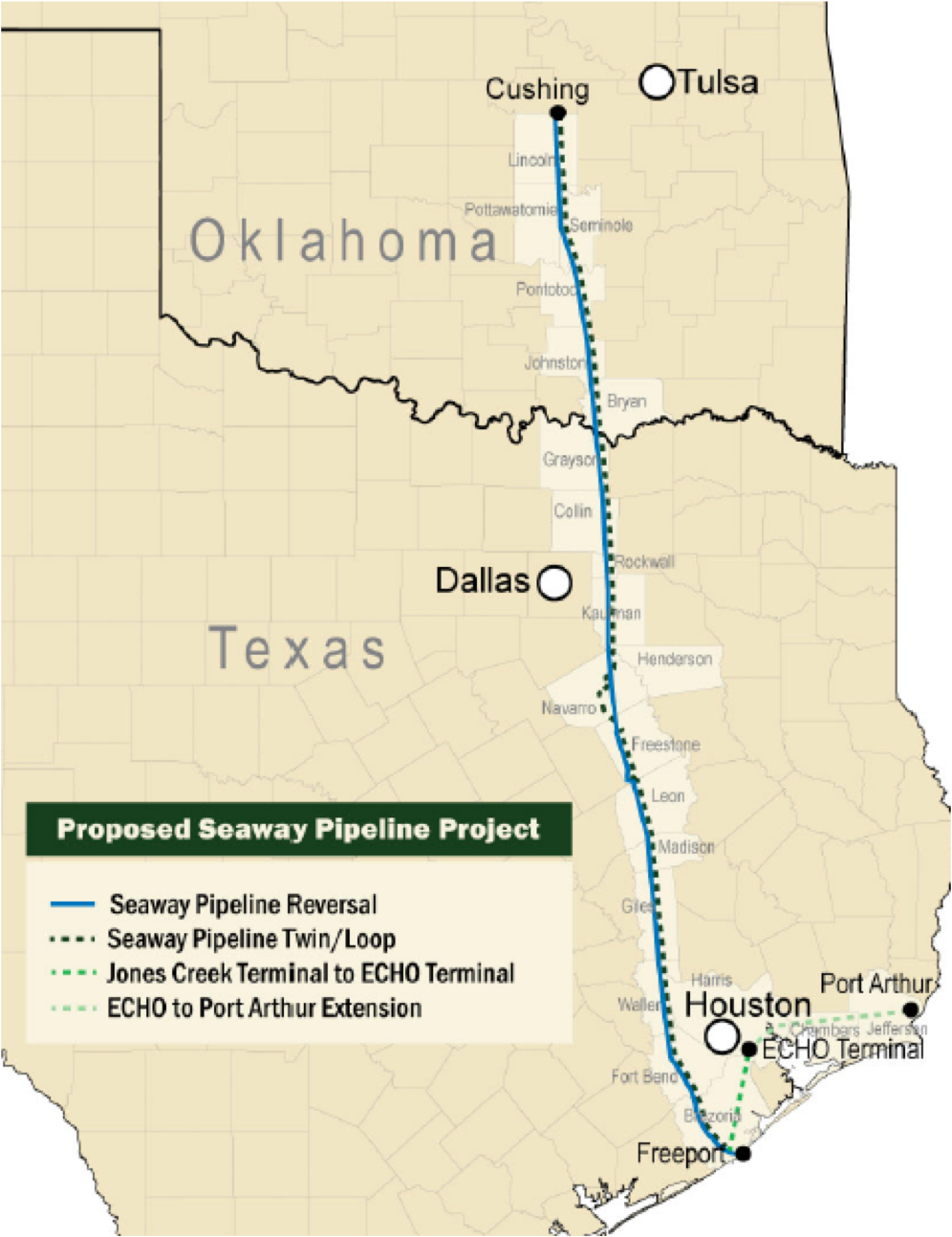

Seaway Crude Pipeline Company LLC (Seaway) is a 50/50 joint venture between Enterprise Products Partners L.P. (EPP) the operator, and Enbridge Inc. The Seaway pipeline is a 500-mile, 30-inch diameter pipeline that runs from Cushing, Oklahoma to Freeport on the Texas Gulf Coast, south of Houston (see map below). The Seaway pipeline originally shipped imported crudes from the Gulf Coast to Cushing but has been reversed to ship rising domestic and Canadian crude production from the Midwest to the Gulf Coast region where fifty percent of the country’s refining capacity resides (see Seaway Reversal and Expansion). Seaway’s reversal is a multi year project that has come online in two phases so far, the first in July 2012 providing 150 Mb/d capacity and the second in January 2013 expanding to 400 Mb/d. The final phase of the Seaway project, currently under construction, is a loop (twin) pipeline that will more than double capacity to 850 Mb/d. Phase three is expected online during the second quarter of 2014.

Source: Seaway Pipeline Website

As part of the Seaway reversal and expansion projects, additional pipelines are being constructed to allow shippers to access the EPP Enterprise Crude Houston Oil terminal (ECHO) in southeast Houston. We have posted a couple of blogs on the build out of the ECHO terminal in the past year, first back in November 2012 (see ECHO and the Blending Men) and more recently in May (see Texas Terminal Wars). Access to ECHO is a critical part of the Seaway project because of it’s growing storage capacity (750 MBbl today, 1.6 MMBbl by the end of 1Q 2014, and 6 MMBbl by 2015) and ongoing connections to Houston and Port Arthur/Beaumont area refineries.

Comments

With the surge in domestic & Canadian crude headed to the Gulf Coast, it would seem the import levels from Venzuela and Mexico would be most at risk of losing market share as they do not have JV refinery operations located in the Gulf to assure a market. Would be most interested in RBN's assesssment. Additionally, Would the economics allow Canadian crude brought to the Gulf to be exported from the Gulf?

In reply to Mexican & Venezuealan Crude Imports by Neil Nelson

I second Crysball's comment regarding RBN's assessment of the vulnerability of imports from Venezuela and Mexico. This might involve an analysis of the Argus Sour Crude Index, which apparently is used by some of the JV refiners Crysball alludes to.

It is time we all use correct terminology.

Dilbit is not heavy crude nor is it heavy oil. Dilbit, typically a 30% mix of gas condensate in raw bitumen, fundamentally differs from heavy crude or heavy oil in terms of flammability and toxicology of the diluent, and difficulty in clean-up after spills due to the fact that raw bitumen, by definition, has an API gravity less than 10, causing it to sink in fresh water.

It is technically incorrect, physically misleading, and dishonest to call dilbit "heavy oil" or "heavy crude" if it is a mix of either raw bitumen, or even very heavy oil, with condensate diluent.

What underlies 54,132 square miles of land in northern Alberta is neither "oil sands" as used by proponents or "tar sands" as used by opponents but bitumen-saturated partially-consolidated sandstone or carbonate reservoirs. Bitumen sands, bituminous sands or sandstones, or bituminous carbonates, if you please.

Bitumen can produce tar-like asphalt once processed but neither bitumen or asphalt are tar. Tar is a black, thermoplastic material produced by the destructive distillation of coal. Neither is bitumen oil until upgraded to a suitable refinery feedstock like syncrude which requires further refining into useable oil products. Get it? Raw bitumen, then dilbit or syncrude, then commercial oil products. Asphalt, used as a binder for aggregate in paving roads, is produced only in relatively small quantities at upgraders and refineries.

Dear Abccannuck, Althought they have high pour point, Syncrude and WCS are still amongs heaviest sour grades in the world. (Heavy: API 11, S 3.5%, TAN KOH 0.93/g (total acidic number). If we can't call them Heavy sour, maybe "challenging crudes", "alternative crude", "opportunity crudes" is valid because they present processing challenges due to high levels of water, salt, metals, solids, asphaltene incompatibility, high pour point or high conductivity.

Simon