If you add up the numbers since the start of 2012 just under 2 MMb/d of transport capacity has been added to bring crude into the Texas Gulf Coast refining region. In the next two years (2014 and 2015) we expect another 2.1 MMb/d of crude pipeline and rail transport capacity to be added. In total that is over 4.1 MMb/d of potential incoming crude – to a region with just under 3.7 MMb/d of nameplate refining capacity. Today we begin a series describing the incoming flood of crude and preparations being made to handle it.

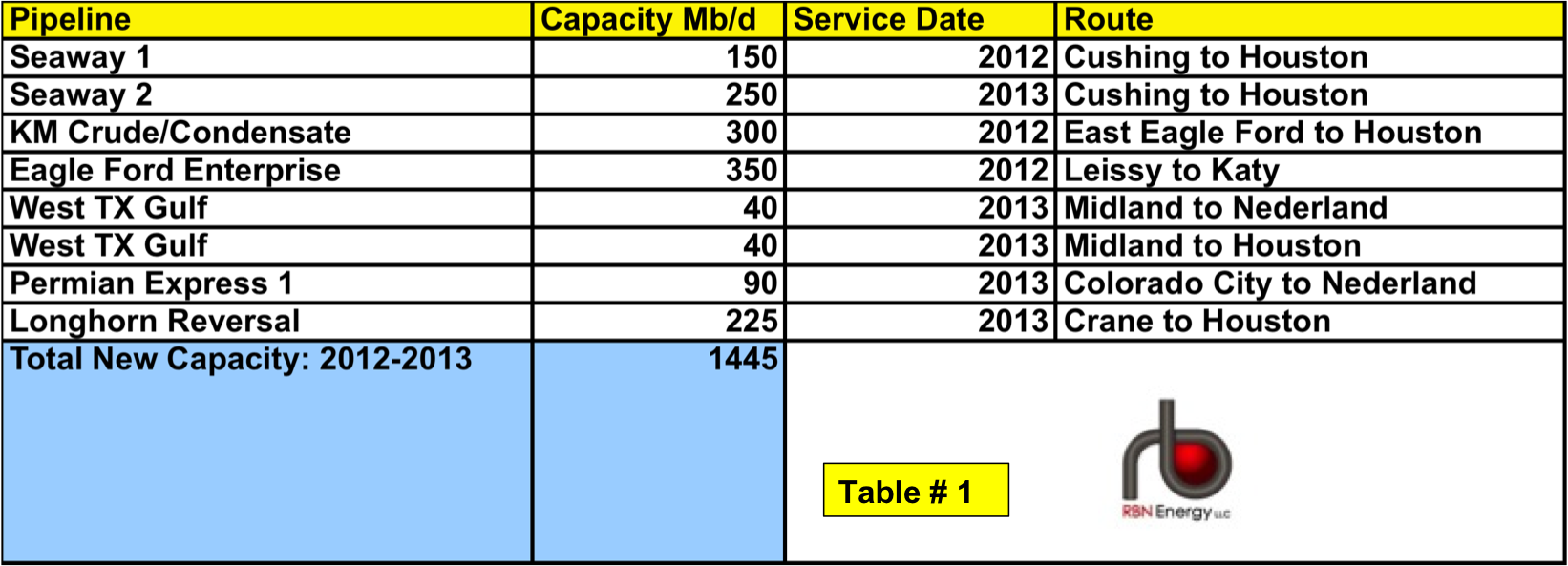

A lot of new crude oil supplies have descended on Texas Gulf Coast refineries in the past two years. Since the start of 2012 approximately 1.4 MMb/d of pipeline capacity has been added to transport crude into the region. Table #1 below lists the pipeline projects and their capacity. The crude flows are coming from Cushing on the Seaway pipeline, from the West Texas Permian Basin and from the Eagle Ford in South Texas.

Source: RBN Energy

In addition to incoming pipeline capacity at least 128 Mb/d of crude supplies have been arriving into the Gulf Coast region as a whole by barge from the Midwest (July 2013 - source Energy Information Administration – EIA). For the sake of this exercise we will assume that most of that waterborne crude (75 percent) is headed to Louisiana on the Mississippi River – leaving 25 percent coming to the Texas coast - 32 Mb/d. A great deal more waterborne crude is headed to Texas Gulf Coast refineries from the Eagle Ford via Corpus Christi. As we detailed a couple of weeks back the Port of Corpus Christi reported 387 Mb/d of crude leaving for Gulf Coast destinations in August and Clipper Data estimates that 55 percent of that crude arrived at Texas Gulf Coast refineries – 213 Mb/d (see Float On). Adding the Corpus volume to the Midwest volume into Texas we get a total inbound barge volume to the Texas Gulf Coast of (213 + 32) = 245 Mb/d.

And of course increasing volumes of crude have been shipped to new unloading terminals on the Gulf Coast by rail. Most of those terminals are on the Louisiana side of the Gulf Coast but there are now at least three unit train crude-by-rail unload facilities operating at Port Arthur (GT Omniport 100 Mb/d), Beaumont (Jefferson Energy 70 Mbd/) and Galveston [Texas International Terminals 90 Mbd)]. That’s another potential 260 Mb/d of crude arriving at Texas Gulf Coast refineries.

Adding up these existing incoming crude transport capacity totals we get:

Pipeline additions since 2012 (in service now) 1445 Mb/d

Waterborne movements 245 Mb/d

Rail unloading capacity 260 Mb/d

Total 1950 Mb/d

That’s precious close to 2 MMb/d of new crude arriving if all that capacity is used.

But the influx of new crude is not going to stop there. Table #2 below shows pipeline projects planned to come online in 2014 and 2015 bringing another 1.9 MMb/d of potential crude supplies into the Texas Gulf Coast region. Most of that crude will be coming from Cushing – on the Seaway (additional 450 Mb/d) and Keystone Gulf Coast XL (additional 700 Mb/d to Nederland, TX and 130 Mb/d to Houston) pipelines. The rest comes from additions to pipeline capacity from the Permian basin. On top of pipeline additions the KW Express rail unload terminal at Greens Port will have 210 Mb/d capacity online in 2014 and a proposed Magellan/Vopak rail unload facility at Deer Park would handle 72 Mb/d in 2015. And there is more. We can only guess at how much more Eagle Ford crude and condensate will be headed to Houston by barge in the next two years – new dock facility additions are planned at Corpus Christi to help get growing supplies arriving at the port by pipeline onto barges and tankers (see We’re Jammin’). For the moment we will make the conservative assumption that inbound waterborne crude from the Eagle Ford will remain at or about current levels because of dock space constraints and limited availability of qualified Jones Act barges that can carry crude in US waterways (see The Sea and Mr. Jones).

About the song

The song “I’m Waiting For The Man” appeared on The Velvet Underground & Nico (1967) - thanks for giving us alternative Lou.

Comments

It would be useful to have one of your blogs publish a glossary of fracking and horizontal drilling terminology and how the different technologies are used. For example, slick water fracking versus zip fracking...pros and cons, etc.