Yesterday (April 30, 2014) the Energy Information Administration (EIA) reported yet another increase in Gulf Coast inventories as of April 25 - adding 5.7 MMBbl to set a new record of over 215 MMBbl of crude. Stocks in the region are now 27 MMBbl above the 5-year average and even if refiners cranked up output to the highest levels ever (96.5 percent utilization) the surplus would take at least 3 months to get back to “normal”. Crude prices are being impacted as the premium of Light Louisiana Sweet (LLS) crude at the Gulf Coast over West Texas Intermediate (WTI) delivered to Cushing, OK has narrowed close to $2/Bbl. With no crude exports allowed to ease the surplus it looks like Gulf Coast prices will remain under pressure. Today we look at prospects of reducing the crude surplus.

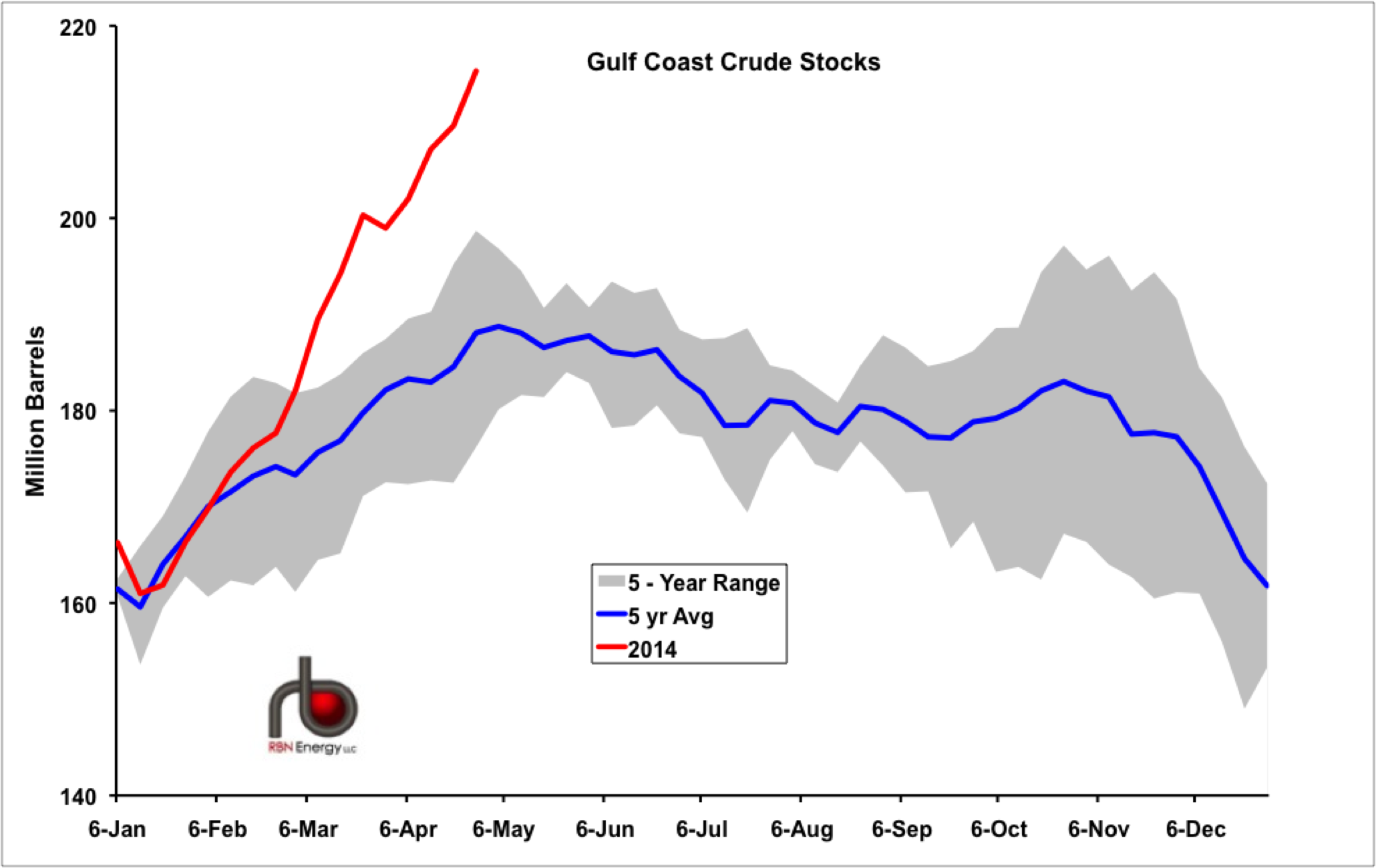

This week (according to EIA data) crude stocks in Petroleum Administration Defense District (PADD) 3 – the Gulf Coast region - set a new record of 215.3 MMBbl. At the same time inventories at Cushing fell again as they have been doing since January – down another 0.6 MMBbl to 25.4 MMBbl on April 25, 2014. As we discussed in an earlier episode of this series (see The Cushing Crude Stockpile Heads to the Gulf Coast) the Cushing draw down is principally prompted by new outbound pipeline capacity and backwardation (prices lower in the future than today) in the futures market. Gulf Coast inventories are piling up as new crude arrives in the region from Eagle Ford and Permian production as well as increased volumes from Western Canada via Cushing. Figure 1 below shows PADD 3 crude oil stocks for 2014 (red line) as well as the average of the previous 5 years (blue line) and the high low range over that period (grey area). As you can see, over the past 5 years there was a normal seasonal pattern to Gulf Coast crude with inventories higher in the summer and lower in the winter. But this year that seasonal pattern has gone out of the window with inventories jumping sharply – rising above the 5 year average at the end of January and not looking back since.

Figure 1 – Source EIA and RBN Energy

Comments

I wonder what the cost is to carry such inventories are ?

Thank you for the excellent report.

Lifting the 1970's era prohibition on US exports of crude, at least from the Gulf Coast region to the EU, would enable the EU to restrict imports of Russian crude as a sanction for Ukranian aggression.

http://info.drillinginfo.com/us-crude-oil-can-save-the-ukraine-from-russian-aggression/

The Atlantic coast of Canada may the next exit valve. Oct/Nov 2014

Line 9 reversal expansion will take 320Mbd light Crude into Montreal 400Mbd refining). The economics exist for Irving Oil 300 Mbd(Rail + Gulf Tanker) and Come By Chance 115 Mbd (US Gulf tanker) to use US imports only ($2 to tanker from USGC)

Canadian Atlantic Offshore Crude production (240Mbd) exported to other countries or to US depending on Bakken/Brent spread. Same as exporting 250 Mbd of US intermediate Crude to international markets.

Would be great to see a post on effects of Enbridge system changes and expansions and line 9 reversal. I believe it'll quite pronounced as it lightens the loads on the all sustems heading into Mid con. Almost like 320Mbd vanishing.

Permian production (which will come in much higher than forecast, see the horizontal righ count change), Bridgetex, Seaway, Flanigan, will keep LLS/Brent under pressure and ecomomics strong for BakCan.

As long as LLS stays under pressure, there is incentive for Imperial oil refinery (88Mbd) Dartmouth, NS, CA to open back up. Similarly there is a case to be made for opening up other east coast refineries (all light crude) to export products. Cheap Natural gas, better utilization rates, super strong balance sheets and access to cheaper capital. Will keep us refiners at an advantage for the forseeable future.

Starting this summer we'll see more impact of US Can production on the world markets.