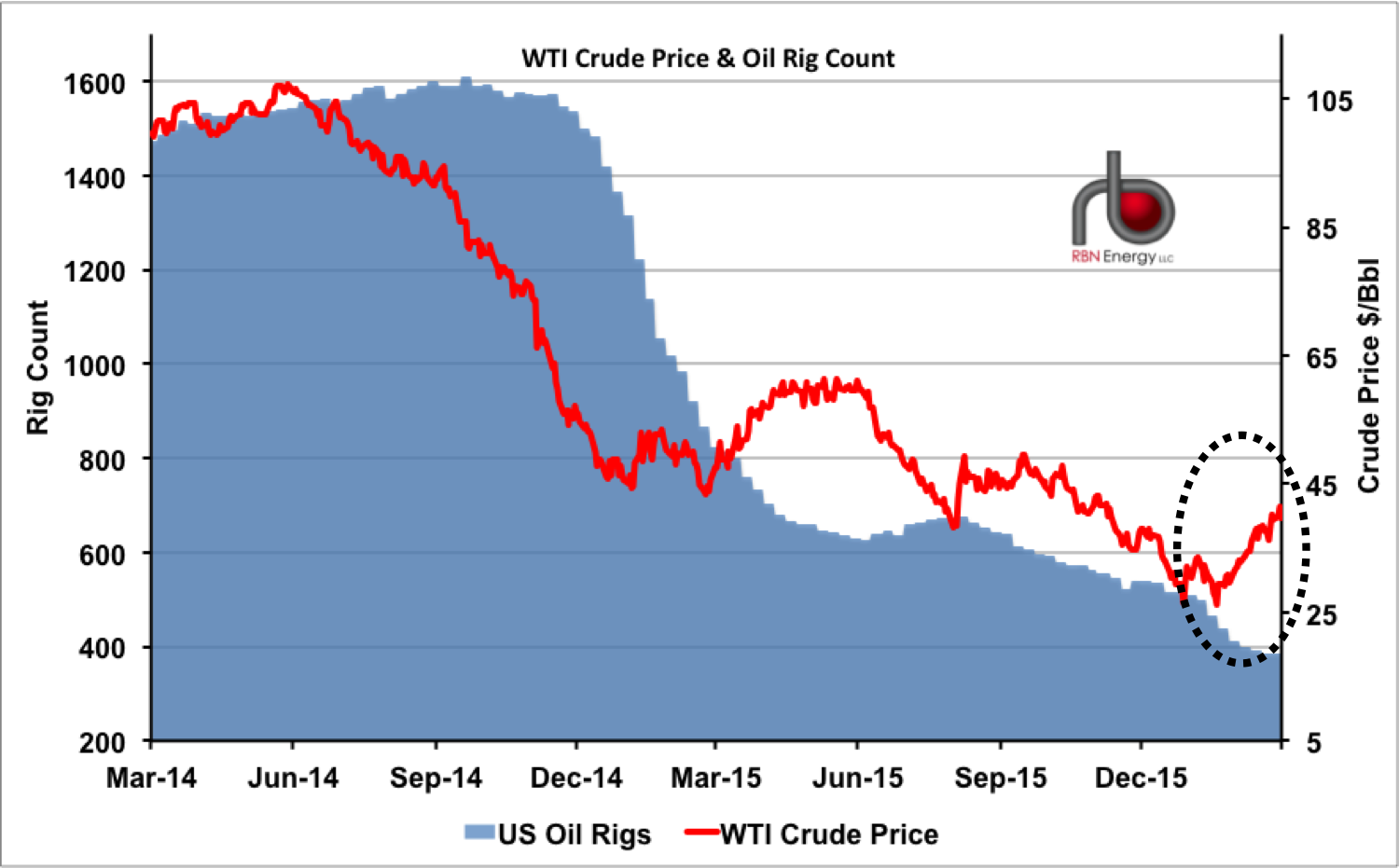

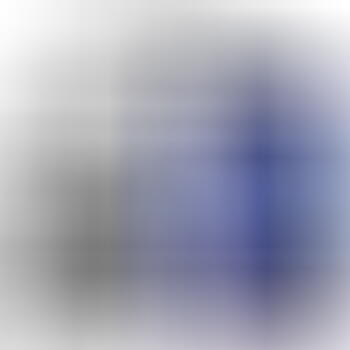

In the five weeks since February 11, the price of WTI crude oil on the CME/NYMEX spiked 50%, up from $26/bbl to $40/bbl (see black dashed circle in Figure #1). For hedge funds that took long positions in February, it was an awesome trade. And for beleaguered producers, it was certainly a bit of good news. But there are no celebrations in the streets of Houston and Oklahoma City. The fact that $40/bbl should be considered “good news” is sobering: Eighteen months ago, that price level would have been seen as a catastrophe for the producing community. In fact, it still is. In today’s blog we examine the factors that help push prices above $40/bbl and what it will take to really get US production growing again.

Yes, $40/bbl crude oil will help the balance sheets of most oil and gas producers. A handful of rigs might be put back to work. But let’s put things in perspective. Since October 2014, the price of crude is down 60%, over 1,200 rigs drilling for crude (75%) have been idled (see Figure #1), and thousands of oil industry workers are looking for jobs. Producer CAPEX budgets have been slashed, and the reality is that a price of $40/bbl will do little to change the meager investment plans that most producers laid out in their Q1 earnings calls. At $40/bbl, producer returns for drilling most shale wells are under water. Consequently, new drilling has slowed to a crawl. A few companies have declared bankruptcy, and more are on the way.

Figure #1; Source: Baker Hughes and CME Data from Morningstar, RBN Energy

In the midst of this carnage, the market has started – ever so slowly – to correct itself. Production volumes are declining. Even though the US Energy Information Administration reports that US crude oil production remains above 9 million barrels per day, it is down about 600 thousand barrels per day from its peak this time last year, and will likely drop at least another 750 thousand barrels per day by year end.

Comments

Supply and demand fundementals are sticky, but eventually work. Thanks.

You've just described basic supply and demand. There's no added insight from your post. "Floors" and "ceilings" are just fluffy words.

And it's not a new concept that in commodity industries there can be a price cycle based on the time to bring new supply on line (if oppty exists for +NPV full cycle investment) or the time for supply to exit (that is negative on full cycle costs, but positive on variable costs).

It's possible to add some new insights based on changed time elasticity of shale or in depth discussion of cost curves. But you don't even do that. Just...'if prices get high new supply will come on' and 'if prices get too low, supply will dwindle' as if those are some kind of brainstorm.

I generally agree with the argument and it will be the dominating sentiment in the oil market, but how much incremental oil can the US pump out every year, and how would the medium term global S-D be, if the oil is capped at $55?

If you are a believer of the technology in shale oil, think about this:

What about other non-OPEC non-North American producers whose supply contiribution is about a half of global? At this pace of capex, we may see the oil output in that block to fall at least 1% per year from 2017-18. That's 500kb/d YoY decline roughly.

Remeber during a decade before oil crash (2005-14) with Brent oil averaging about $86, Non-OPEC Non-NA had no production growth. Those countries are mostly free from geopolitical risks, so it dictates that oil over 90 couldn't justify the addtional supply, or outside the NA or ME oil was actually depleting.

Speaking of OPEC - after Iran ramp up, they will be running at or close to the full capacity.

So if OPEC is flat and other Non-OPEC Non-NA (a half of the pie) declines, can the US/Canada pump out a lot more, enough to offset the decline perhaps (-0.3 to -0.7mb/d in aggregate) and furthermore meet the +c1.0mb/d YoY demand growth? I.e Can US production at end of 2020 be 14-15mbd?

I don't think so, as the oil ventures will find it harder (than old good days) to borrow money from the bearish ppl in the finance industry. And when the service sector undergo a period of consolidation, the cost will also rise.

So i think 35-55 (what is priced in the futures curve up until 2022-23) can only be the medium/long term pirice when a recession happens and as a consequence no growth in oil demand.