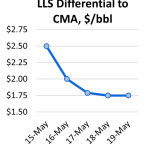

The premium for Louisiana Light Sweet (LLS) crude over the price of the NYMEX Contract Monthly Average lost altitude last week on news of an imminent restart of the Zydeco pipeline which ships crude from the Houston area to St. James, LA. The pipeline was originally closed on April 25 after a line break and boosted the relative value of LLS and other crudes in the St. James region for a number of weeks. In wider crude oil headlines last week, the WTI prompt contract recorded a weekly gain of $1.51/bbl, breaking the trend of four straight weekly losses.

Featured Articles

- Blog

The Price is Right - North America Crude Oil Price Differentials Explain and Foretell Market Shifts

There is no debate about it: The CME/NYMEX domestic sweet (DSW) crude oil futures prompt-month contract at Cushing, OK, is the most closely followed benchmark in U.S. energy markets. It’s the price quoted in nightly news reports and general media publications. And now, with U.S. exports of WTI deliverable on the Brent contract, domestic sweet at Cushing is arguably setting the price for crudes around the world. But the fact is, most crudes traded in physical markets across North America are not priced at the DSW-at-Cushing benchmark but instead at a differential to Cushing — higher or lower on any given day based on each crude’s unique quality, location, and supply/demand characteristics. In today’s RBN blog, we discuss how the behavior of differentials from the Cushing benchmark can go a long way to explain what is happening with crude oil production, transportation volumes, storage and, of course, exports.

- Blog

Tank House Blues – Brent, WTI and LLS Learning to Live With A Crude Oil Glut

In spite of a brief respite provided last week by increased geopolitical risk in Saudi Arabia, crude oil prices are still in the $50/Bbl range – down more than 50% since last Summer - and inventories at Cushing and on the Gulf Coast continue at record levels. The fall in crude prices was initially consistent across markets with international benchmark Brent trading within $1/Bbl of U.S. benchmark West Texas Intermediate (WTI) and Gulf Coast marker Light Louisiana Sweet (LLS) in January 2015. But since February the relationship between Brent, WTI and LLS has changed as the build up of Cushing inventories weighs on prices in the Midwest. Today we provide an update on crude price differentials at The Gulf Coast.

- Blog

One Step Beyond? - Bakken Prices Threatened by Narrowing Brent/WTI Spread

Yesterday the Intercontinental Exchange Brent premium to WTI NYMEX closed at $9.31/Bbl, its lowest value since January 2012. Spread watchers have long anticipated this narrowing but it throws a spanner in the economics of crude by rail shipments from North Dakota. Today we suggest that the Brent/WTI spread may have narrowed before crude supply fundamentals justify the move and that it could widen again quickly to $15 or higher.