Featured Articles

Hurricane Helene to Make Landfall Between Major Energy Infrastructure

Let Me Move You, Part 5 - How LNG Exports Will Change Gulf Coast Natural Gas Markets in 2019

One of the biggest factors affecting the U.S. natural gas market in 2019 will undoubtedly be the dramatic rise in LNG export demand. The slate of liquefaction and LNG export capacity additions this year will boost U.S. demand for feedgas supply to nearly 9 Bcf/d by the end of the year, almost tripling the 2018 full-year average of 3.1 Bcf/d and close to doubling the December 2018 average of 4.6 Bcf/d, with the lion’s share of that growth happening along the Texas and Louisiana Gulf Coast. Three liquefaction trains — one each at Cheniere Energy’s Sabine Pass and Corpus Christi terminals, as well as one at Cameron LNG — are likely to be fully operational in the first quarter, with five additional trains due in rapid progression later in 2019. That much new gas demand concentrated in one region is bound to disrupt physical flows and pricing dynamics. Today, we wrap up the series with a look at the timing and feedgas routes for the final two facilities: Freeport LNG in Texas and Kinder Morgan’s Elba Island project in Georgia.

Such Great Heights - U.S. LNG Feedgas Demand Surges as Export Capacity Additions Continue

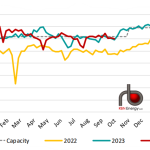

If there’s one word that sums up the U.S. LNG export market over the past year, it’s resilience. After taking a pummeling last year, feedgas demand and exports have roared back, reaching new heights in recent weeks, and are headed still higher in the coming months as new liquefaction capacity is commissioned at a faster pace than expected. Train 3 at Cheniere Energy’s Corpus Christi LNG facility came online on March 26, increasing U.S. LNG export capacity to 75 MMtpa (~9.9 Bcf/d), which equates to a total feedgas demand of nearly 11 Bcf/d. Two more export projects — 18 modular trains at Venture Global’s new Calcasieu Pass facility and the sixth train at Cheniere’s existing Sabine Pass — are on track to ship their first commissioning cargoes later this year, ahead of their originally proposed construction schedules, and will be fully operational in 2022. This is quite a different picture from last year, when nothing but uncertainty loomed on the horizon in a COVID-hit world and progress for just about every project was in jeopardy. Today, we start a short series providing an update on the status of operational and under-construction export capacity and where LNG feedgas demand is headed this year.