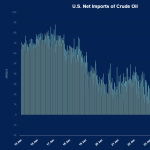

Last week, flat crude oil production, lower imports, record exports, and slightly stronger refinery demand sharply tightened the U.S. crude balance. The biggest shift came from crude oil exports, which surged to a record 6.4 MMb/d and helped push the U.S. into net crude exporter status for the first time ever. Imports fell to 5.75 MMb/d, led by PADD 1 dropping to a record low of 135 Mb/d, potentially aided by the Jones Act waiver encouraging more Gulf Coast barrels to move to the East Coast. Strong outbound flows and firmer refinery runs drove major draws across crude oil, motor gasoline, and distillates. Crude prices responded to the tighter setup, with WTI rising $10.55/bbl, or 12.6%, to end the week at $94.40/bbl. Prices have continued to run up, and WTI is currently trading over $105/bbl.

Featured Articles

Double-Edged Sword – Refinery ‘Capacity Creep,’ Falling Inventories May Limit U.S. Crude Export Surge

U.S. crude oil production averaged a record 13.6 MMb/d in 2025, up nearly 1.6 MMb/d from 2023, but crude export volumes remained remarkably stable — at or very near 4.1 MMb/d — until a recent Iran-related surge. A key reason: “capacity creep” expansion projects at several Gulf Coast refineries.

Let It Go, Let It Flow – Jones Act Waiver Opens Up New Routes for Foreign-Flagged Ships on U.S. Waters

The White House gave the green light on March 18 for foreign-flagged tankers to move crude oil and refined products between U.S. ports by waiving the Jones Act. In less than two months, about 60 waivers have been recorded. Today, we’ll dig into the new patterns that have emerged.

How’s It Going to Be – How a Prolonged Conflict with Iran Could Disrupt U.S. Gasoline, Jet and Diesel Markets

The U.S. is seeing softer domestic demand for traditional fuels, but pockets of the country remain highly dependent on imported gasoline, jet fuel and diesel. Today, we’ll zero in on which PADDs are at the highest risk for shortages and price spikes if the Iran war drags on for an extended period.