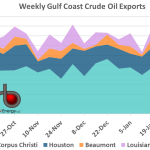

Crude exports from the U.S. Gulf Coast rebounded decisively to 5.0 MMb/d, the second-highest weekly value in RBN records. Coming off a week with a fairly low value, this could simply be a slightly more-extreme week-to-week variation, or a continuation of the longer-term upward trend in exports.

Featured Articles

- Blog

Summertime - Low European Stocks, High Global Gas Prices to Keep U.S. LNG Production at Full Capacity

U.S. LNG export terminals are running at their operationally available and contracted levels and will continue to do so, with no economically driven cargo cancellations anywhere on the horizon. Global gas prices are well supported by low storage levels in Europe, and it will take time to refill inventories, which means these high prices are not going away anytime soon. The upshot: U.S. LNG will have a very different kind of summer than it did last year, when global prices were at historic lows and many U.S. terminals saw more cargo cancellations than exports. Feedgas in April this year averaged 10.77 Bcf/d, nearly 3 Bcf/d higher than last year, and as we progress into summer, the year-on-year delta will become even more pronounced. Barring any major operational issues, feedgas demand will stay around 11 Bcf/d, which is the level needed for the terminals to produce at full capacity. That’s in stark contrast to last summer, when feedgas demand cratered and averaged as low as 3.34 Bcf/d in July as cargo cancellations peaked. Today, we look at what’s supporting global gas prices, how that impacts export economics for U.S. LNG, and what that means for feedgas demand in the months ahead.

- Blog

It's Too Late - Global Natural Gas/LNG Supply Squeeze Sets Stage for Record Winter Prices

Global natural gas and LNG prices have spent the summer going from high to higher to the highest on record. The major European indices hit post-2008, and then all-time highs multiple times throughout the summer — even surpassing Asian prices on a handful of days. At the same time, Asian prices have set all-time seasonal records and are now sitting just below the previous single-day high settle from this past January. Usually, as the weather cools heading into fall, so do prices, but that’s unlikely this year as the European gas storage inventory is at the lowest level for this time of year than we’ve seen in recent history, and the time to replenish stocks for the winter is rapidly running out. The incredible bull run for global gas prices has been underpinned by high demand for LNG and the cascading effect of a supply squeeze in Europe, brought on by the triple threat of low domestic production, decreased imports from Russia, and a scarcity of incremental LNG cargoes. Not only is this driving record-high gas prices and increased volatility now, but the low inventory means sustained high prices for the heating season ahead. In today’s blog, we take a look at recent global gas price trends and the precarious European storage situation ahead of what is shaping up to be an incredibly bullish winter.

- Blog

Listen Up! - Hear What the Shale Revolution Really Means: The Domino Effect Audio Book

Crude oil and natural gas prices are back from the abyss, but does that mean the long awaited recovery is underway? Maybe so. But maybe not. Energy markets are fickle, driven by a chain of interactions where one market event triggers another, and then another. Rusty Braziel’s best-selling book, The Domino Effect, explores 30 such market events, which are represented by dominoes – hence the title of the book. More dominoes are falling now and still more will fall in years to come. This book explains the interconnectedness of energy markets through an analysis of energy market fundamentals: prices, flows, infrastructure, value, and economics. And good news for fans of audio books: The Domino Effect is now available on Amazon in Audible format. Today’s blog, an advertorial for the audio book, highlights what The Domino Effect has to say about what’s going on now.