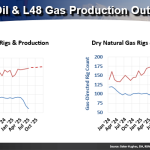

Improvements in drilling rig efficiency have allowed U.S. crude oil and natural gas production to move higher this year even as the overall rig count – which is normally a bellwether of production trends – has moved lower. That trend was discussed as part of the U.S. oil and gas production outlook on Day 1 of RBN’s School of Energy Canada, being held Tuesday and Wednesday at the Hyatt Regency in Calgary.

Featured Articles

- Blog

All Shook Up - Arrow Model Forecasts Shifts in Gas Flows, Basis as New Pipes, LNG Capacity Arrives

The rapid growth in U.S. natural gas production and LNG exports over the past 10 years was just the beginning. Between now and 2035, gas production in the Permian, Eagle Ford, Haynesville and other plays will continue rising, the Gulf Coast’s LNG export capacity will double and many new pipelines will be built. New gas-fired power plants will be added, too. The shifts in gas flows as new production and infrastructure come online will be frequent and often sudden, as will the changes in basis at gas hubs throughout Texas and Louisiana. Is there any way to make sense of it all? There sure is. In today’s RBN blog, we continue to explore how our Arrow Model helps guide the way.

- Blog

Hugh Do You Love? Encore Edition - A New Entrant to Tackle the Permian's Dire Need for Gas Takeaway Capacity

Negative natural gas prices have been breaking hearts in the Permian Basin for many years, with pipeline development struggling to keep pace with rapid increases in associated gas production, but 2024 has shattered all previous records for the severity and length of negatively priced periods. The Matterhorn Express Pipeline, which started partial service at the beginning of October, is helping to stabilize the market for now, but with more production gains on the way, additional takeaway capacity will be needed. And after this year’s run of negative prices, producers have been willing to commit to new capacity.

- Blog

Hugh Do You Love? - A New Entrant to Tackle the Permian's Dire Need for Gas Takeaway Capacity

Negative natural gas prices have been breaking hearts in the Permian Basin for many years, with pipeline development struggling to keep pace with rapid increases in associated gas production, but 2024 has shattered all previous records for the severity and length of negatively priced periods. The Matterhorn Express Pipeline, which started partial service at the beginning of October, is helping to stabilize the market for now, but with more production gains on the way, additional takeaway capacity will be needed. And after this year’s run of negative prices, producers have been willing to commit to new capacity.