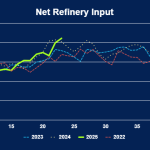

Refinery activity surged last week, with total net inputs climbing 230 Mb/d to 17.225 MMb/d, the highest level since late 2019. Gross inputs rose by 170 Mb/d, pushing utilization up nearly a full point to 94.3%, with PADDs 2 and 5 leading the gains. On the demand side, motor gasoline bounced back strongly, rising 900 Mb/d after the previous week’s steep drop, though demand swings of this magnitude for three straight weeks point to an unusually volatile market. Despite the rebound, the sharp increase in refinery throughput added 1.5 MMbbl to gasoline inventories. Meanwhile, crude prices moved higher, but product gains didn’t keep pace, pressuring refining margins. The 3-2-1 crack spread dropped 6.8% to $20.05/bbl as falling gasoline cracks outweighed a small uptick in diesel.

Featured Articles

Don’t Stop The Party – Why Refiners Kept On Dancing As The Crude Price Collapsed

While many companies in the energy sector – particularly in the producer community – are licking their wounds and reporting lower profits and reduced capital expenditure to their stockholders this quarter, refiners have continued to thrive. Lower refined product prices have begun to increase domestic consumption of gasoline and diesel in the face of longer-term decline trends. And strong refining margins continue to encourage high levels of refinery utilization. Today we start a two-part look at how U.S. refiners are faring after the oil price crash.

Where Did Our Distillate Go? Stocks Low as Heating Oil Season Arrives

U.S. inventories of distillate — especially ultra-low-sulfur diesel (ULSD) and heating oil — are at their lowest pre-winter level in three years after falling during the summer months for the first time since inventory records started being measured in 1982. Rising diesel exports are one culprit; another is the shutdown of a number of Gulf Coast refineries during and immediately after Hurricane Harvey. The good news is that distillate prices have been increasing, as have the margins for refining crude oil into distillate — both encouraging refineries to ramp up their diesel/heating oil production. Today, we look at recent developments in the distillate market and what they may mean for diesel and heating oil prices this winter.

Strange Brew - COVID-19 and the Crude Oil Price Crash Puts the Screws on U.S. Refiners

The collapse in crude oil prices and COVID-19’s very negative effects on global gasoline, jet fuel and diesel demand are putting an unprecedented squeeze on U.S. refiners. Even before the initial coronavirus outbreak in Wuhan, China, started to grab headlines around New Year’s Day, refineries had already been incentivized to shift their refined products output toward diesel, which can be used to help make IMO 2020-compliant low-sulfur bunker. Now, with the COVID-19 pandemic spreading to Europe and North America and stifling consumer transportation fuel demand, the price signals are even stronger, pushing refineries to do everything they can to minimize their gasoline and jet fuel production and enter what you might call “max diesel mode.” Today, we discuss how there are challenges and limits to what they can do, and a number of refineries may need to shut down due to lower demand, at least temporarily.